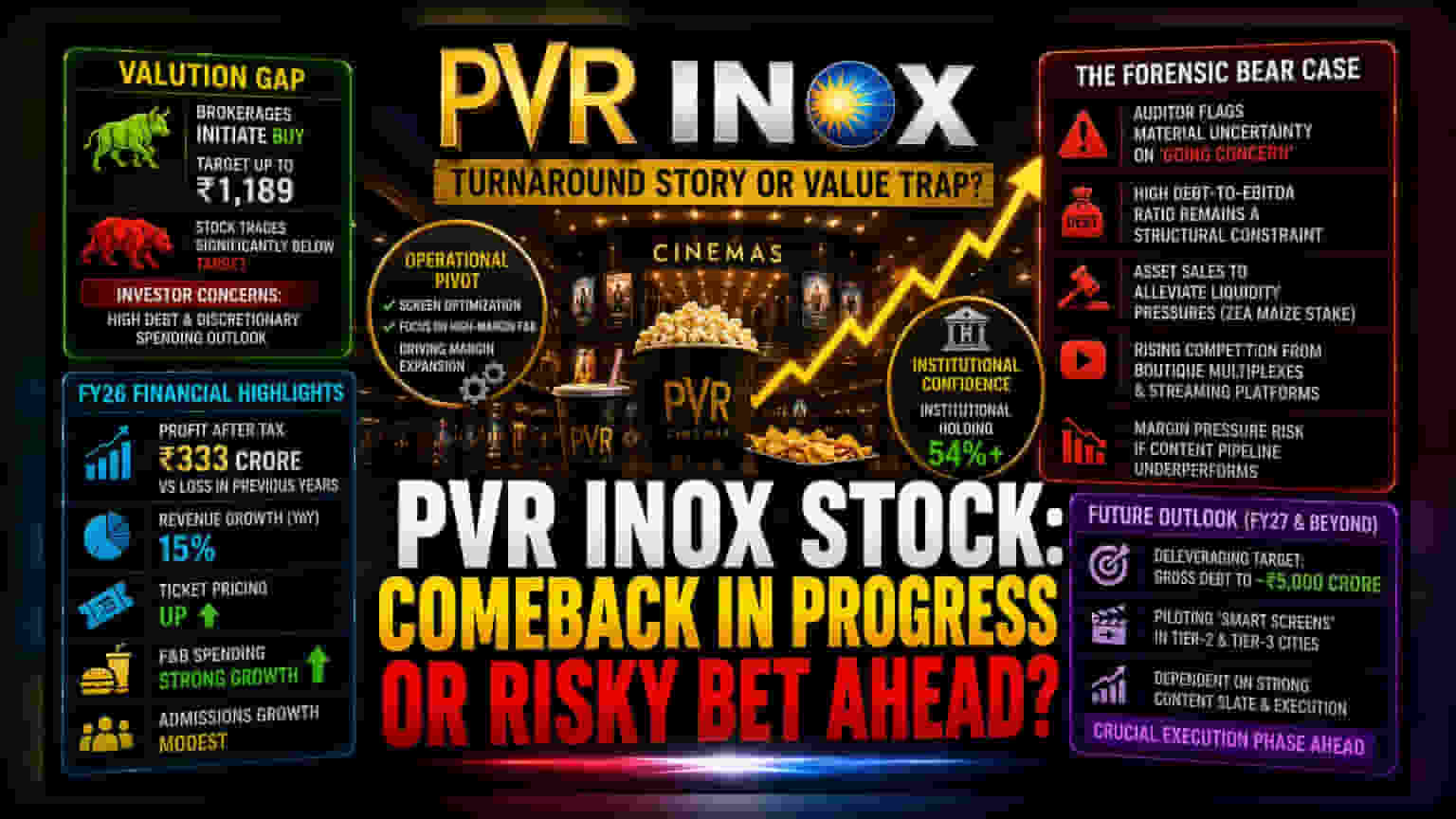

The Valuation Gap

Market sentiment toward PVR INOX remains deeply divided as the company balances a structural turnaround against persistent liquidity concerns. While recent brokerage reports have initiated 'BUY' ratings with price targets reaching ₹1,189, the stock continues to trade significantly below these valuations. This disconnect is largely driven by investor apprehension regarding the company’s heavy debt load and a cautious outlook on discretionary spending, even as revenue metrics show signs of stabilization.

Operational Pivot and Margin Drivers

Financial performance for FY26 highlights a significant operational pivot, with the company shifting from the losses of previous years to a consolidated profit of ₹333 crore. This recovery is underpinned by a 15% year-over-year revenue climb, fueled by an uptick in both ticket pricing and food and beverage (F&B) spending. The firm has successfully optimized its screen footprint and continues to focus on high-margin F&B services, which remain a critical lever for offsetting volatile box office collections. However, growth in admissions remains modest, suggesting that the company is currently relying more on pricing power than on volume expansion to drive top-line growth.

The Forensic Bear Case

From a risk-averse perspective, PVR INOX presents a complex profile that extends beyond traditional valuation metrics. The most glaring headwind is the auditor's recent note regarding material uncertainty surrounding the firm's 'going concern' status. While management has moved to alleviate liquidity pressures through asset sales—such as the divestment of its stake in Zea Maize—the high debt-to-EBITDA ratio remains a structural constraint. Furthermore, the exhibition industry faces increasing competition from both premium boutique multiplexes and the continued rise of digital streaming platforms, which threaten to compress margins if content pipeline performance fails to meet aggressive box office expectations.

Future Outlook and Sector Context

Looking toward FY27, analyst consensus suggests that PVR INOX is moving into a phase of critical execution. With plans to deleverage the balance sheet by reducing gross debt to approximately ₹5,000 million and piloting 'smart screens' in tier-2 and tier-3 cities, the company is attempting to democratize the luxury cinema experience. While institutional holdings remain robust at over 54%, the stock’s performance in the coming quarters will likely hinge on the success of the upcoming content slate and the firm's ability to maintain its margin expansion in a challenging macro-economic climate.