The Income Tax Appellate Tribunal has ruled that salaried employees cannot be forced to pay tax again if their employer deducted TDS but failed to deposit it with the government. This decision provides significant relief to taxpayers facing automated tax demands due to TDS mismatches. The ruling reinforces that the legal obligation to deposit deducted tax rests solely with the employer under Section 205 of the Income-tax Act.

What Happened

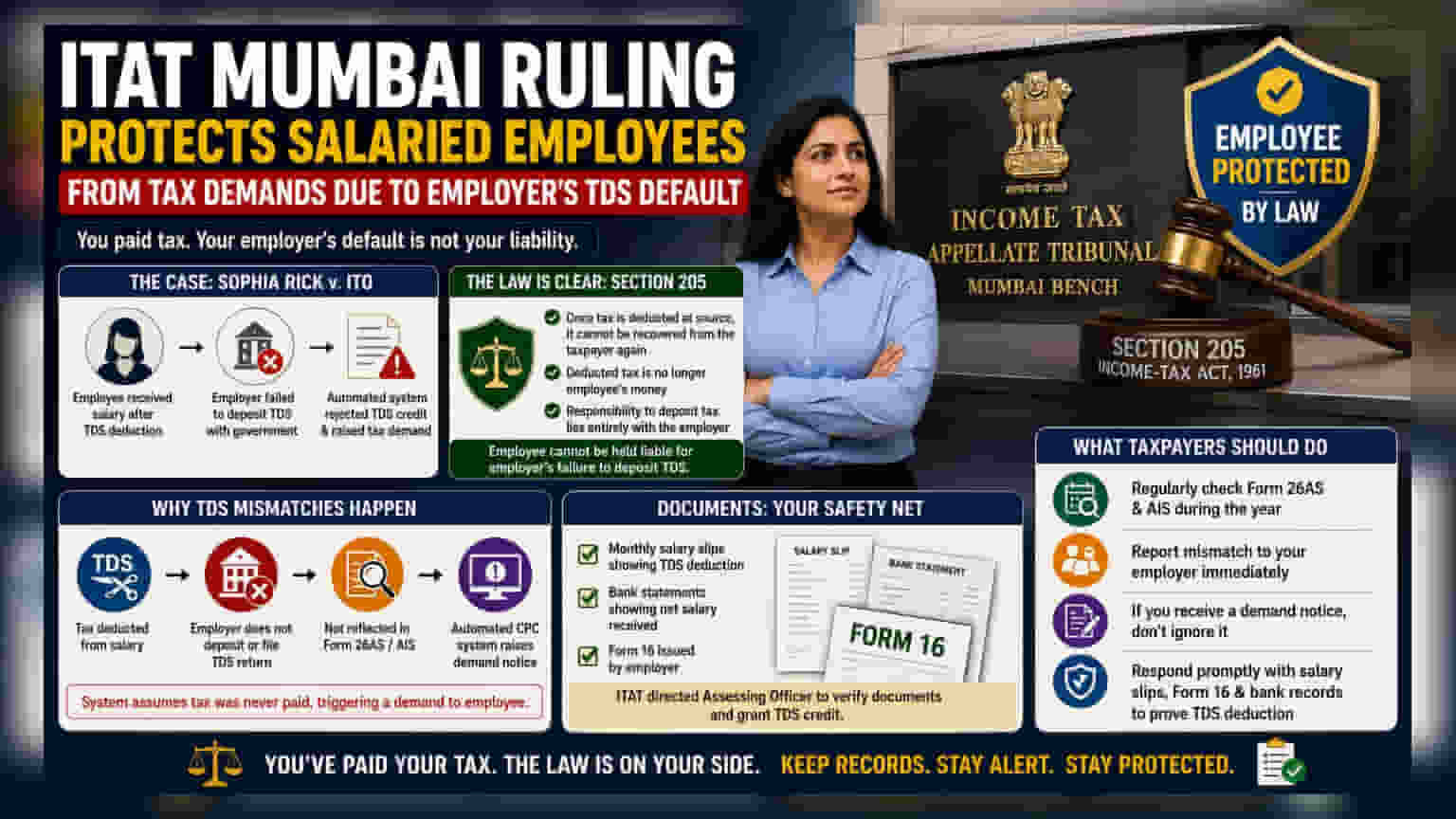

The Income Tax Appellate Tribunal (ITAT) Mumbai has issued a verdict that protects salaried employees from tax demands caused by their employer's failure to deposit Tax Deducted at Source (TDS). The case, involving Sophia Rick v. ITO, centered on a situation where the taxpayer had received her salary after TDS was deducted. However, the Income Tax Department's automated system rejected part of her TDS credit because the employer, M/s Trimax IT Infrastructure & Services Ltd, had not deposited that amount with the government. This resulted in an automated tax demand notice being sent to the employee for the unpaid amount.

The Legal Protection For Employees

The Tribunal’s decision is based on Section 205 of the Income-tax Act, 1961. This section clearly states that once tax is deducted at source, the government cannot recover it from the taxpayer again, even if the employer fails to deposit the funds. The court emphasized that the deducted tax amount is no longer the employee’s money. Once the employer deducts it, the legal responsibility to transfer it to the government lies entirely with the employer. The Tribunal noted that the employee cannot be held liable for the deductor's failure to follow the law.

Why TDS Mismatches Happen

Many taxpayers face automated notices when there is a mismatch between the TDS credit they claim in their income tax return and the data available in their Form 26AS. The Income Tax Department’s Centralized Processing Centre (CPC) runs these checks automatically without human intervention. If the employer has deducted tax from the salary but has not filed the returns or deposited the money, the transaction will not appear in the employee's Form 26AS. Consequently, the automated system assumes the tax was never paid, triggering a demand notice to the employee for the missing amount.

Documentation Is The Employee's Safety Net

While the law protects employees, taxpayers must be prepared to prove their case if they receive a demand notice. The ITAT ruling suggests that proving the tax was deducted is essential. Taxpayers should maintain and be ready to present documents such as monthly salary slips that show the TDS deduction, bank statements reflecting the net salary received, and the Form 16 issued by the employer. The Tribunal directed the Assessing Officer to verify these documents to grant the TDS credit, highlighting that the burden of proof rests on the taxpayer to demonstrate that the deduction occurred.

What Investors And Taxpayers Should Track Next

Taxpayers should regularly monitor their Form 26AS and Annual Information Statement (AIS) throughout the year, rather than waiting until the tax filing deadline. If there is a discrepancy, it is important to communicate with the employer immediately to rectify the filing. If a demand notice is received, taxpayers should not ignore it but instead respond promptly with the necessary salary and bank records to substantiate their claim of TDS deduction.