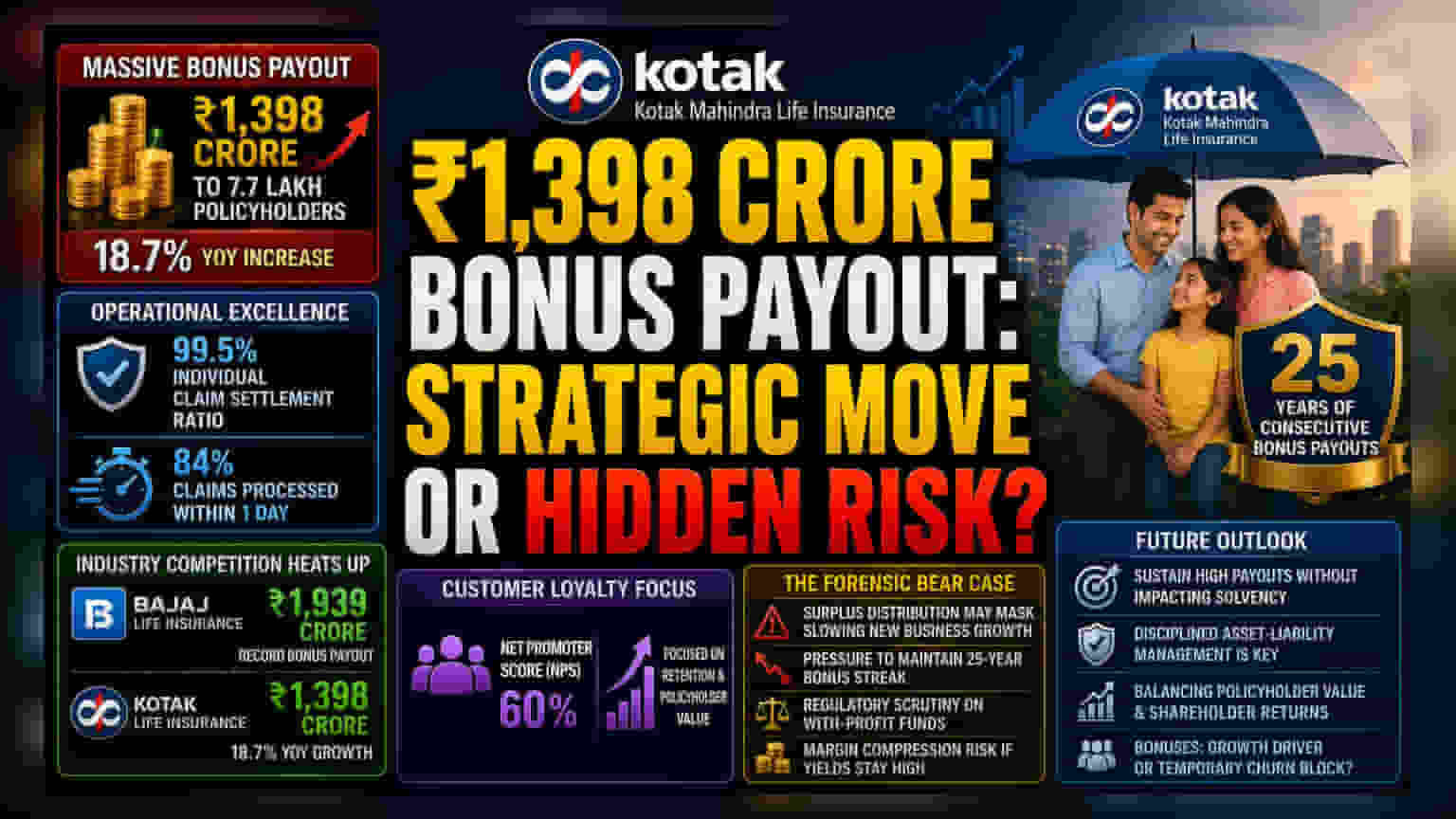

The Capital Allocation Shift

The decision to distribute ₹1,398 crore to 7.7 lakh policyholders represents a strategic move by Kotak Mahindra Life Insurance to solidify customer retention amidst an increasingly crowded Indian insurance market. By increasing its total bonus payout by 18.7% year-over-year, the subsidiary of Kotak Mahindra Bank is signaling confidence in its participating fund surplus. However, the move also reflects the intense pressure life insurers face to maintain competitive yields in a fluctuating interest rate environment where traditional 'with-profit' products compete directly against more dynamic market-linked investment vehicles.

Benchmarking the Surplus Strategy

When viewed alongside industry peers, the scale of this payout underscores a broader race for policyholder loyalty. While Bajaj Life Insurance recently announced a higher record payout of ₹1,939 crore, the relative growth rate of Kotak’s bonus allocation suggests a focused attempt to boost its Net Promoter Score, which currently stands at 60%. Market data indicates that insurers are currently prioritizing high claim settlement efficiency—Kotak’s 99.5% individual ratio—as a primary marketing tool to differentiate themselves from smaller players who may struggle with operational bottlenecks. This operational speed, where 84% of claims are processed within one business day, acts as a critical moat against aggressive competitors that lack equivalent digital infrastructure.

The Forensic Bear Case

Investors monitoring the parent company, Kotak Mahindra Bank, should maintain a critical view of these insurance-side distributions. Aggressive bonus declarations, while positive for customer sentiment, can sometimes mask a strategy of using surplus distribution to drive new business growth in a slowing market. If the underlying participating fund faces volatility or if the bank requires additional capital for its broader financial services expansion, the pressure to maintain this 25-year streak of consecutive bonuses could eventually lead to margin compression. Furthermore, as regulators increase oversight on solvency margins and transparency in 'with-profit' funds, insurers may find it increasingly difficult to balance shareholder dividends with the rising expectations of policyholders for higher bonus payouts.

Future Outlook and Sector Dynamics

The reliance on legacy participating products remains a double-edged sword for Kotak Life. While these products provide steady inflows and a captive customer base, they tether the insurer to long-term liabilities that require disciplined asset-liability management. As the fiscal year progresses, industry consensus remains focused on whether insurers can sustain these high payout levels without sacrificing the solvency buffers needed to navigate potential macroeconomic downturns. Policyholder value is currently being prioritized, but the ultimate test will be whether these distributions drive sustainable long-term business growth or merely function as a temporary mechanism to suppress churn.