Claiming false tax deductions or using fabricated documents may result in penalties of up to 200% and potential criminal prosecution. Taxpayers should be aware that improved data analytics now make it easier for the Income Tax Department to identify discrepancies. Correcting errors through updated returns is a safer approach than facing long-term legal consequences.

Taxpayers who attempt to lower their tax liability through fake deductions or fabricated documentation face severe financial and legal risks. Under the Income-tax Act, the tax department is empowered to impose heavy monetary penalties and initiate criminal proceedings against those found misreporting their income.

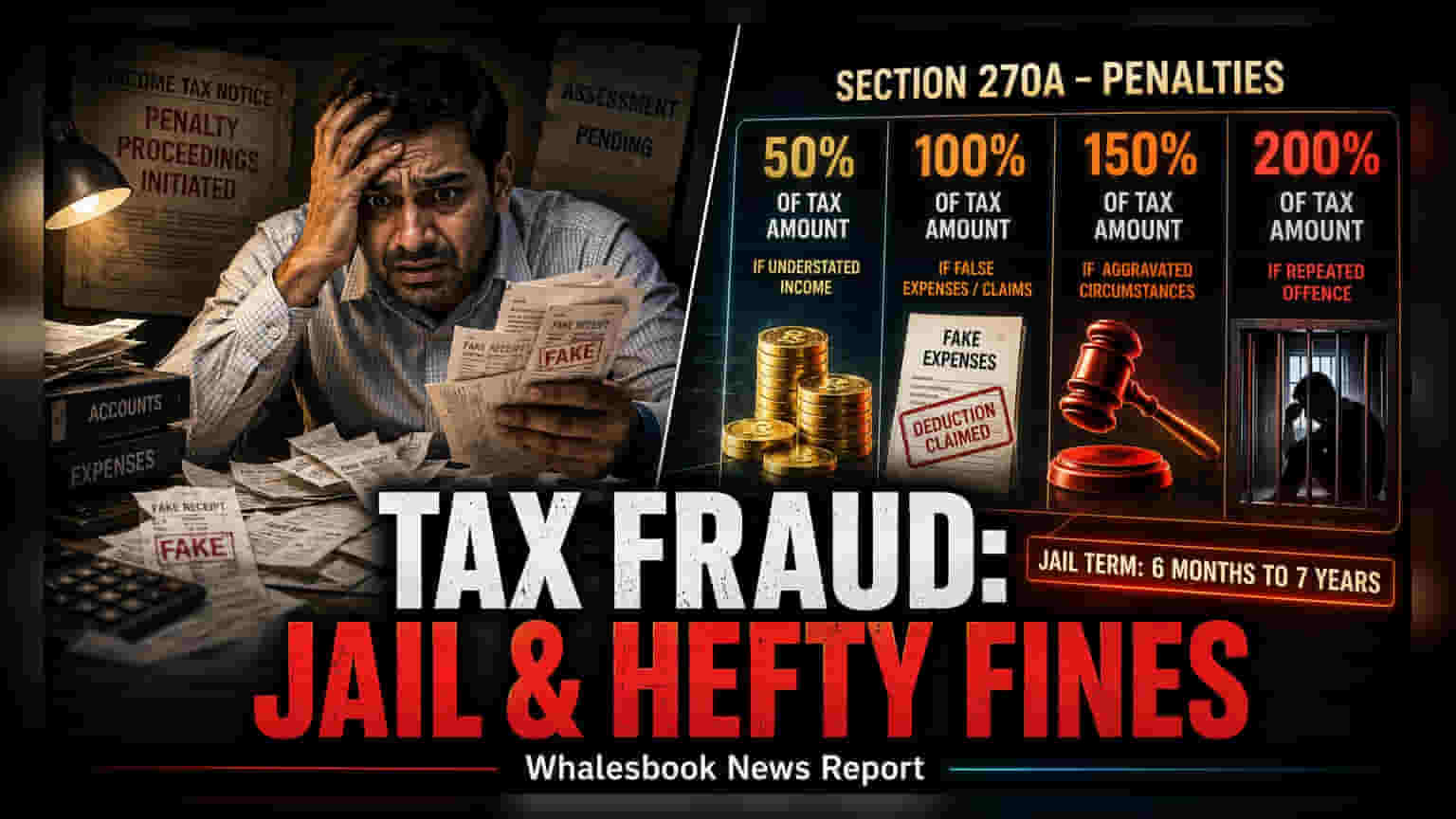

Financial Penalties Under Section 270A

Section 270A of the Income-tax Act provides for penalties ranging from 50% to 200% of the tax payable on under-reported or misreported income. This provision is triggered when a taxpayer fails to disclose full income, records false entries, or claims expenses without any valid supporting evidence. The scope of misreporting includes suppressing material facts, failing to record investments, or neglecting to report international transactions. With the integration of the Annual Information Statement (AIS) and advanced data analytics, the tax authorities now have enhanced capabilities to cross-verify financial data and detect inconsistencies that were previously difficult to spot.

Criminal Prosecution and Legal Consequences

Beyond monetary fines, the use of forged documents or false verification can escalate a tax issue into a criminal matter. Section 276C of the Act deals with the willful attempt to evade tax, which carries a sentence of rigorous imprisonment ranging from six months to seven years. Similarly, Section 277 covers the submission of false statements or verification, with potential jail terms of three months up to seven years. The legal risk extends to those who facilitate such activities, as they may also be held liable under Section 278.

In cases involving the use of forged documents, authorities may also invoke provisions of the Bharatiya Nyaya Sanhita related to forgery and cheating. Furthermore, for instances involving organized fake donation receipts or large cash trails, the Prevention of Money Laundering Act (PMLA) may be applied, which significantly increases the severity of the legal process. It is also important to note that the discovery of fraudulent practices in a single assessment year often prompts the tax department to initiate a reassessment of previous years, creating a compounding legal and financial burden.

Correcting Tax Filings

Given the stringent scrutiny of digital tax records, experts suggest that taxpayers who have inadvertently made errors should prioritize filing revised or updated returns. Voluntarily correcting income disclosures and ensuring all claims are backed by authentic bills and receipts helps avoid the high costs, stress, and potential long-term imprisonment associated with tax evasion investigations. The most prudent step for any individual or business is to maintain transparent and accurate records to withstand the tax department's automated verification systems.