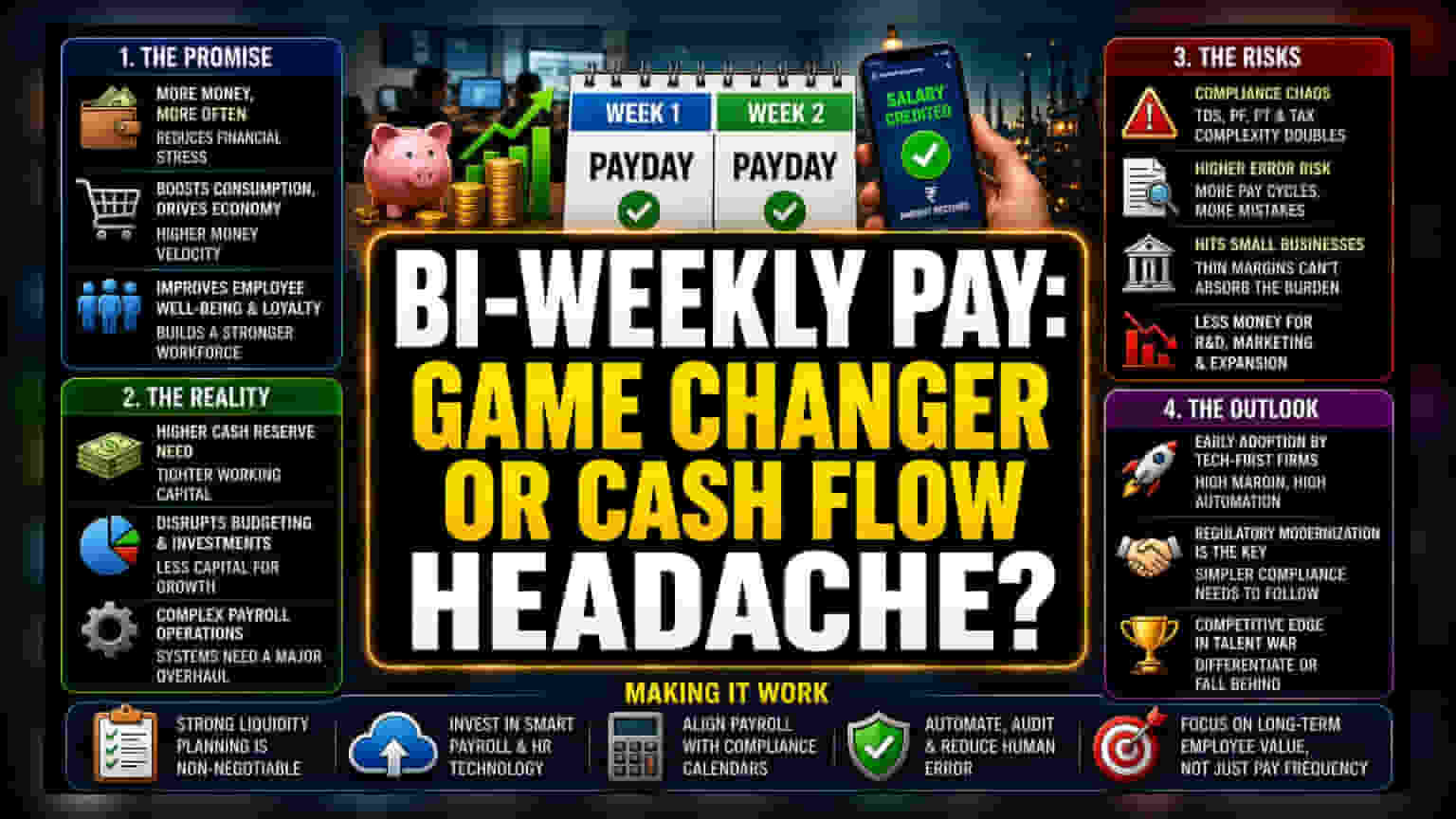

The Operational Friction of Accelerated Payroll

The push to transition away from traditional monthly payout cycles involves more than a mere shift in administrative scheduling; it directly challenges the established working capital management of Indian enterprises. While the moral argument centers on employee dignity and reducing reliance on high-interest credit lines for essential monthly expenditures, the financial architecture behind payroll systems is deeply integrated with monthly accounting and tax compliance cycles. Moving to a bi-monthly system requires a fundamental restructuring of cash flow management, as companies must maintain higher average liquidity to meet obligations twice within a thirty-day window.

The Macroeconomic Paradox

Proponents of the shift argue that increasing the velocity of money in the hands of the workforce will stimulate consumption and provide a meaningful tailwind to GDP growth. However, this perspective overlooks the structural constraints faced by smaller businesses. For many startups and micro-enterprises operating on thin margins, the liquidity required to front-load or split salary payments can disrupt investment in growth initiatives. Analysts note that while larger, cash-rich organizations like Shaadi.com possess the operational flexibility to move payout dates, the broader corporate sector may view the transition as an unnecessary increase in overhead complexity, particularly when automation and payroll software are designed primarily for single-cycle disbursements.

The Forensic Bear Case: Structural Weaknesses

Critics of the proposal emphasize that liquidity management is a zero-sum game for many firms. Accelerating salary disbursements necessitates that companies hold larger cash buffers, which effectively reduces the capital available for R&D, marketing, or expansion. Furthermore, payroll-related compliance—including TDS deductions, provident fund contributions, and professional tax—is synchronized with monthly reporting requirements. Integrating these regulatory obligations into a bi-monthly model introduces significant potential for clerical errors and statutory interest penalties. Without a corresponding modernization of the underlying regulatory and taxation reporting systems, the operational burden of a bi-monthly payroll could negate the intended benefits for all but the largest, most technologically mature organizations.

Future Outlook and Market Adoption

Industry consensus suggests that while the proposal is gaining social traction, adoption will likely remain siloed within the tech-first sector, where high-margin business models can absorb the operational costs of more complex payroll management. Unless systemic regulatory changes occur to simplify the compliance burden of fractional payments, widespread adoption across traditional manufacturing or service-oriented sectors remains improbable. Expect continued discourse on the modernization of workforce compensation, driven by firms looking to differentiate their employer brand in a hyper-competitive talent market.