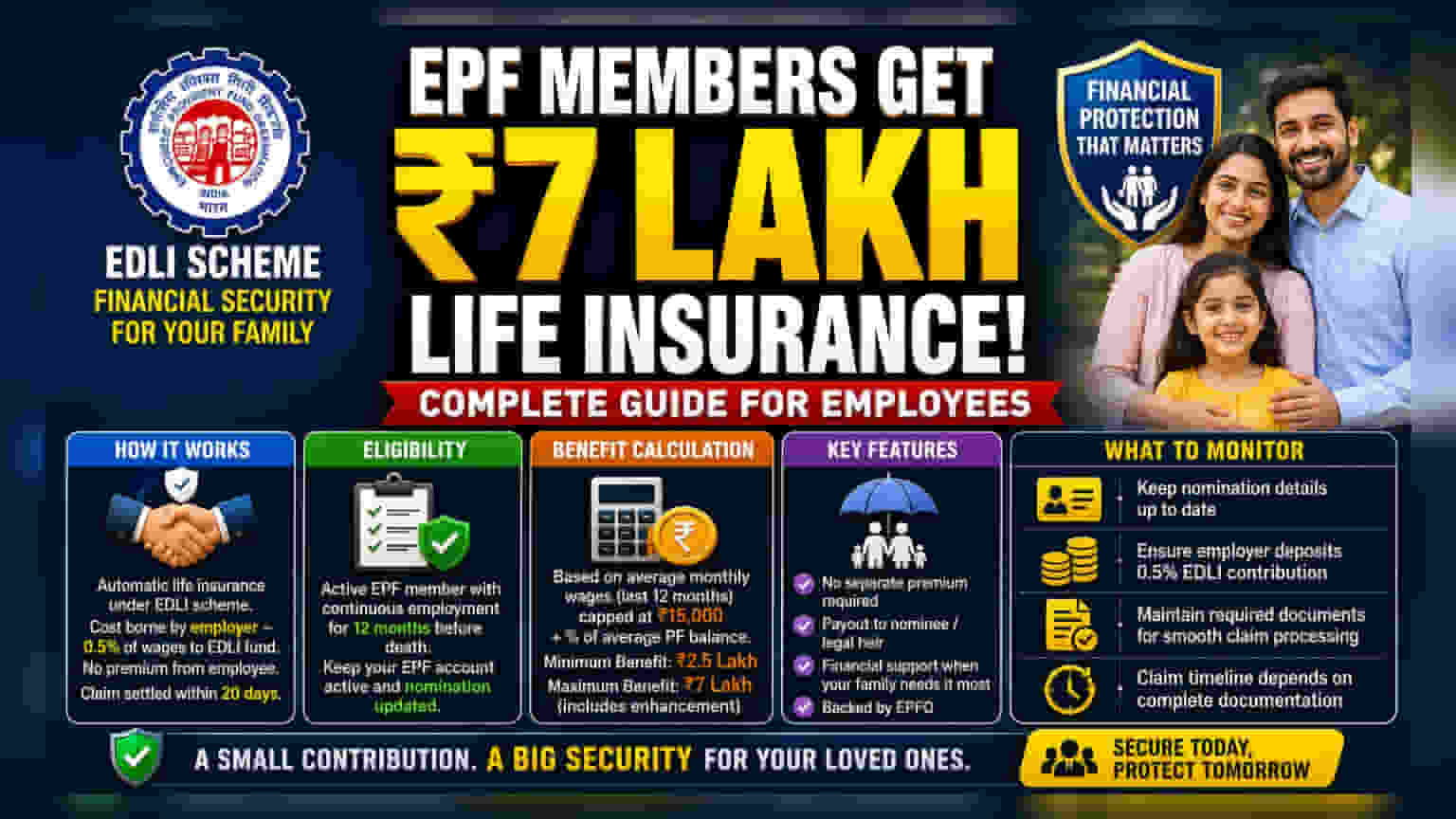

Employees' Provident Fund (EPF) subscribers receive life insurance cover of up to Rs 7 lakh under the EDLI scheme. This benefit is fully funded by employers at no extra cost to the employee, offering a financial safety net for families in the event of the member's death while in service.

What Happened

Employees who are active subscribers of the Employees' Provident Fund (EPF) are entitled to life insurance coverage of up to Rs 7 lakh. This benefit is provided under the Employees' Deposit Linked Insurance (EDLI) scheme, managed by the Employees' Provident Fund Organisation (EPFO). The insurance is designed to provide immediate financial support to the families of employees in the event of their unfortunate death while still in service. This coverage is automatic for all active EPF members and requires no separate premium payment or contribution from the employee.

How The Coverage Works

The EDLI scheme is essentially an insurance product linked to the EPF account. The entire cost of this insurance is borne by the employer, who contributes 0.5% of the employee’s monthly wages into the EDLI fund. Because the employer funds the scheme, there is no direct impact on an employee’s take-home pay or their monthly PF contribution. The insurance payout is disbursed to the designated nominee or legal heir in the event of the member's death. The EPFO aims to process these claims within a 20-day window to ensure timely support for the family.

Eligibility Criteria

While the insurance is automatic for active members, there is an important eligibility condition regarding tenure. Typically, the scheme requires that the employee must have been in continuous employment for the preceding 12 months to be eligible for the insurance benefit. This ensures that the insurance acts as a steady safety net for workers who have been consistently contributing to the EPF system. Employees should ensure that their EPF accounts are updated with a valid nomination, as this simplifies the claim process for family members significantly.

Benefit Calculation

The insurance payout is calculated based on the employee's salary and their EPF balance at the time of death. The formula generally involves a calculation based on the average monthly wages over the 12 months prior to death, subject to a wage cap of Rs 15,000. Additionally, it considers a percentage of the average PF balance. The minimum assured benefit under the scheme is Rs 2.5 lakh, while the maximum ceiling is Rs 7 lakh, which includes an enhancement component. These limits ensure that there is a predictable range of financial assistance provided to the nominees.

What To Monitor

The most critical factor for subscribers is maintaining an active EPF account and ensuring that nomination details are current and accurate. An outdated or missing nomination can lead to delays in the claim process, potentially complicating the settlement of the insurance payout for the family. While the scheme provides a helpful layer of security, it is meant as a supplement to other life insurance policies an individual might hold. For employees, verifying that their employer is consistently depositing the required 0.5% EDLI contribution is also a good practice, as it ensures their eligibility remains intact. Claim settlement timelines can vary based on the completeness of documentation, so keeping records in order is essential for a smooth experience.