The Goods and Services Tax Appellate Tribunal has extended its relaxed appeal rules through December 2026. This move reduces the compliance burden on taxpayers by preventing appeal rejections due to minor technical errors, allowing for a focus on the core merits of tax disputes.

What Happened

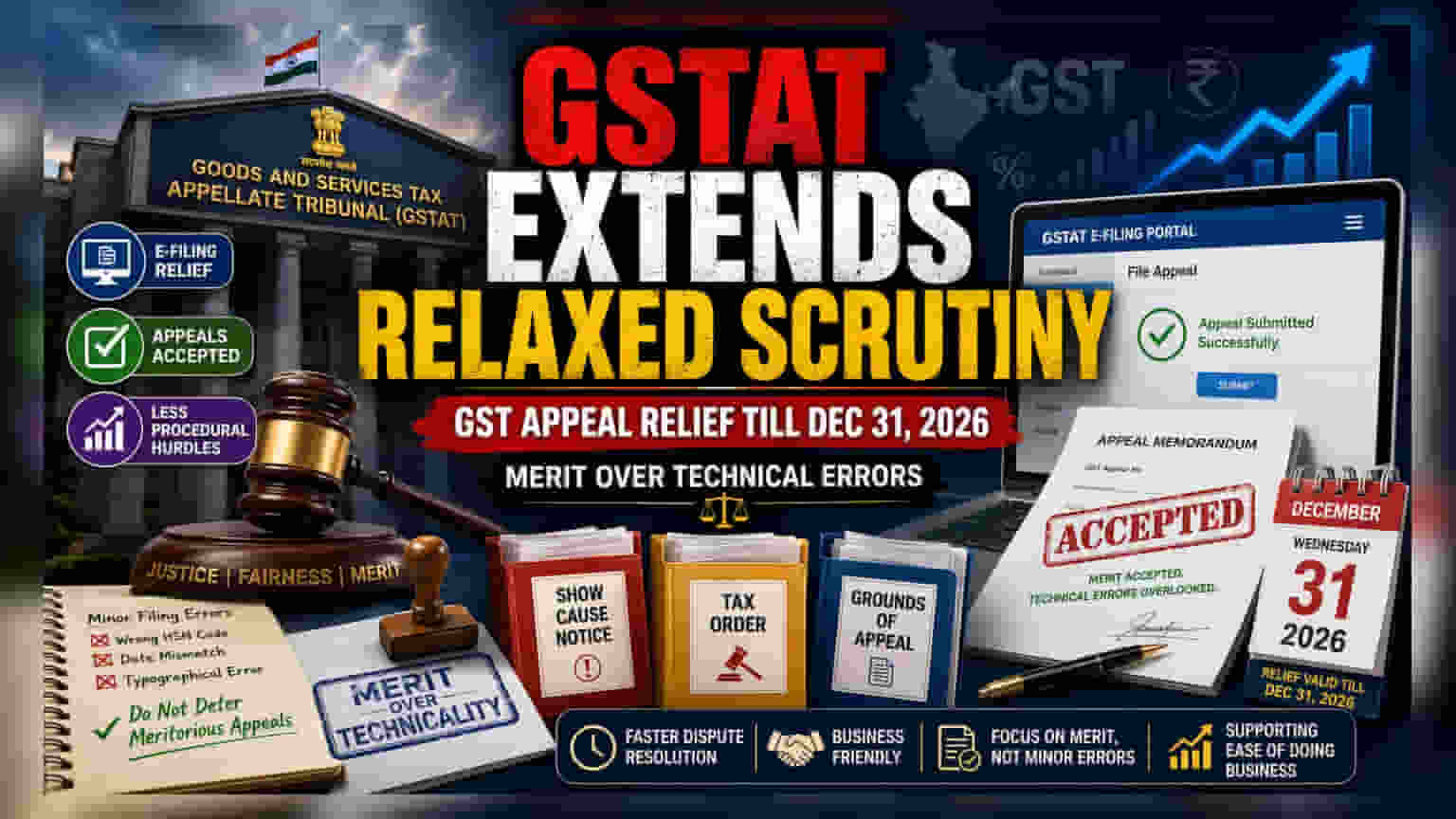

The Goods and Services Tax Appellate Tribunal (GSTAT) has officially extended its relaxed guidelines for tax appeal scrutiny until December 31, 2026. Originally introduced to help taxpayers adapt to the new e-filing system, these rules were set for a shorter duration but will now remain in place for longer. The goal is to ensure that tax appeals are judged based on their legal merits rather than being rejected for minor technical or formatting mistakes.

Why This Matters For Taxpayers

For businesses and individuals, tax litigation can be time-consuming and expensive. By allowing a more flexible approach, the tribunal is ensuring that companies do not lose their right to appeal just because of a small clerical error in the submission process. This is particularly relevant as the tax department continues to transition to a more digitized environment, which can sometimes be difficult for users to navigate during the initial phases.

The Practical Relief

Under the extended rules, scrutiny officers have been instructed to accept appeals that include the necessary core documents—such as the show cause notice, original tax orders, and grounds of appeal—without creating objections for minor procedural gaps. Taxpayers are still required to provide essential items like authorization letters, but the focus remains on the substance of the case over the format. This change gives tax professionals and legal teams more breathing room to align with the online portal’s requirements without the fear of immediate rejection.

What This Means For Business Efficiency

Tax disputes are a common source of uncertainty for many listed companies. When tax tribunals operate more efficiently and focus on substantive legal issues rather than technical hurdles, it helps resolve pending tax cases more smoothly. While this does not change tax law itself, it makes the administrative process of defending a tax position less painful and less prone to delays caused by simple administrative errors.

What Investors Should Track

While this is primarily an administrative update, investors should watch for signs of faster tax dispute resolution in company quarterly filings. If the tribunal system becomes more accessible and efficient, it may help companies resolve long-pending tax liabilities or secure refunds more quickly. The key monitorable will be whether this leads to a reduction in the backlog of GST tax cases in the coming quarters.