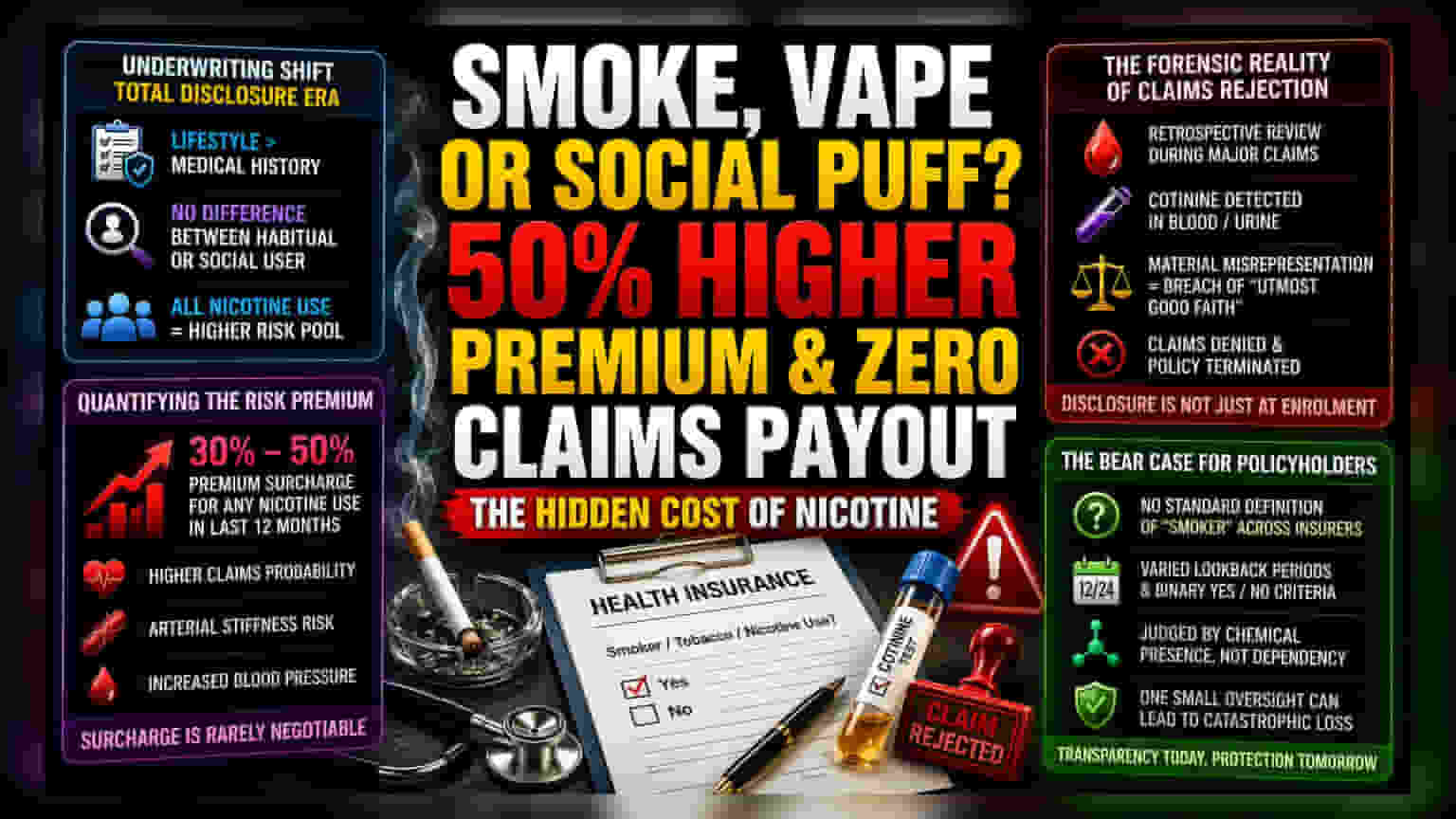

The Underwriting Shift Toward Total Disclosure

The financial barrier to entry for health insurance has moved beyond medical history, settling firmly on lifestyle habits once considered negligible. Modern actuarial models prioritize risk mitigation, leading to a climate where the distinction between a habitual smoker and a social user has virtually evaporated in the eyes of underwriters. This consolidation of risk profiles means that even infrequent nicotine intake frequently triggers the higher-tier premium brackets typically reserved for heavy tobacco users.

Quantifying the Risk Premium

Insurance providers operate on high-frequency data models that penalize variance. When an applicant self-identifies as a smoker, they are subjected to a secondary underwriting process that assesses not just the physical habit, but the long-term potential for chronic respiratory or cardiovascular events. In the current market, the actuarial math often dictates a 30% to 50% premium surcharge for any disclosed nicotine usage within a one-year lookback period. This surcharge is rarely negotiable, as it aligns with the provider’s statistical models regarding the higher claims probability associated with nicotine-induced arterial stiffness and increased blood pressure, even in moderate users.

The Forensic Reality of Claims Rejection

Beyond initial pricing, the true financial threat lies in the post-claim investigation process. Many policyholders mistakenly assume that disclosure is only required at the time of initial underwriting. However, insurers frequently conduct retrospective reviews during significant claims events. If a medical report identifies cotinine—the primary metabolite of nicotine—in a blood or urine panel during a hospitalization, the discrepancy between the initial application and the biological evidence can be classified as material misrepresentation. This constitutes a valid legal basis for insurers to invoke the clause of 'utmost good faith,' potentially leading to the complete denial of coverage and the permanent termination of the policy.

The Bear Case for Policyholders

While insurance companies view these stringent policies as necessary for maintaining the solvency of their risk pools, the lack of a standardized industry definition for a 'smoker' creates structural volatility for the consumer. Some insurers define the term by frequency of use, while others apply a binary 'yes' or 'no' criteria based on any consumption within the preceding 12 or 24 months. This ambiguity acts as a trap for the unwary. Furthermore, the reliance on biological markers like cotinine means that policyholders are being judged by chemical presence rather than clinical dependency. For the insured, this necessitates a rigorous commitment to absolute transparency, as the cost of a minor oversight at the inception of a policy can lead to catastrophic financial losses when a major health event occurs.