Many policyholders face unexpected medical bills due to overlooked clauses like room rent limits and co-payment terms. Understanding your insurance policy details before a medical emergency occurs is essential to avoid large out-of-pocket expenses.

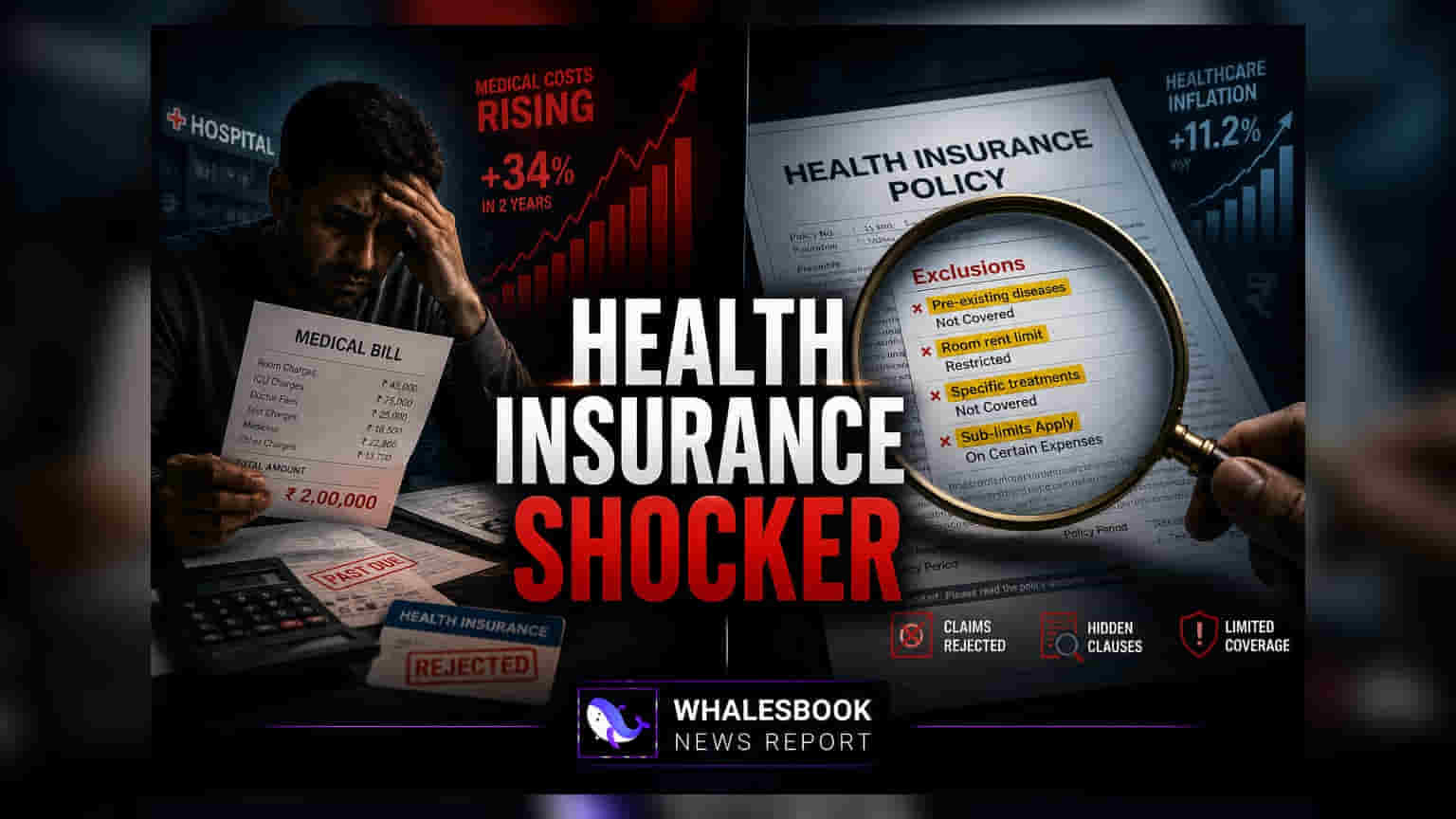

Health insurance is often viewed as a complete safety net for medical emergencies, but many families encounter significant financial stress when they realize their policy does not cover the full cost of treatment. This gap between expectation and reality often stems from complex policy language that many policyholders do not fully review until they are already in a hospital.

The Impact of Room Rent Limits

One of the most common reasons for unexpected costs is the room rent limit. Many insurance plans impose a cap on the daily room rent. If a patient chooses a room that exceeds this limit, the insurer may not only charge the difference in rent but also apply a proportional deduction to the entire hospital bill. This means that if the room rent is higher than the allowed limit, the coverage for doctor fees, medicine, and other services may also be reduced, leading to a much larger bill for the patient than anticipated.

Understanding Co-Payment and Deductibles

Many policies include a co-payment clause, which requires the policyholder to pay a fixed percentage of every claim. While these plans often come with lower annual premiums, they create a recurring out-of-pocket expense during every hospitalization. Similarly, some plans have a deductible, which is a fixed amount the insured must pay before the insurance company begins to cover any costs. Ignoring these clauses can lead to surprise bills during a time of financial and physical stress.

Navigating Waiting Periods and Exclusions

Insurance policies frequently contain waiting periods for pre-existing conditions or specific illnesses. If an emergency occurs for a condition that is still within the waiting period, the claim may be fully or partially rejected. Furthermore, every policy includes a list of exclusions—procedures, treatments, or conditions that the insurer simply does not cover. Cosmetic surgery, certain dental procedures, and experimental treatments are common examples. Patients who assume all hospital expenses are covered often find themselves responsible for these non-medical or excluded items.

Claim Process and Network Hospitalization

The choice of hospital plays a major role in how claims are settled. Receiving treatment at a hospital that is not part of the insurer’s network often means the patient must pay the bill upfront and seek reimbursement later. This process can be delayed if documentation is incomplete or if the insurer requires clarification on the treatment provided. Keeping digital and physical copies of the policy, understanding the cashless hospitalization process, and notifying the insurer immediately upon admission can help streamline the claims experience. Regularly reviewing the policy document and discussing coverage terms with an insurance advisor before a medical crisis is the best way to manage these financial risks.