The Judicial Pushback

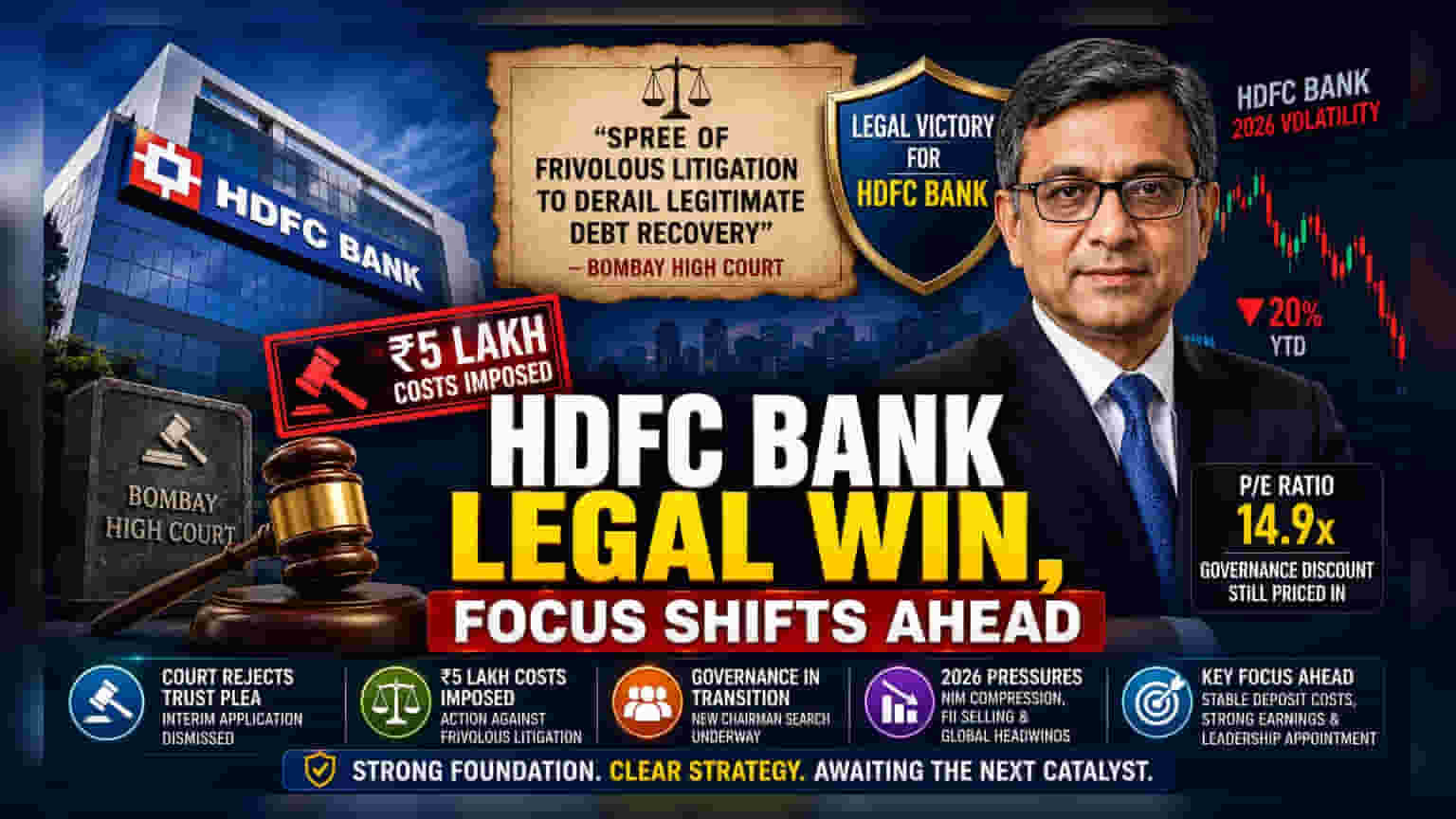

The recent rejection of the Lilavati Kirtilal Mehta (LKMM) Trust’s interim application by the Bombay High Court represents a tactical victory for HDFC Bank. Justice Somasekhar Sundaresan not only denied the request to restrain the bank and its CEO, Sashidhar Jagdishan, from commenting on the dispute but also took the rare step of imposing ₹5 lakh in litigation costs on the trust. The court’s scathing observation—that the trust has engaged in a "spree" of frivolous litigation designed to derail legitimate debt recovery—underscores the judiciary's increasing intolerance for weaponized legal proceedings against financial institutions.

The Governance Context

The bank’s dispute with the trust is a long-running, multi-layered saga that has become a flashpoint for HDFC Bank's broader reputation. While the bank is currently navigating internal governance questions—including the search for a new permanent chairman following the March 2026 resignation of Atanu Chakraborty—this court ruling provides much-needed relief from the "reputational noise" that has dogged the lender. The market has been hypersensitive to such controversies, with the stock seeing significant volatility throughout 2026 as investors weigh these headlines against the bank’s core retail deposit franchise and long-term tech-first institutional strategy.

Structural Vulnerabilities

Despite the legal victory, HDFC Bank remains in a delicate position. The stock has faced a notable correction in 2026, driven by a combination of global macroeconomic tensions, foreign institutional investor (FII) selling, and concerns over net interest margin (NIM) compression. Unlike its peers, which have seen a smoother trajectory, HDFC Bank is still dealing with a "governance discount" that analysts expect will persist until the bank completes its leadership transition and provides clearer evidence of NIM improvement in upcoming quarterly results. The market continues to treat the bank’s valuation—trading at a P/E ratio of approximately 14.9x—as a reflection of this uncertainty, despite the fact that many brokerages still view the core asset quality as highly resilient compared to regional banking peers.

Strategic Outlook

For shareholders, the focus is shifting away from legacy litigation and toward the bank’s ability to stabilize deposit costs. The bank has maintained a robust stance against allegations of impropriety, asserting that its internal oversight mechanisms remain intact. Looking forward, the primary catalysts for a re-rating will be the formal appointment of a permanent RBI-approved chairman and a return to consistent, high-growth quarterly earnings. Until these milestones are reached, the stock is likely to remain in a period of consolidation, with investors balancing the bank's deep-value proposition against the residual risk of further legal or regulatory headlines.