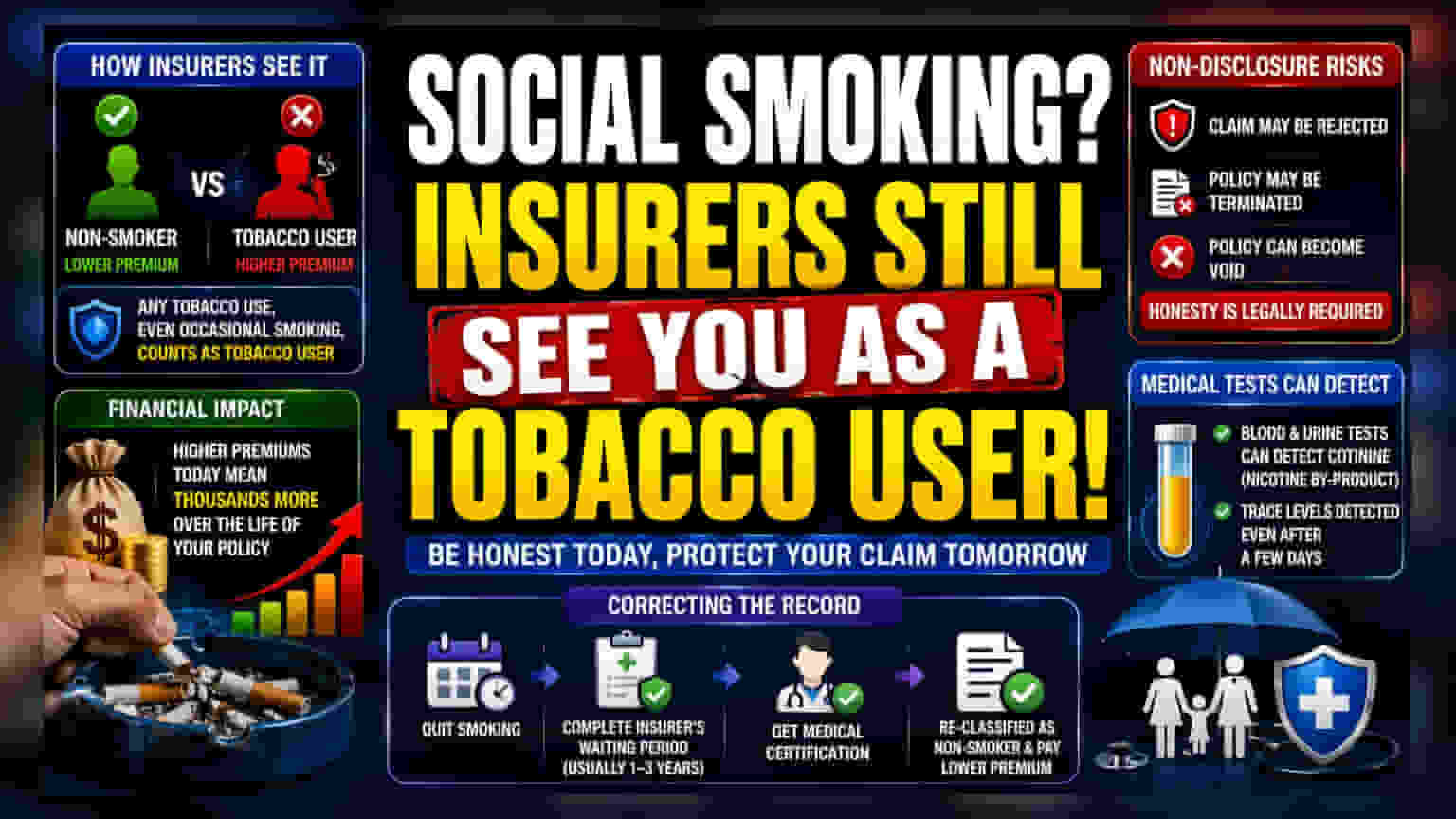

Health insurance providers classify all tobacco use as a high-risk factor, regardless of frequency. Even occasional social smoking can result in higher premiums. Crucially, failing to disclose this habit during the application process creates a significant financial risk, as insurers can legally reject claims or terminate policies if tobacco use is discovered later.

What Happened

Health insurance companies generally do not distinguish between occasional "social" smoking and habitual tobacco consumption when assessing risk. During the application process, insurers ask about tobacco use as a binary factor: you are either a user or a non-user. For underwriters, any history of tobacco use serves as a statistical indicator of potential long-term health issues such as cardiovascular disease, stroke, or cancer. Consequently, applicants who admit to social smoking are often placed in the 'tobacco user' category, which directly impacts the premium rates offered.

The Financial Impact of Classification

When an insurer classifies an individual as a tobacco user, the insurance premium is typically higher compared to a non-smoker of the same age and health profile. While the price difference for a single policy might appear manageable, the cost difference accumulates over the life of the policy. Insurers use this higher premium to account for the increased statistical probability of future medical claims. It is important for applicants to understand that underwriting rules vary by company, and each insurer has its own specific methodology for calculating these risk-adjusted prices.

Why Non-Disclosure Is a High Financial Risk

Insurance contracts are built on the 'Principle of Utmost Good Faith.' This means both the insurer and the policyholder have a legal duty to be completely honest during the application. If an individual hides their smoking habit to secure a lower premium, they risk severe financial consequences. If the insurer discovers the truth at the time of a claim—for instance, if medical tests reveal nicotine or cotinine traces—the company may exercise its right to reject the claim entirely. In more serious cases, the insurer may terminate the policy or declare it void, leaving the individual without coverage exactly when it is needed most.

Medical Tests and Verification

Many insurance policies, particularly those with higher coverage limits or for older applicants, require a medical examination. These screenings often include blood or urine analysis, which can easily detect the presence of cotinine, a chemical the body produces after processing nicotine. Even if a person has not smoked for a few days, these tests can identify recent tobacco use. Relying on the assumption that 'social' use will go undetected is a major risk that can lead to immediate complications during the underwriting process.

Correcting the Record

Individuals who have stopped smoking may be able to lower their premiums, but this usually requires proof. Insurers typically have a defined waiting period—often several years of documented abstinence—before they will re-classify an applicant as a non-smoker. This re-classification often requires medical certification. For policyholders who are currently misclassified or who have quit, the standard practice is to communicate with the insurance company to understand their specific timeline and documentation requirements for shifting to a non-smoker rate.