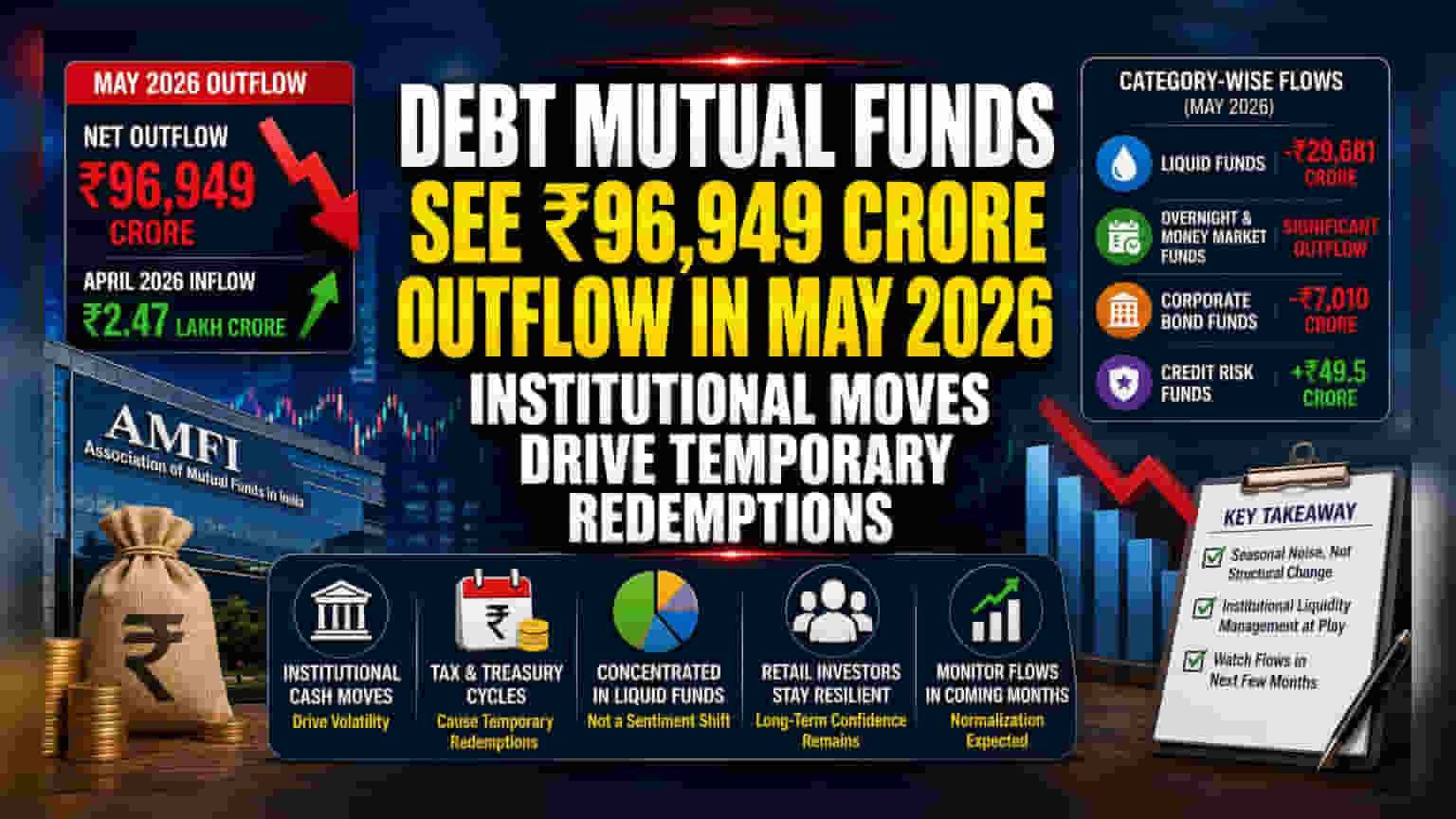

Debt mutual funds reported a net outflow of ₹96,949 crore in May 2026, a sharp reversal from April's strong inflows. While the headline number appears large, market data suggests this is driven by institutional treasury cycles and tax payments, rather than a retreat by retail investors.

What Happened

Debt mutual funds in India recorded a net outflow of ₹96,949 crore in May 2026, according to data released by the Association of Mutual Funds in India (AMFI). This figure marks a significant change from the previous month, when debt schemes attracted substantial inflows totaling ₹2.47 lakh crore. The data shows that the outflow was primarily concentrated in liquid, overnight, and money market fund categories, which are sensitive to institutional cash management needs.

Why Institutional Movement Matters

For an individual investor, a monthly outflow of nearly ₹1 lakh crore might seem concerning. However, the nature of these funds—specifically liquid and money market schemes—is fundamentally different from equity funds. These schemes are the preferred choice for banks, large corporations, and financial institutions to park their excess working capital for very short durations.

Institutional treasury departments often move money in and out of these funds based on their internal liquidity cycles, such as quarterly tax payment deadlines, advance tax outflows, or adjusting their cash positions at the end of financial periods. Because these massive institutional blocks of capital move in unison, they create high volatility in monthly flow data. When these entities withdraw funds to meet statutory payment obligations or operational expenses, it creates a temporary spike in redemption numbers that does not necessarily reflect the long-term sentiment of the wider investor base.

The Performance of Specific Categories

Liquid funds, which typically hold the shortest maturity papers, faced the brunt of the outflows, seeing redemptions of ₹29,681 crore in May. This was a sharp pivot from the massive inflows seen in April. Similarly, corporate bond funds also saw outflows of ₹7,010 crore, reversing their positive trend from the month prior. In contrast, credit risk funds, which invest in lower-rated papers and are generally favoured for slightly longer holding periods, remained relatively stable, recording modest inflows of ₹49.5 crore. This resilience suggests that investors with a slightly longer-term horizon remained committed to their positions, further supporting the view that the large outflows were concentrated in short-term institutional holdings.

How Investors May Read This

This trend is frequently described by market analysts as seasonal noise rather than a structural change in the fixed-income market. When looking at monthly AMFI data, it is useful to separate the 'noise' of institutional treasury cycles from the actual trend of retail participation. If the outflows were driven by retail investors losing confidence, it would likely show up more consistently across various categories, including long-duration gilt or income funds, rather than being concentrated in funds used for short-term liquidity management.

What Investors Should Track

Investors may monitor the data for the coming months to see if the flows normalize as expected once the tax and treasury cycles pass. The key monitorable is not the absolute number of outflows, but whether these movements continue over a sustained period. If the institutional money returns to the system in the subsequent months, it will confirm that the May outflows were merely a result of routine corporate cash management rather than a permanent shift away from debt mutual funds.