Waiting periods in health insurance determine when your coverage actually starts for specific medical conditions. Knowing these terms before you buy can help prevent unexpected claim rejections. Choosing policies with shorter waiting periods or buying insurance early can provide faster access to benefits when you need them most.

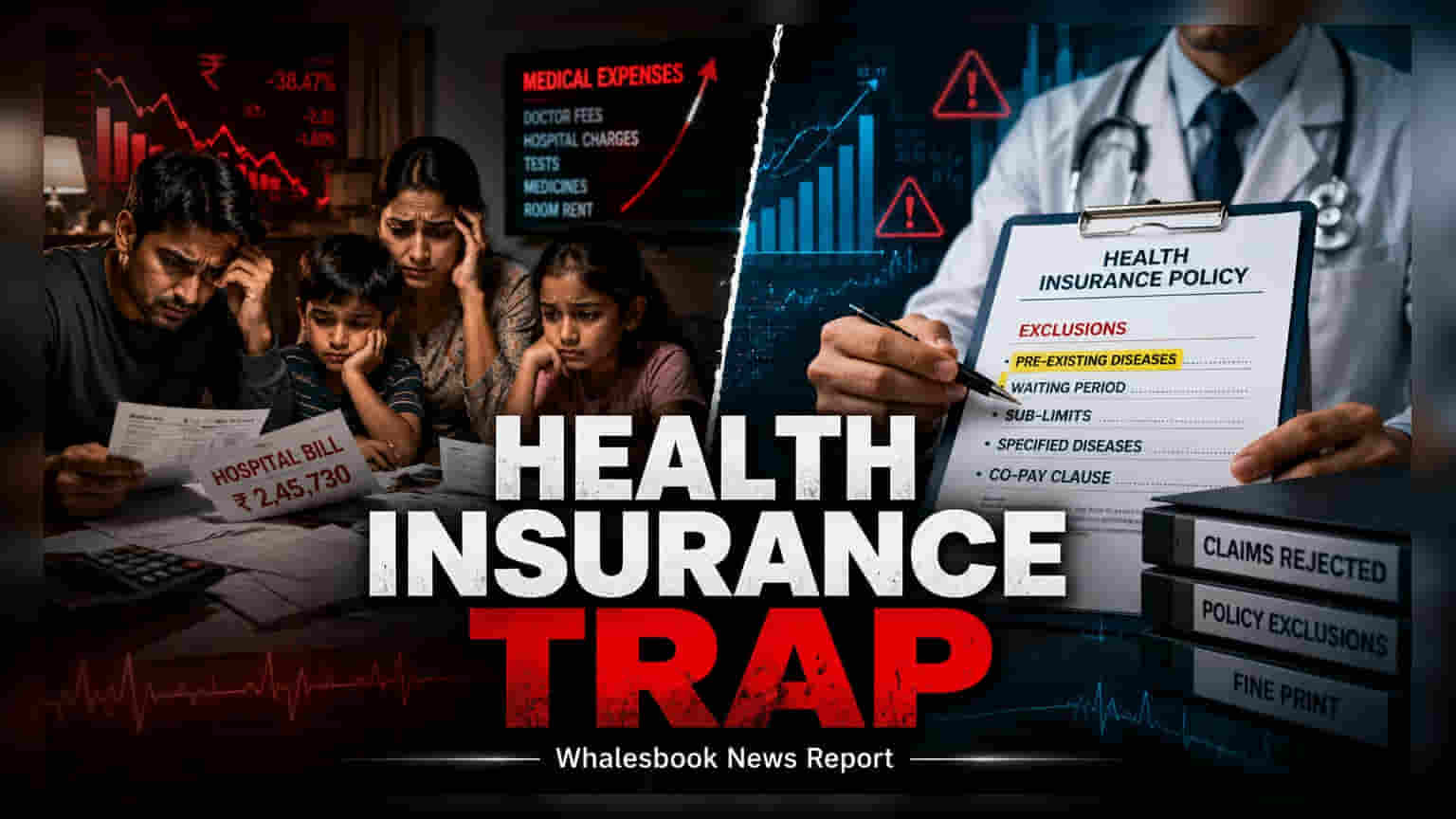

When buying health insurance, many people focus only on the premium amount and the total sum insured. However, a critical factor that can determine whether your future medical claims are approved or rejected is the waiting period. This is the specific time frame during which your insurer will not pay for treatments related to certain illnesses or existing health issues.

Understanding How Waiting Periods Function

A waiting period acts like a buffer zone after you purchase a policy. If you undergo treatment for an ailment covered by these clauses during this time, the insurance company has the right to deny your claim. For instance, most policies have an initial waiting period of 30 days for any illness, excluding accidents. More importantly, specific diseases—such as cataracts, hernia, or joint replacements—often have their own waiting periods that can last for one to two years, regardless of when you were diagnosed.

Managing Pre-Existing Conditions

For those with pre-existing medical conditions, such as diabetes or hypertension, insurers typically impose a longer waiting period before these conditions are covered. This duration is often between two to four years, depending on the insurer and the specific policy terms. Because these conditions are known to the insurer at the time of purchase, the waiting period serves as a risk-mitigation strategy for the company. Investors and policyholders should note that failing to disclose these conditions correctly at the time of purchase can lead to permanent claim rejection, regardless of the waiting period.

Strategic Planning for Policyholders

One effective way to navigate these clauses is to purchase health insurance at a younger age, even if you are currently healthy. By doing so, you allow the waiting periods for various conditions to pass while you are not yet needing medical care. By the time you reach an age where medical issues are more common, your policy will have cleared these waiting periods, ensuring that coverage is fully active.

When comparing different insurance plans, look beyond the price tag. A policy with a slightly higher premium but a significantly shorter waiting period for pre-existing conditions may offer better long-term value. Always read the policy document or the 'Key Information Sheet' provided by the insurer to understand the specific durations for different ailments. If you are switching insurers, check whether the new policy honors your 'waiting period served' from the previous plan, as some insurers offer portability benefits that can reduce your waiting time.