Bollywood's Push for Full Control: Distribution Expansion

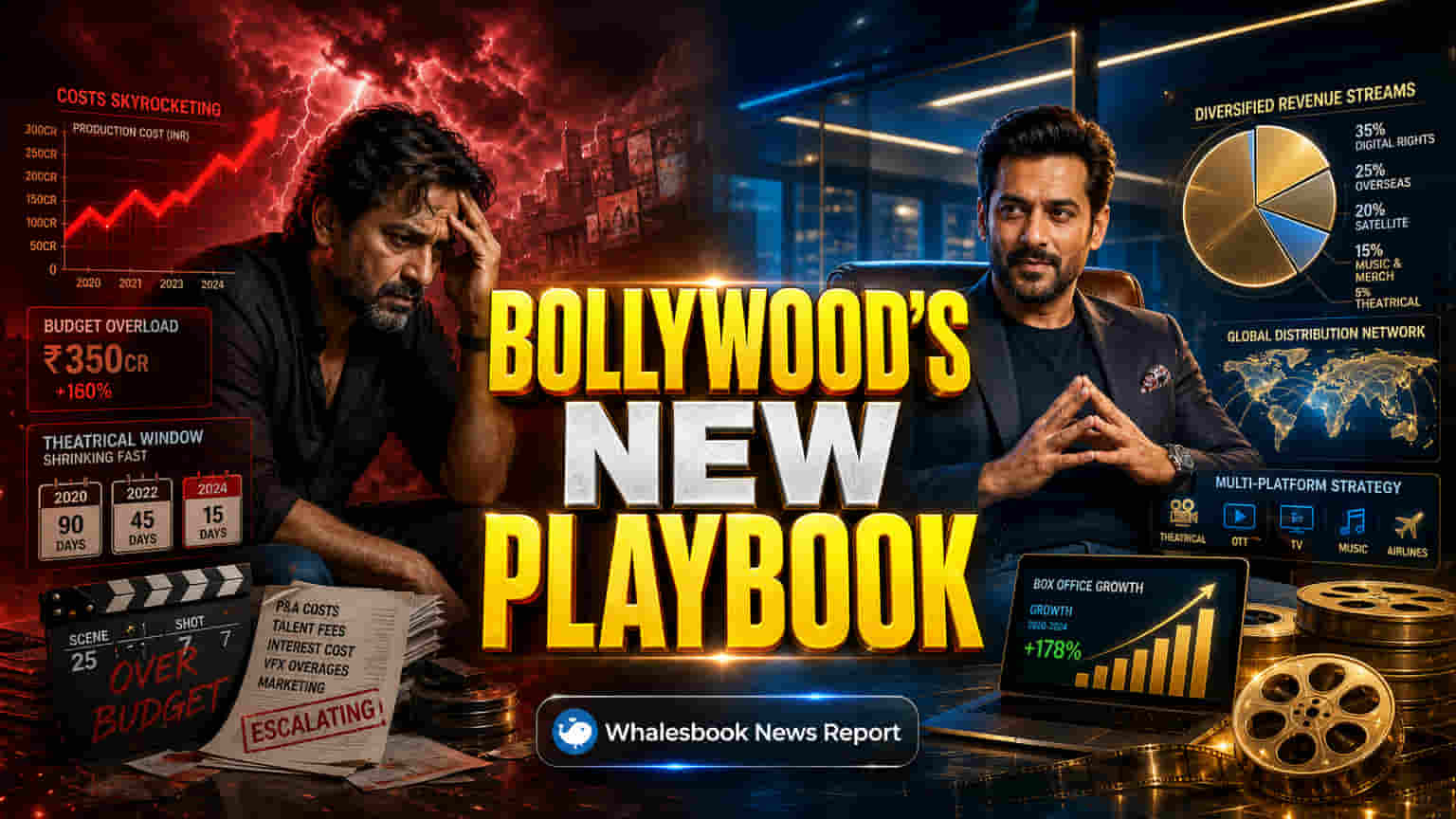

Bollywood production houses are aggressively moving into film distribution. This fundamental shift is driven by rising filmmaking expenses and new revenue models. The move is more than just survival; it's a calculated strategy to gain greater control over the entire film value chain, from creation to audience. By building their own distribution arms, these companies aim to capture a larger share of film revenues. This change comes as India's film industry reached a record ₹13,395 crore in box office collections in 2025. The overall media and entertainment sector grew 9% to INR2.78 trillion that year, with digital media becoming the largest segment, exceeding INR1 trillion for the first time.

Building Integrated Studios: Dharma and Jio Lead the Way

Companies are transforming from traditional production houses into comprehensive studios. Dharma Productions, for example, has hired a Head of Content Acquisition and Film Distribution Worldwide and opened offices in key cities like Delhi, Punjab, Hyderabad, and Chennai to strengthen regional presence and its distribution network. Jio Studios is taking a platform-agnostic approach, linking its content with digital platforms like JioHotstar while also entering theatrical distribution. This ambition to manage financing, marketing, distribution, and licensing allows these firms to keep more intellectual property and revenue. India's strong box office performance supports this, with Hindi cinema contributing ₹5,504 crore in 2025, an 18% year-on-year rise.

Why Distribution Matters: Bypassing Middlemen and Costs

Established players like Yash Raj Films (YRF) already have significant distribution power, partnering with major exhibitors like PVR Cinemas. Other key distributors in the market include AA Films, Pen Marudhar, and Reliance Entertainment. For production houses starting distribution, the main benefit is bypassing sub-distributors, saving commissions that usually range from 5-10% of revenue. Digital tools help centralize operations and provide data for better negotiations with exhibitors on film scheduling and revenue sharing. However, production houses face high capital requirements for distribution, including large spending on prints and advertising (P&A). This can amount to ₹30-80 crore for major releases, often making up 20-30% of the production budget.

Risks Ahead: Consolidation and Capital Demands

Although the move toward integrated studios is clear, significant risks remain. Expanding into distribution requires substantial capital and operational expertise, which could distract from core production strengths. The cinema exhibition market is dominated by consolidated companies like PVR Inox, valued at about ₹9,558 crore and operating 903 screens. New entrants must successfully negotiate with such large exhibitors. In 2025, rising ticket prices combined with fewer audience visits raised concerns about audience volume, even as revenues were high. Relying on blockbuster success for both production and distribution creates a risk of failure at both stages. Companies also face stiff competition from established distributors and potential regulatory changes in the fast-moving media and entertainment sector, projected to reach INR3.3 trillion by 2028.

What's Next: Domination by Integrated Players

The expansion of production houses into distribution is a strategic move responding to market trends that favor integrated operations. With India's media and entertainment sector expected to keep growing, fueled by digital consumption and changing consumer habits, companies that skillfully manage both content creation and distribution are set to capture more long-term value. The shift towards studio consolidation and a focus on building film franchises points to a future where a few strong, integrated players will lead the market.