The Valuation Disconnect

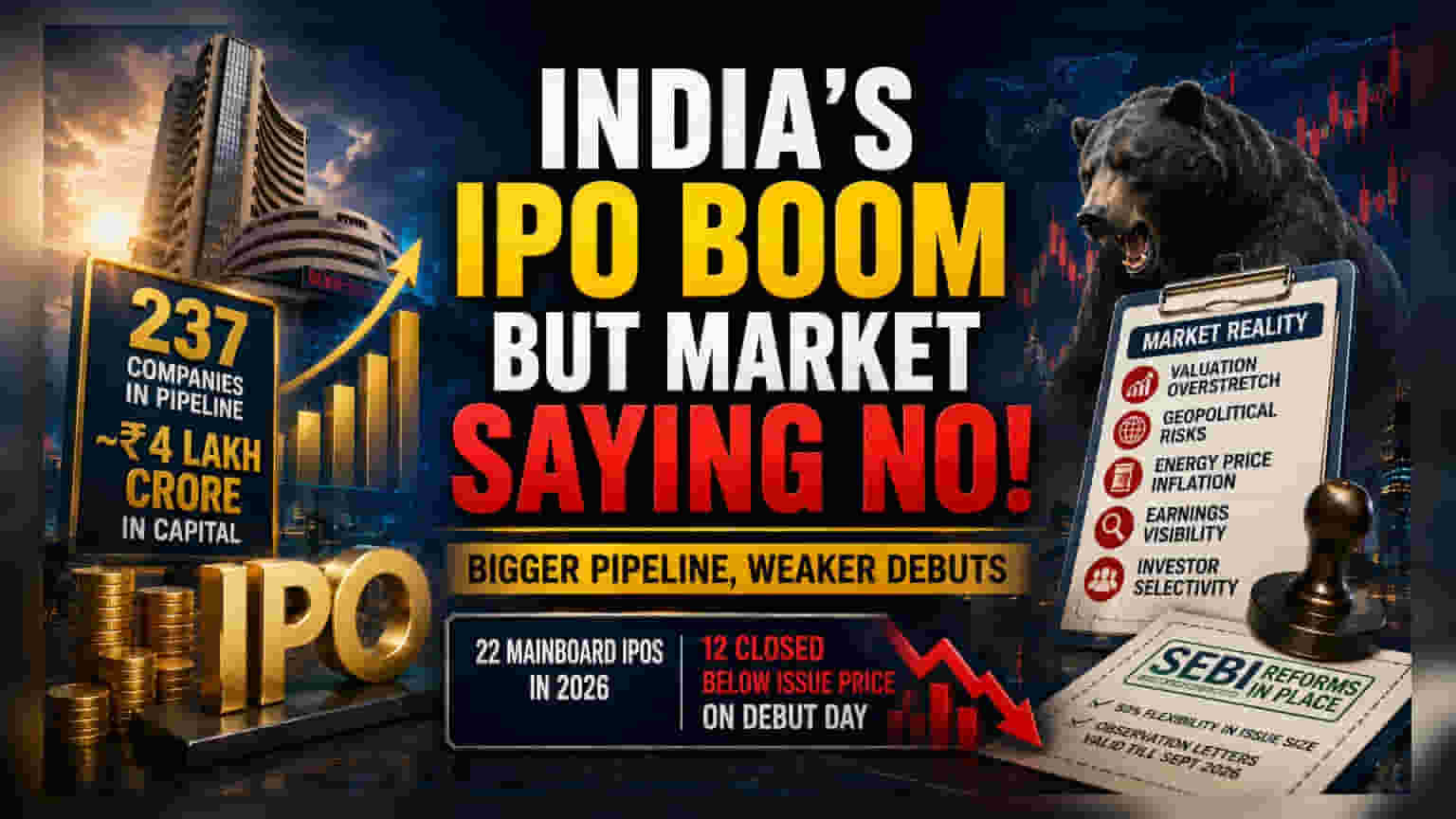

The narrative of a record-setting primary market pipeline—spanning 237 companies and nearly ₹4 lakh crore in potential capital—masks a deepening structural disconnect in the Indian equity landscape. While the sheer volume of filings suggests robust health, the actual market feedback reveals a cooling appetite. Data through June 2026 shows that of the 22 mainboard IPOs launched this year, 12 companies closed their debut session below their issue price. This performance shift marks a transition from the "listing gain" mentality of 2024–2025 to a environment where investors are actively rejecting inflated valuations on day one.

The Shift in Market Dynamics

Market participants are recalibrating their expectations as the era of easy, broad-based IPO premiums faces scrutiny. Unlike previous cycles where retail and institutional liquidity chased almost any new listing, the current environment is defined by selectivity. The surge in the primary market pipeline, while testament to India’s long-term corporate growth, is now meeting a secondary market that is increasingly constrained by geopolitical risks and energy price inflation. With crude prices exerting pressure on domestic inflation and fiscal buffers, investors are prioritizing earnings visibility and valuation comfort over the growth promises often touted in draft red herring prospectuses.

Risk Factors and The Bear Case

The regulatory landscape has attempted to provide a floor to this activity, with the Securities and Exchange Board of India (SEBI) recently allowing a 50% flexibility in issue size adjustments without fresh filings and extending observation letter validity through September 2026. However, these measures serve more as a stabilizer than a catalyst. A significant risk persists: the pipeline is bloated with entities that may struggle to justify their asking prices in a higher-cost capital environment. The current trend of "big fundraising, muted returns" suggests that the market is struggling to absorb the heavy supply of equity, particularly as institutional participants become more risk-averse amid global volatility.

Future Outlook

Moving forward, the primary market is likely to undergo a period of forced discipline. Companies that fail to provide tangible, near-term profitability or those clinging to 2025-style valuation multiples are likely to face either postponement or significant subscription shortfalls. While the structural tailwinds of domestic institutional depth and retail participation remain, they are no longer sufficient to sustain mediocre issues. The coming months will likely see a thinning of the active pipeline as merchant bankers and promoters reconcile with a market that has moved past the phase of uncritical participation.