Many parents assume newborns have immediate health coverage, but policies often include hidden waiting periods and treatment sub-limits. Reviewing these clauses before birth is essential to avoid large out-of-pocket medical expenses.

When planning for a new baby, health insurance is often at the top of the checklist. However, a common misconception among many policyholders is that a family floater health plan automatically covers a newborn from the very first day. The reality is that insurance companies have varying terms, and failing to verify these details can lead to significant financial stress during a medical emergency.

Understanding Day-One Coverage and Limitations

Day-one coverage is designed to provide benefits from the baby's date of birth. While this sounds straightforward, it rarely covers every possible medical expense. Most policies are linked to the maternity benefit section of a family floater plan. If a policyholder's plan does not specifically include maternity or newborn benefits, the child may not be covered immediately. It is important to confirm whether the coverage is truly effective from birth or if there is a mandatory waiting period before the infant is added to the policy as a dependent.

Why Congenital Conditions and NICU Stays Matter

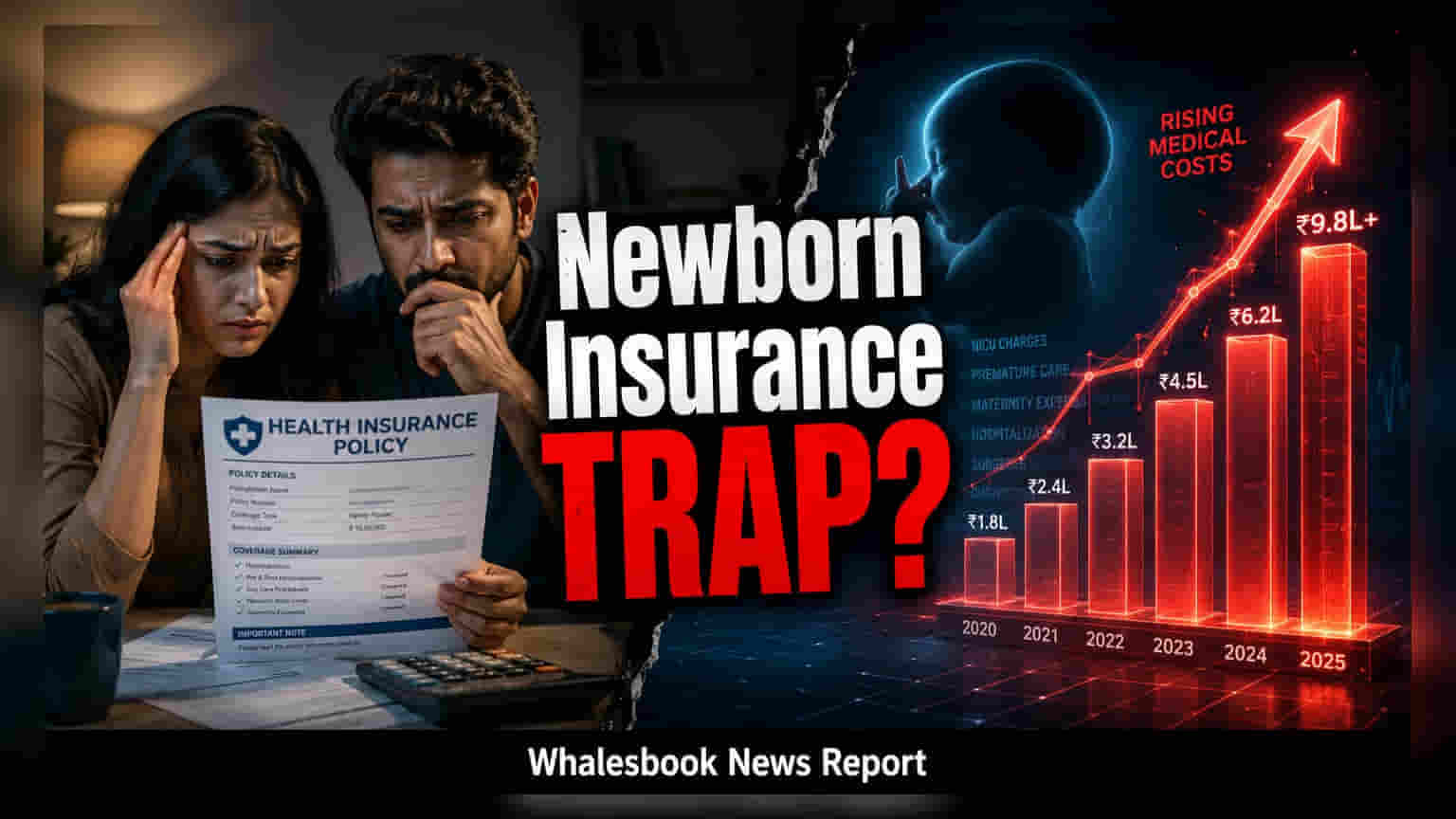

One of the most critical aspects of newborn insurance is the treatment of congenital conditions, which are health issues present from birth. Some policies classify these as pre-existing conditions and may exclude them entirely or impose long waiting periods before they are covered. Additionally, stays in a Neonatal Intensive Care Unit (NICU) can be extremely costly. Many standard family plans have sub-limits, which cap the amount an insurer will pay for specific types of hospitalizations. If the NICU bill exceeds these pre-defined limits, the parents must pay the remaining balance.

Assessing Total Coverage and Policy Exclusions

Parents should also examine the sum assured of their existing family plan. If the plan has a low total limit, the cost of complex neonatal care can quickly exhaust the available cover. Beyond hospitalizations, coverage for routine vaccinations, wellness consultations, and post-birth check-ups often varies by insurer. Policies may explicitly exclude certain procedures or drugs, and these details are usually found in the fine print of the policy document.

Essential Steps for Policy Review

Before finalizing a family health plan, prospective parents should request a detailed explanation of newborn benefits from their insurance provider or agent. Specifically, ask if the plan covers congenital disorders from birth, what the daily room rent or ICU sub-limits are, and if the baby needs to be enrolled within a certain timeframe—such as 30 or 90 days—to maintain continuous coverage. Reviewing these terms early is the best way to ensure that the policy provides the intended financial protection when it is needed most.