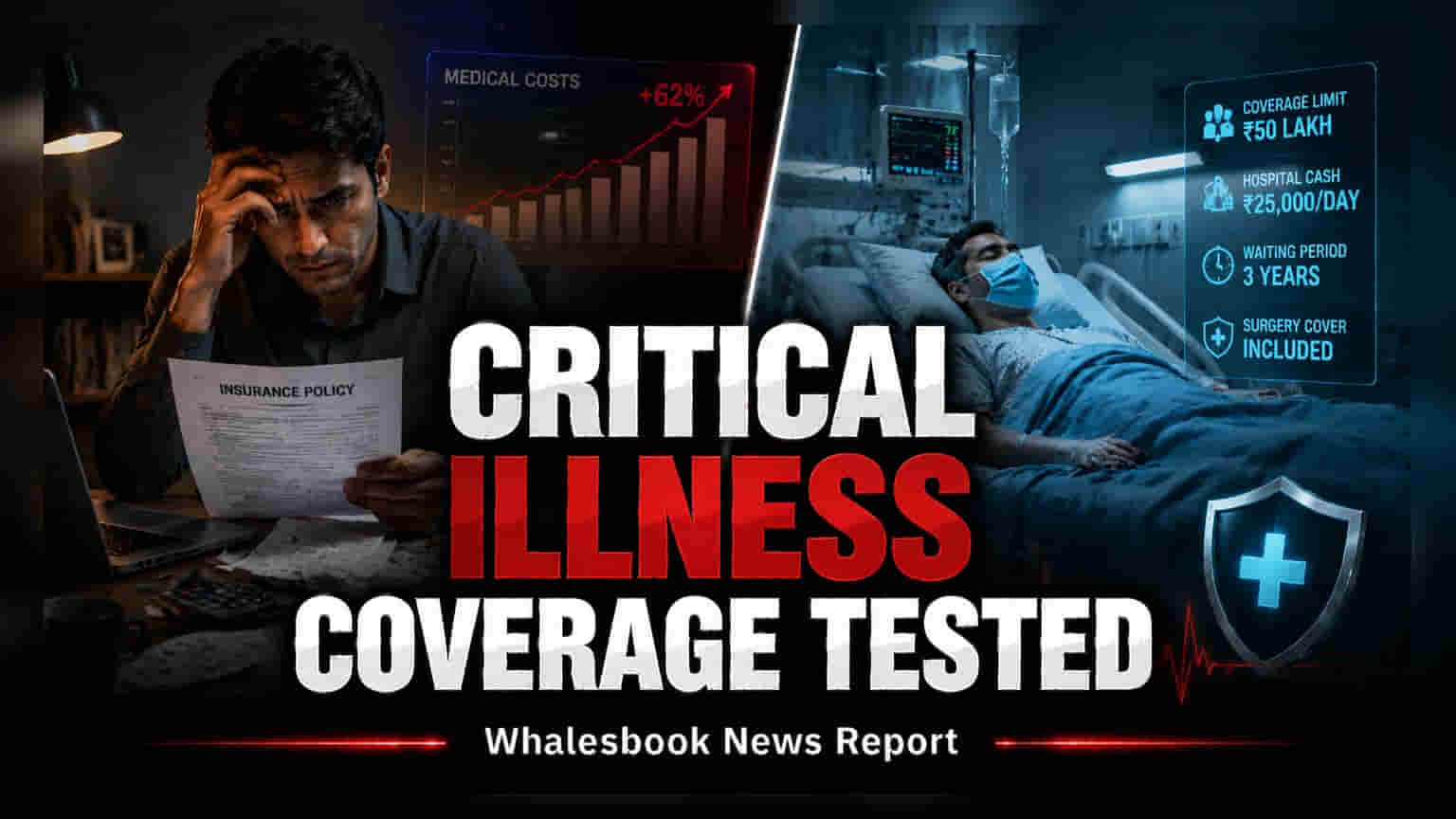

Many health insurance plans carry specific waiting periods and exclusions that can leave policyholders underinsured during major medical crises. Investors and individuals should audit their coverage against rising treatment costs to ensure financial protection. Understanding these policy limitations is essential to avoid unexpected out-of-pocket expenses when they are needed most.

Critical illnesses such as cancer, stroke, heart disease, or organ failure often bring both significant health challenges and heavy financial burdens. While most families hold standard health insurance, many people remain unaware that these policies often have specific limitations regarding how and when critical conditions are covered. Because health insurance products are not standardized in India, every policy document carries unique terms that can impact the final claim settlement.

The Importance of Waiting Periods and Exclusions

One of the most critical aspects of any insurance plan is the waiting period. Many policies do not cover specific illnesses from the very first day. Instead, they require a set duration, often ranging from 30 days to several years, before a claim can be filed for certain conditions. Policyholders should verify their plan's document to understand how long these waiting periods last. Furthermore, policies often contain specific exclusions—conditions or treatments that the insurer does not pay for. Identifying these early is vital to prevent being caught off-guard during a medical emergency.

Evaluating Coverage Adequacy and Scope

It is a common mistake to assume that a policy purchased years ago provides sufficient protection today. With medical inflation significantly increasing the cost of advanced treatments, procedures, and hospital stays, a sum insured that once felt adequate may now fall short of actual costs. Policyholders should regularly compare their existing coverage against current market expenses for critical care. It is also important to verify the exact list of ailments included in the plan. While some comprehensive policies cover a wide range of major conditions, others are much more restrictive. If a specific illness is not listed in the policy schedule, the insurance company is under no obligation to cover the associated expenses.

Next Steps for Policyholders

Instead of waiting for a health crisis, individuals should actively review their policy schedule and terms of service. If a policy is found to be restrictive or insufficient in terms of the total amount provided, speaking with an insurance advisor or the provider about top-up plans or riders is a logical step. The primary goal for policyholders should be to bridge the gap between their existing financial protection and the high costs of modern medical treatment, ensuring that savings are not drained during an unexpected health emergency.