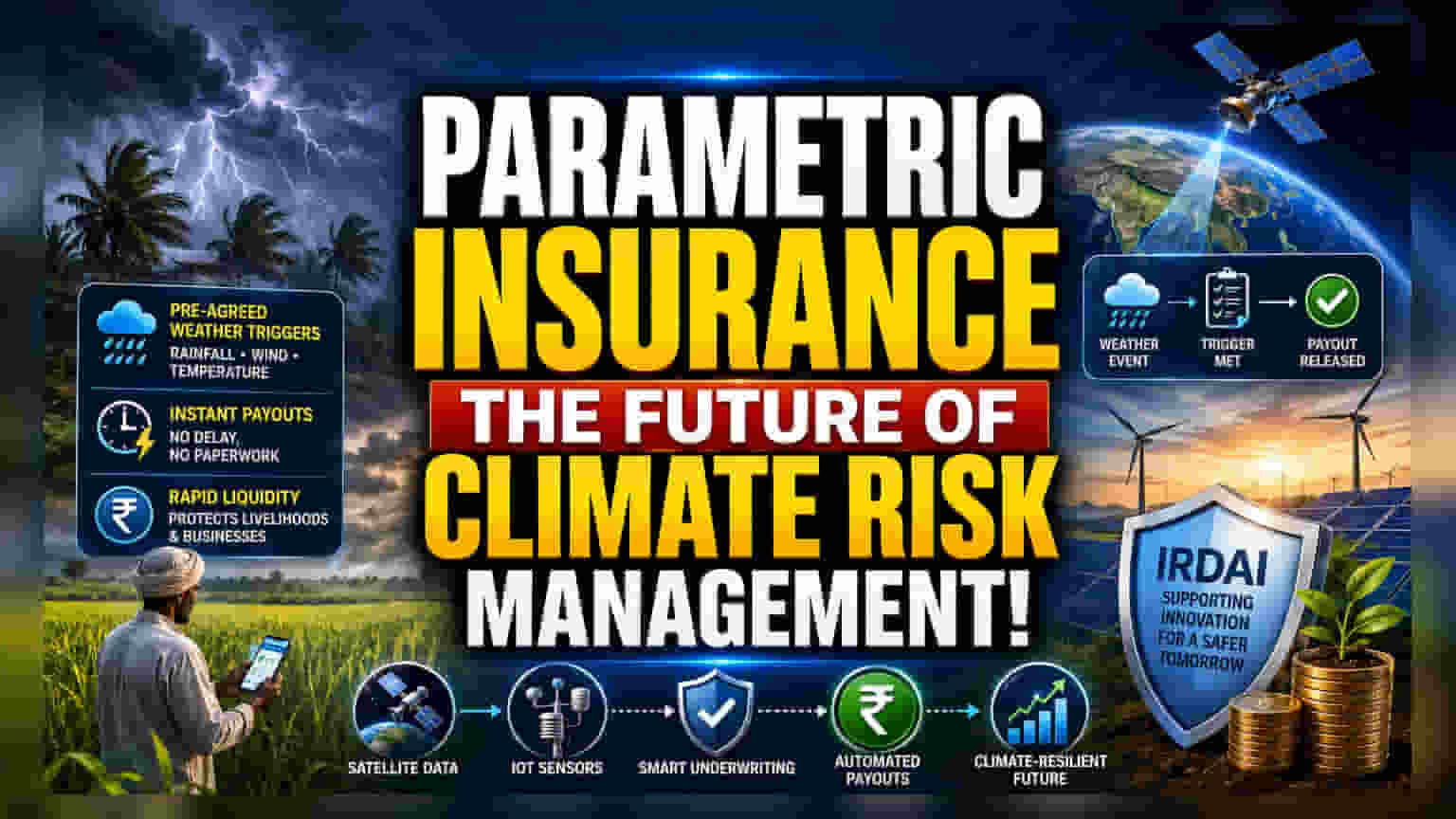

Parametric insurance is gaining traction in India as a fast-payout, trigger-based solution for weather-related financial risks. Unlike traditional policies, it provides swift capital for businesses and farmers based on events like rainfall or wind speed. For investors, this marks a shift in how general insurance companies manage climate risks and reach new markets, though it brings unique challenges like basis risk and the need for high-quality weather data.

What Happened

Parametric insurance is becoming a significant tool in India for managing financial losses caused by extreme weather. Unlike standard insurance policies that pay claims only after a loss adjuster confirms physical damage, parametric insurance operates on pre-agreed triggers. If a specific weather event occurs—such as rainfall crossing a certain threshold or wind speed hitting a defined limit—the insurance company pays a pre-determined amount to the policyholder immediately. This product is designed to provide rapid liquidity to farmers, businesses, and government bodies without the need for a lengthy claims investigation process.

Why This Matters For Investors

The growth of parametric insurance indicates a shift in the Indian general insurance sector toward climate-resilient product design. For insurance companies, this product can help reach untapped markets, such as smallholder farmers or renewable energy projects that are highly sensitive to weather conditions. By automating the payout process, insurers can potentially lower their administrative costs and improve operational efficiency. Investors tracking the insurance space may look at how companies adopt technology to integrate satellite data and IoT weather stations into their underwriting, as these are critical for the accuracy of these policies.

How It Differs From Traditional Insurance

Traditional insurance, often called indemnity-based insurance, focuses on reimbursing the actual loss suffered. This requires a site visit, damage assessment, and negotiation, which can take weeks or months. In contrast, parametric insurance is binary: if the trigger is met, the payout happens. This speed is vital for businesses that face supply chain disruptions or sudden loss of revenue due to events like cyclones or droughts. It acts as a financial buffer, allowing policyholders to manage cash flow immediately after a disaster rather than waiting for a long-drawn-out claim process.

The Role Of IRDAI and Technology

The development of these products is often supported by regulatory efforts to foster innovation. The Insurance Regulatory and Development Authority of India (IRDAI) has been encouraging insurance firms to experiment with innovative products through regulatory sandboxes, which allow for testing new ideas like parametric covers in a controlled environment. Furthermore, the success of these products relies heavily on the quality and accessibility of weather data. The use of advanced analytics, satellite imagery, and localized weather sensor networks is essential to ensure that the triggers are fair and accurately reflect the risks faced by policyholders.

Understanding The Core Risks

While parametric insurance offers speed, it carries a unique risk known as 'basis risk.' This occurs when a policyholder suffers an actual loss from a weather event, but the insurance trigger was not met, meaning no payout is made. For example, a crop might be destroyed by a pest outbreak related to humidity, but if the policy only covers rainfall, the farmer receives no compensation. Alternatively, the trigger might be met, but the payout amount could exceed the actual loss. This risk requires insurance companies to design triggers that are highly correlated with the actual economic impact on the policyholder. Investors should watch whether companies can successfully minimize this gap through better data modeling.

What Investors Should Track

Going forward, the key monitorable is the adoption rate of these products by major insurers and their ability to scale them beyond niche segments. Market participants may also track regulatory updates from the IRDAI that could facilitate wider distribution of these policies. Additionally, the ability of insurers to maintain underwriting discipline and effectively price these products will be critical. As the sector evolves, the performance of these climate-linked products will be an important indicator of how well insurance firms are managing long-term environmental risks and diversifying their product portfolios.