MetLife aims to increase its ownership in PNB MetLife beyond the current 49.73 percent, likely by buying shares from minority partners. While PNB MetLife is not a publicly listed company, the move impacts its shareholders, including Punjab National Bank, Jammu & Kashmir Bank, and the Shapoorji Pallonji Group.

What Happened

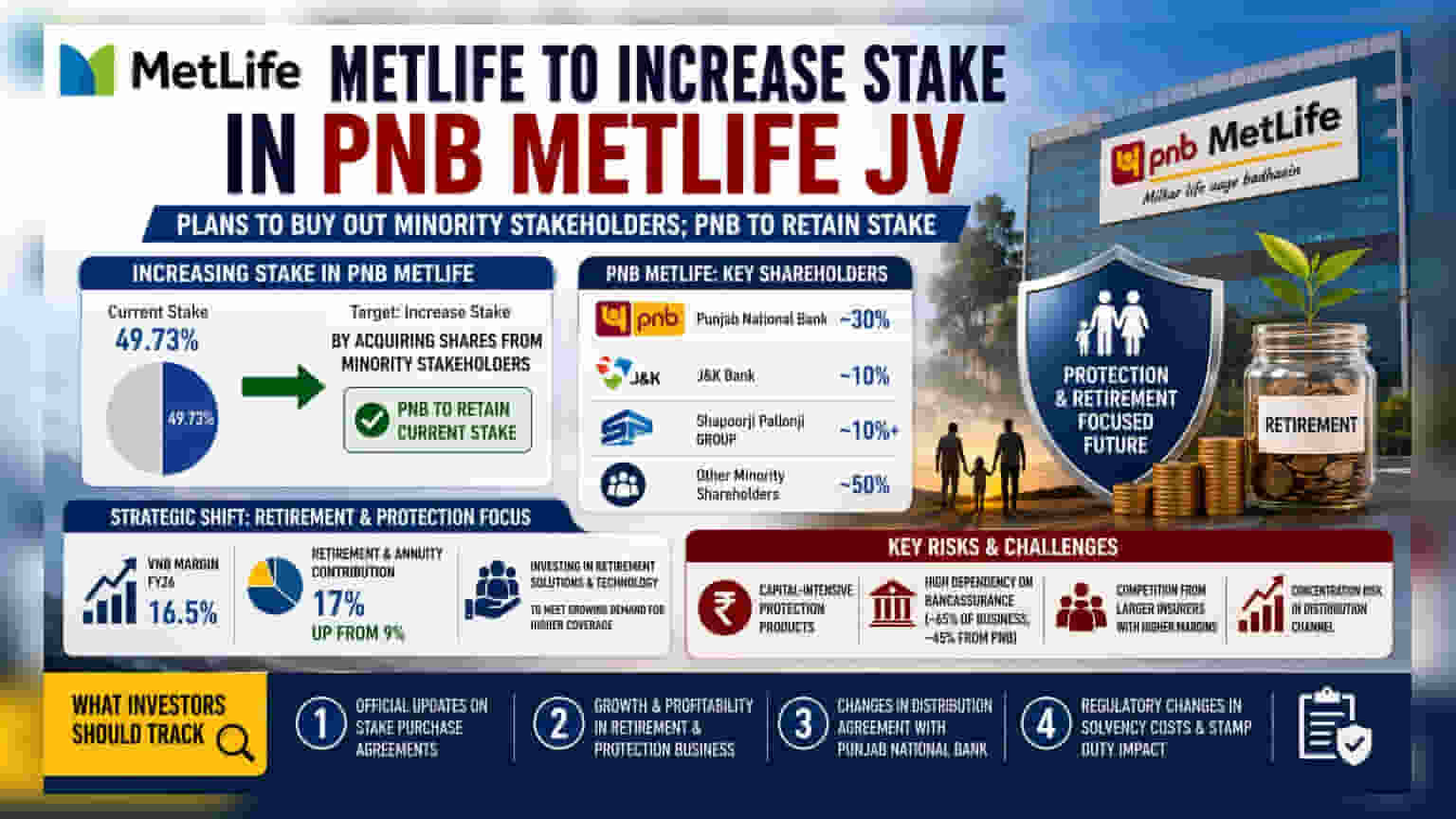

MetLife has announced its intention to increase its stake in PNB MetLife, its Indian life insurance joint venture. The global insurer currently holds a 49.73 percent stake and is looking to raise this figure further. According to managing director and CEO Sameer Bansal, the company plans to achieve this by acquiring shares from existing minority stakeholders. It is expected that Punjab National Bank (PNB), which is the primary Indian partner in the venture, will retain its current shareholding.

Impact on Stakeholders

It is important for investors to note that PNB MetLife is an unlisted company. This means retail investors cannot buy shares of the insurance firm directly on the stock exchange. However, the ownership structure involves several entities, including Punjab National Bank (which holds approximately 30 percent), Jammu & Kashmir Bank, and the Shapoorji Pallonji Group. Any share transfer or stake sale by these minority partners would affect their respective balance sheets and potentially alter the control structure of the joint venture. Investors holding shares in the listed partner banks, particularly Punjab National Bank, may want to watch for official updates regarding any potential stake sale or valuation change.

Strategic Shift to Retirement and Protection

PNB MetLife is currently recalibrating its business model. While the Indian insurance market has traditionally been dominated by savings-oriented products, the company is pivoting toward protection and retirement segments. In fiscal year 2026, the company reported a Value of New Business (VNB) margin of approximately 16.5 percent. Management noted that retirement and annuity products have grown to contribute about 17 percent of the business, up from 9 percent previously. The company is investing in new retirement solutions and technology to support this shift, as it looks to address the evolving demand for higher coverage amounts among Indian customers.

Risks and Business Challenges

The company faces several operational hurdles that are common in the insurance sector. Protection products are capital-intensive, meaning they require significant cash to support the growth. Furthermore, the company remains heavily dependent on bancassurance—the practice of selling insurance through bank branches—which accounts for roughly 65 percent of its total business. Of this, about 45 percent comes solely from Punjab National Bank. This high concentration creates a dependency risk; any disruption in the relationship with the bank or changes in its distribution model could impact the insurance company’s growth. Additionally, the company is competing against larger insurers that currently enjoy higher profit margins, putting pressure on PNB MetLife to improve its cost efficiency and business quality.

What Investors Should Track

For those tracking the broader insurance sector or the parent banks involved, the key monitorables include:

- Updates on any official share purchase agreements between MetLife and minority partners.

- The ability of PNB MetLife to scale its retirement and protection business profitably, as these segments are key to long-term margin improvement.

- Any changes in the distribution agreement with Punjab National Bank, given the high reliance on this single channel.

- Regulatory shifts regarding solvency costs and stamp duty, which could affect the affordability and growth rate of protection products across the industry.