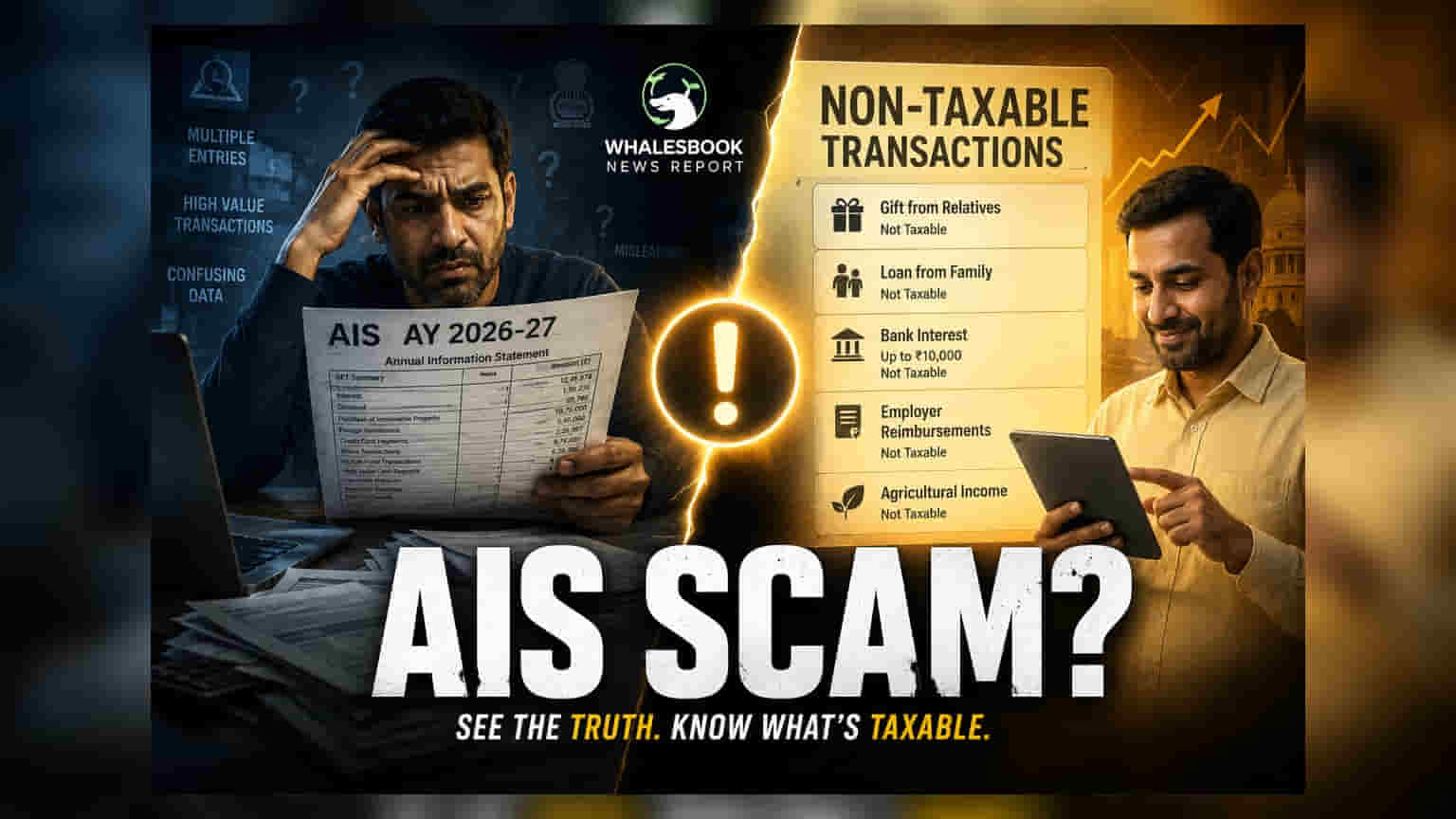

As taxpayers prepare for the AY 2026-27 filing season, many transactions appearing in the Annual Information Statement do not attract tax. Understanding the difference between informational entries and taxable income is essential for accurate ITR reporting and avoiding unnecessary notices from the Income Tax Department.

With the Income Tax Return filing season for Assessment Year 2026-27 underway, taxpayers are increasingly relying on the Annual Information Statement (AIS) to compile their financial data. While this statement provides a comprehensive view of financial activities reported by banks, stock exchanges, and other entities, its presence in the AIS does not automatically imply that the amount is taxable.

The AIS is designed as a transparency tool to help taxpayers reconcile their financial activities with their income tax filings. It captures various financial movements that are meant for informational purposes, allowing the Income Tax Department to track data points across the economy. Before submitting an ITR, it is important for taxpayers to verify which of these entries represent actual income versus those that are merely capital movements or investments.

Distinguishing Investments from Income

Several common financial transactions often trigger reporting in the AIS without necessarily creating a tax liability. For example, the purchase of mutual fund units or shares is considered an investment activity. Taxation only occurs when these assets are sold or redeemed, triggering capital gains or losses. Similarly, opening or closing fixed deposits is an investment action; only the interest earned, rather than the principal amount deposited, is subject to tax.

Savings account activity is another frequent point of confusion. Deposits and withdrawals are standard banking operations that do not represent income. However, taxpayers should ensure their records can explain the source of any large cash deposits if they are flagged for scrutiny. Furthermore, settling credit card bills—even those for high-value purchases—is not considered taxable income, though the reporting allows authorities to monitor high-value consumption patterns.

Exempt Income and Tax Credits

Some entries appear in the AIS specifically because they have been reported by financial institutions, yet they remain tax-exempt. For instance, interest earned on a Public Provident Fund (PPF) account is typically exempt from tax, even though it may be reflected in the statement. Additionally, payments made for advance tax or self-assessment tax appear as credits that the taxpayer will use to offset their final tax liability during the filing process.

Foreign remittances and property purchases also appear in the statement for tracking purposes. In the case of property, the act of purchasing is not a taxable event for the buyer. For foreign funds, the taxability depends on the nature and source of the money rather than the simple act of the transfer. Investors are encouraged to cross-check their own financial records and bank statements against the AIS before filing to ensure that all income is reported correctly, while informational transactions are not mistakenly treated as taxable income.