Under Section 64 of the Income Tax Act, income from assets gifted to a spouse without adequate payment is often taxed in the giver's hands. Known as 'clubbing of income,' this rule prevents shifting assets to lower tax brackets to reduce liability. Investors must understand these provisions and maintain proper records to avoid penalties, as digital tax filing tools now make it easier for authorities to spot discrepancies.

What Is Income Clubbing Under Section 64

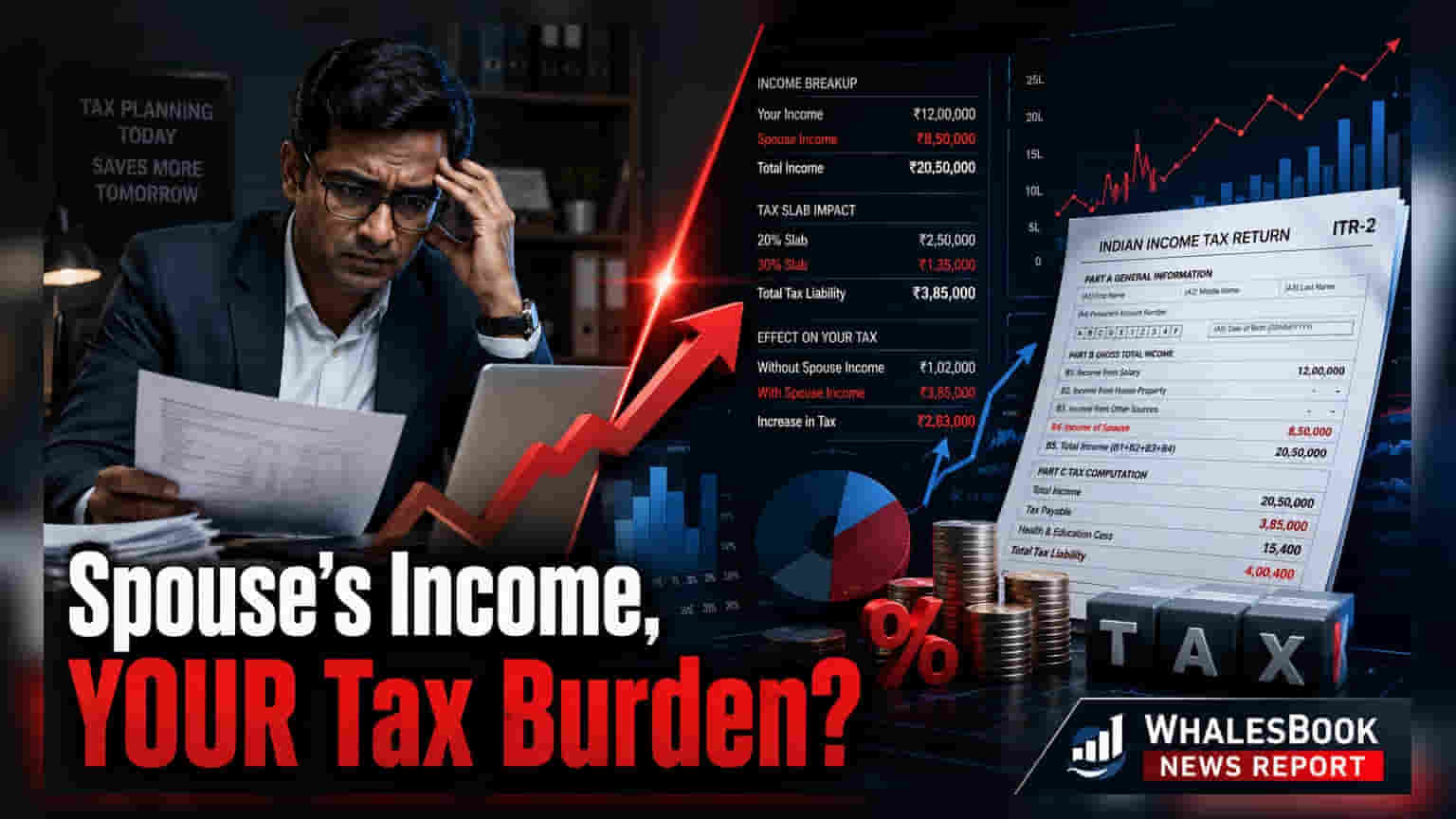

The Income Tax Act includes specific provisions to prevent individuals from lowering their tax liability by transferring income-generating assets to family members in lower tax brackets. This is known as the 'clubbing of income' under Section 64. When you transfer assets—such as cash, property, or investments—to your spouse without receiving 'adequate consideration' in return, the income generated from those assets is legally treated as your own. This means that even if the investment is in your spouse's name, the interest, dividends, or rental income must be included in your tax return.

Which Investments Are Affected

This provision covers a wide range of common financial instruments. If you gift funds to your spouse and they invest that money in fixed deposits, corporate bonds, or mutual funds, the interest or capital gains generated from that specific corpus are subject to clubbing rules. Similarly, if you transfer a house property to your spouse for no payment, the rental income from that property will be added to your taxable income. The primary intent is to ensure that taxes are paid based on the actual source of the investment capital, not just the name on the investment account.

The Importance Of 'Adequate Consideration'

The clubbing provisions generally do not apply if the transfer is made for 'adequate consideration.' This means the spouse pays fair market value for the asset or the funds. If a spouse uses their own independent income or assets to invest, those earnings remain their own and are not clubbed with yours. Furthermore, income earned by a spouse through their own professional qualifications, expertise, or business activities is also exempt from these rules, even if you provided the initial capital for the business setup.

Key Exceptions To Keep In Mind

There are clear scenarios where clubbing rules do not apply. Transfers made before the marriage do not attract these provisions. Additionally, if the transfer occurs while the couple is legally separated or under a formal agreement to live apart, the income is not clubbed. Because tax laws can be complex regarding these exemptions, keeping detailed documentation of the source of funds and the nature of the transfer is essential for every taxpayer.

Why Compliance Is More Critical Now

In recent years, the Income Tax Department has significantly improved its ability to track financial transactions through the Annual Information Statement (AIS) and Form 26AS. These digital tools provide a comprehensive view of interest, dividend, and property income linked to a taxpayer's PAN. If income from gifted assets is not reported correctly, the system may flag the discrepancy automatically. This can lead to notices from the tax department, resulting in additional tax liability, interest charges, and potential penalties for non-disclosure. Maintaining accurate records of all inter-spousal transfers and consulting with a tax professional during filing season can help ensure compliance and prevent future disputes.