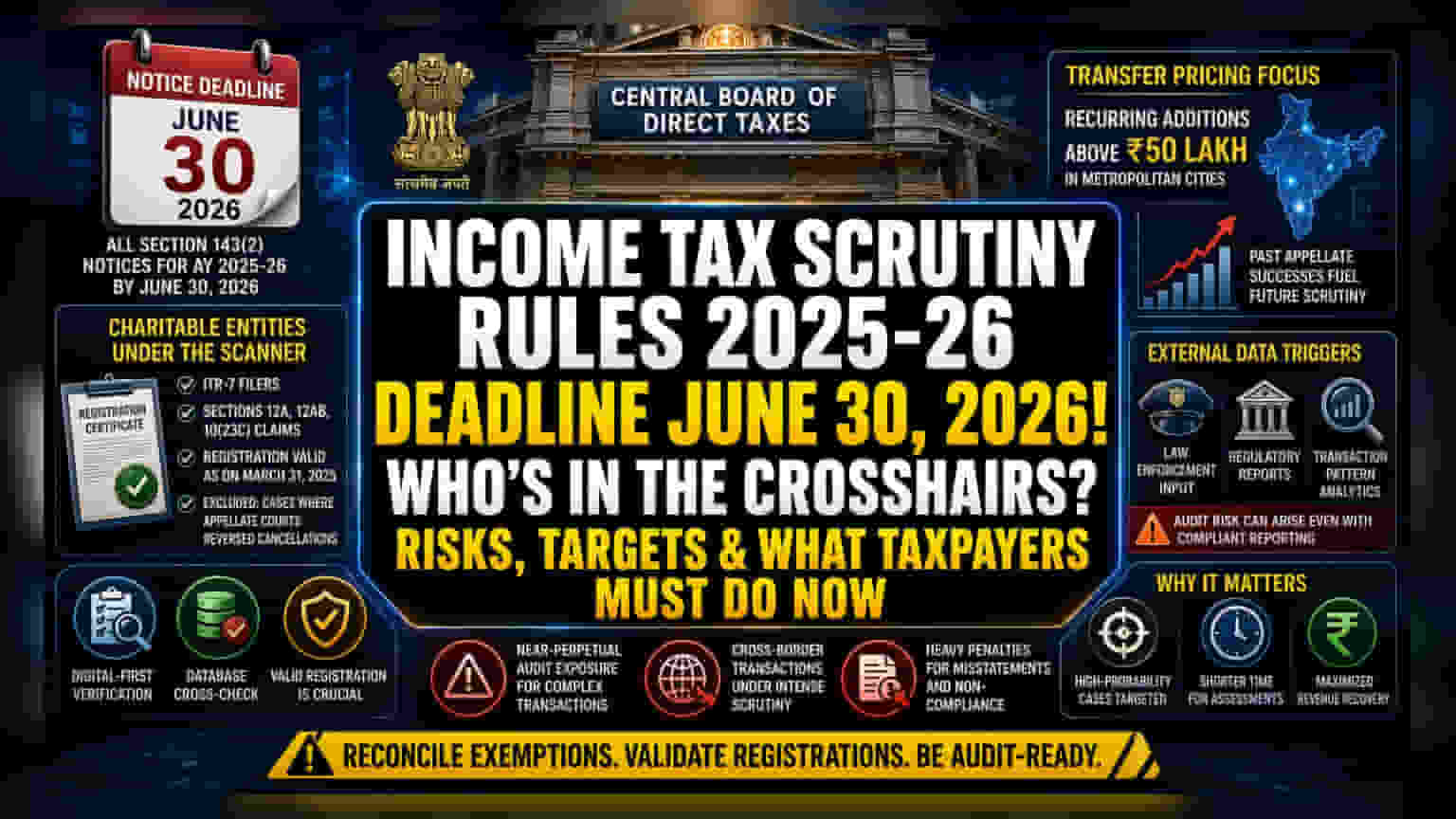

The Compliance Tightening

The recently finalized scrutiny directives from the Central Board of Direct Taxes represent a strategic calibration rather than a policy overhaul. By mandating that all Section 143(2) notices for the 2025-26 fiscal year reach taxpayers by June 30, 2026, the tax authority is effectively compressing its window for administrative intervention. This temporal constraint forces audit departments to prioritize cases with the highest probability of recovery, particularly those involving institutional or high-net-worth entities under the purview of transfer pricing regulations.

Targeting the Exemptions Gap

The mechanism for selecting returns involving charitable entities reflects a shift toward digital-first verification. Entities filing under ITR-7 that assert exemption claims under Sections 12A, 12AB, or 10(23C) face elevated risk if their registration status appears invalidated as of March 31, 2025. This focus on the validity of registration suggests that the tax department is cross-referencing its internal database with annual filings to identify clerical lapses or deliberate avoidance strategies among non-profit entities. The exclusion of cases where appellate courts have reversed cancellations serves as a necessary buffer, yet the operational burden remains on the taxpayer to ensure their registration status is current in the central ledger.

The Operational Bear Case

For corporate taxpayers and sophisticated investors, the primary risk lies in the persistent targeting of 'recurring additions.' The threshold of Rs 50 lakh in metropolitan hubs creates a high-stakes environment for multinational subsidiaries frequently involved in transfer pricing adjustments. Because the revenue department has already achieved success in appellate forums for similar issues, the current scrutiny cycle functions as an automated enforcement tool designed to collect revenue on settled legal interpretations. This creates an environment where companies with complex cross-border transactions face nearly perpetual audit exposure, as the authorities look to replicate past legal victories in subsequent assessment years. The reliance on information from external law enforcement and regulatory bodies also introduces a 'black box' variable, where internal compliance standards may be sufficient for reporting, but external data streams regarding transaction patterns could trigger a mandatory investigation regardless of tax transparency.

Forward Trajectory

While the predictability of these guidelines is marketed as a stabilization measure, it ultimately signals a maturing, automated system that is less reliant on manual selection. Taxpayers should anticipate a more rigid application of these standards as the department leverages advanced data analytics to identify discrepancies between domestic accounting and international reporting standards. The immediate focus for financial departments must be the reconciliation of all exemption claims with valid registration certificates to preemptively mitigate the risks associated with the June 30 notice deadline.