India's Household Investment in Securities Soars

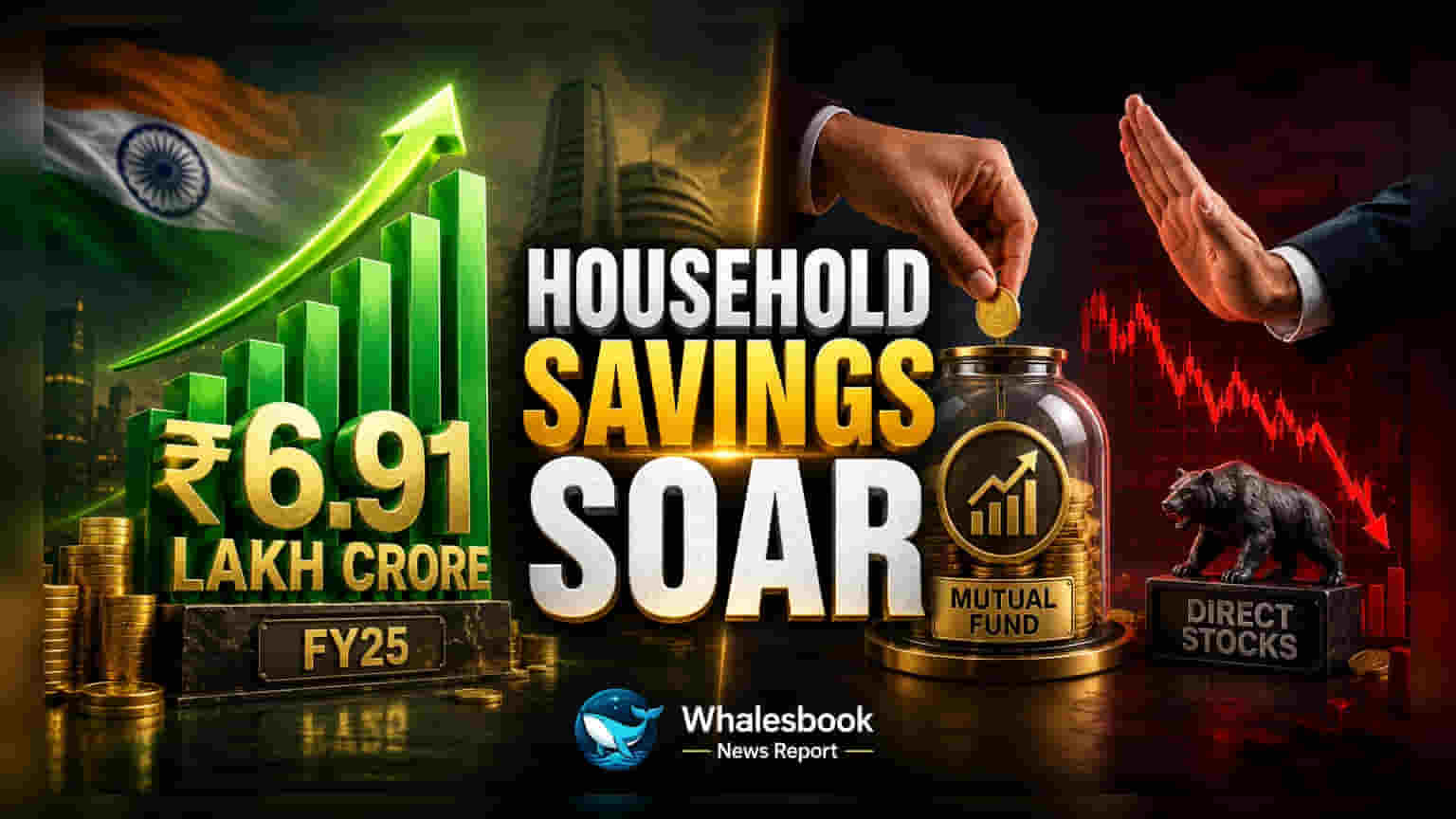

Household investment in India's securities market surged to ₹6.91 lakh crore in fiscal year 2025, nearly doubling from the previous year. This significant increase reflects a major shift in how Indian families are saving, with mutual funds becoming a preferred vehicle for wealth creation over direct equity investments.

Mutual Funds Lead the Surge

Mutual funds were the primary driver of this growth, attracting an estimated ₹5.13 lakh crore in primary market inflows during FY25. This marks a substantial rise from ₹2.85 lakh crore in FY24 and ₹1.66 lakh crore in FY23. The overall primary market saw nearly double the flows, reaching ₹6.31 lakh crore, reinforcing investor preference for professionally managed products. Household mutual fund holdings grew to ₹44.39 lakh crore by the end of FY25, up from ₹36.28 lakh crore a year earlier.

Retail Investors Pare Direct Equity Holdings

Meanwhile, households continued to be net sellers in the secondary equity market for the third consecutive year. Net outflows from direct equity investments totaled ₹54,786 crore in FY25, following outflows of ₹69,329 crore in FY24 and ₹27,684 crore in FY23. This move away from direct stock trading suggests a move toward a more disciplined, long-term investment strategy.

Debt Markets Attract More Interest

Despite net outflows in equity, overall secondary market flows improved to ₹59,452 crore in FY25, compared to ₹818 crore in FY24. This increase was partly due to greater participation in debt markets, which saw household investments exceeding ₹1.04 lakh crore in combined primary and secondary flows for FY25. This indicates a growing interest in stable, fixed-income products amid equity market fluctuations.

Maturing Behavior and Wider Market Reach

Experts view this trend as a sign of maturing retail investor behavior, shifting from speculative trading to disciplined, long-term investing via methods like Systematic Investment Plans (SIPs). Overall capital market participation is also broadening, with 23.5 lakh demat accounts added by December 2025, bringing the total to over 21.6 crore. The mutual fund industry reached 5.9 crore unique investors by December 2025, with 3.5 crore as of November 2025 residing in non-tier-I and tier-II cities. This points to market-linked investments reaching beyond major urban centers.

Financial Deepening and Diversification

The rise in household investment through mutual funds is a key indicator of financial deepening in India. The preference for mutual funds over direct equity signals a greater reliance on professional fund management and a desire for diversification. This is supported by a significant increase in SIP contributions, which hit an all-time high of ₹31,002 crore in December 2025. The growing investment in debt instruments highlights a strategic move towards more stable assets, potentially as a hedge against equity market volatility. The expansion of demat accounts and mutual fund investors into smaller cities suggests greater financial market accessibility, driven by increased financial literacy and digital platforms. Approximately 55%-60% of new SIP registrations come from B30 cities, underscoring this trend.

Concentration and Risk Factors

Despite positive growth, the base of this financialization remains relatively narrow. While mutual fund assets under management are substantial, the investor base is still concentrated among urban and upper-middle-class populations. Rural and lower-income groups continue to favor traditional investments like gold, real estate, and bank deposits. Although direct equity saw outflows, the total value of household equity assets still grew to ₹88.92 lakh crore in FY25 due to market appreciation and primary market participation. This means that while retail investors are reallocating, the equity market is still influenced by factors beyond mutual fund flows. The practice of opening multiple demat accounts for better IPO allotment chances also suggests not all account openings lead to active, long-term investing.

Future Expectations

The trend of households channeling savings into securities, especially through mutual funds and debt instruments, is expected to persist. Increasing penetration into smaller cities and continued growth in SIPs indicate a deepening and broadening of India's investment landscape. A focus on longer-term investment horizons, seen in the rise of longer-term SIPs, suggests a more stable domestic investor base that could help balance foreign portfolio flows in the future.