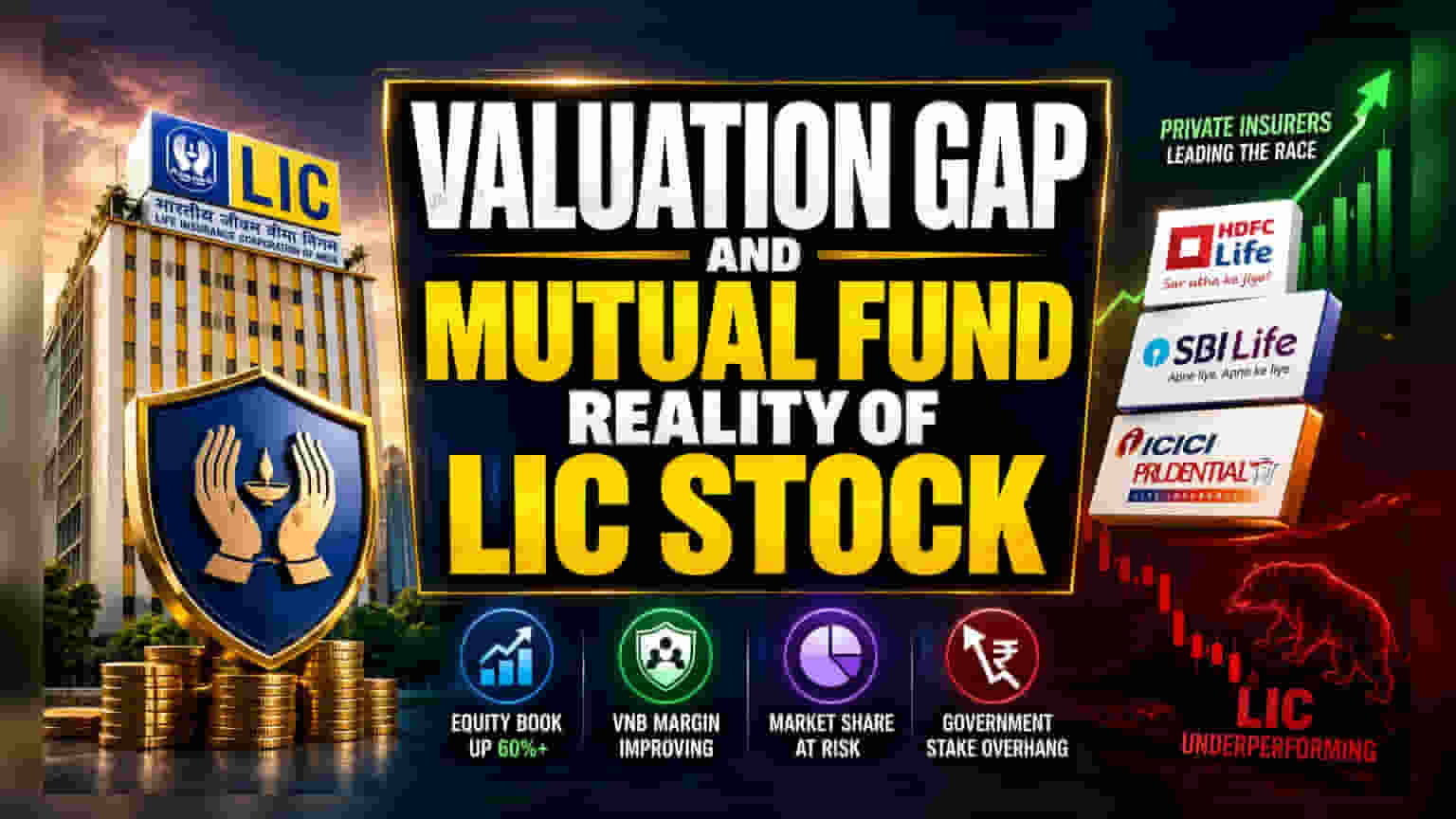

The Valuation Gap

The disconnect between LIC’s swelling investment book and its lackluster market performance reveals a deeper skepticism regarding the insurer's long-term earnings quality. While the value of its equity portfolio expanded by more than 60% over the last four years, the stock has failed to capture the upside of the broader Indian bull market. This stagnation persists despite the insurer’s aggressive efforts to pivot its product mix toward higher-margin, non-participating segments, which are theoretically designed to shrink the valuation chasm between LIC and its private-sector rivals.

Competitive Dynamics and Margin Evolution

Private insurers like HDFC Life, SBI Life, and ICICI Prudential have effectively weaponized the shift in consumer preference toward protection-oriented and unit-linked products, areas where LIC historically maintained a weaker footprint. Although LIC’s Value of New Business (VNB) margin improved to 21.2% in FY26, this metric is still playing catch-up to the industry leaders who have long operated with a leaner, more agile product architecture. The current market pricing suggests that investors are not yet convinced that these structural internal improvements are sufficient to offset the ongoing erosion of overall market share in the premium individual business segment.

The Forensic Bear Case

The primary ceiling on LIC’s valuation remains the constant overhang of potential government stake dilution. Institutional investors remain cautious about the impact of large secondary share sales, which often create a persistent supply-demand imbalance that keeps a lid on price appreciation. Furthermore, the company’s heavy reliance on its massive, legacy participating product portfolio introduces volatility into its earnings, as the insurer must balance competitive interest rates with the need to protect its own margins. Unlike private competitors who can pivot rapidly to specific high-yield niches, LIC’s gargantuan scale often acts as an operational anchor, making rapid adjustments to business strategy a slow and cumbersome process.

Looking Toward a Re-rating

Despite these structural hurdles, the bull case rests on the company’s transition to a more efficient operating model. Trading at roughly 0.8 times its FY28 estimated price-to-embedded value, the stock presents a valuation that is difficult to ignore for value-focused managers. If the company manages to maintain its recent trajectory of expanding VNB margins without further market share loss, the current discount may eventually attract institutional buyers looking for an entry point into India’s financial sector recovery. The path to a re-rating depends entirely on whether the management can prove that its shift in product mix is a permanent structural upgrade rather than a temporary defensive measure.