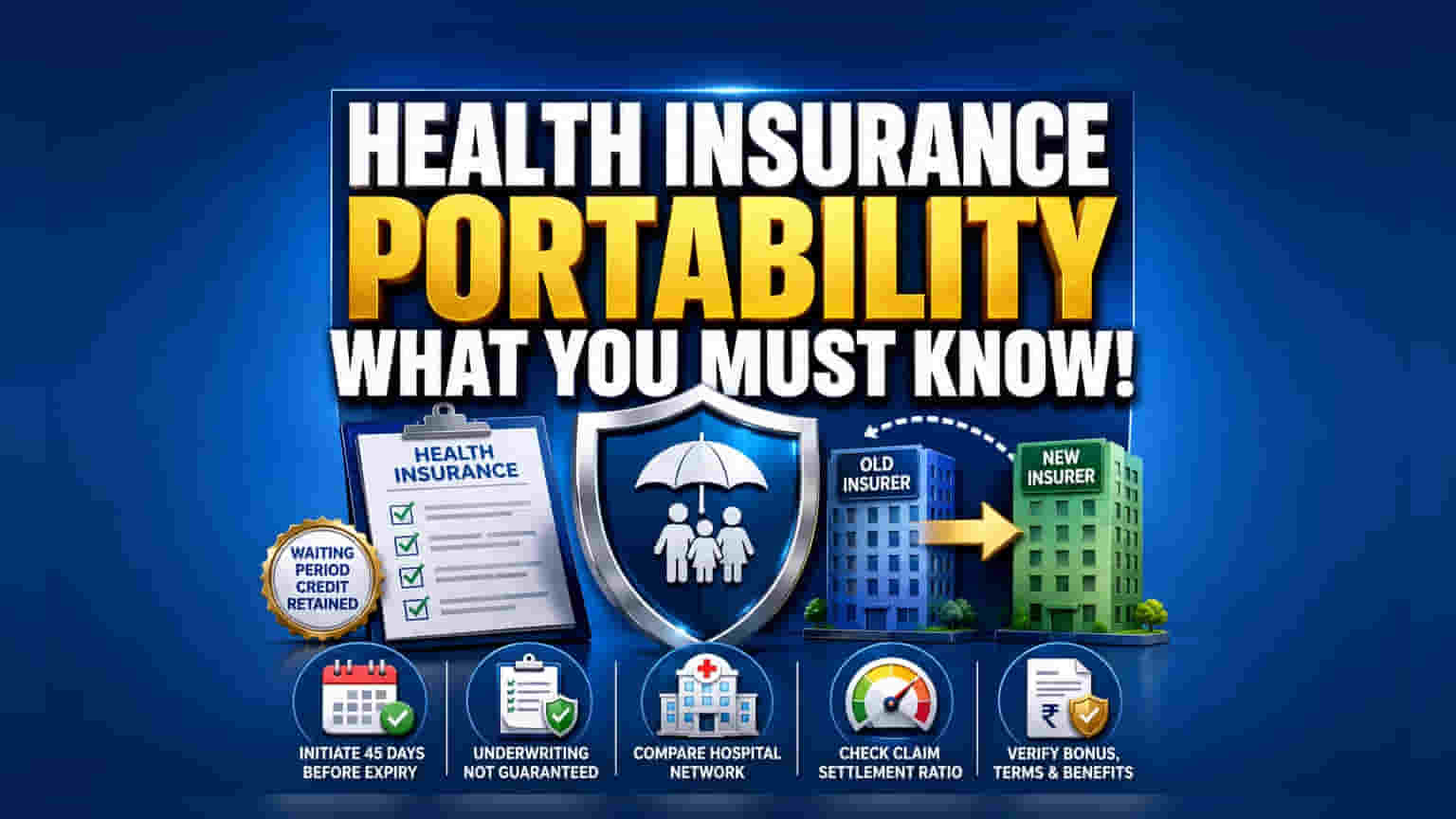

If you are unhappy with your current health insurance provider, you can switch companies while retaining credits for 'waiting periods.' This regulatory facility allows you to carry over the time spent on your existing policy to a new provider. However, this is not an automatic right; the new insurer will evaluate your health status through underwriting. If your health has declined, they may reject the request or adjust premiums. Understanding the 45-day pre-renewal timeline and checking the claim settlement ratio is essential.

What Happened

Health insurance portability allows policyholders in India to shift their existing health insurance policy from one insurer to another without losing the continuity benefits they have accumulated. Regulated by the Insurance Regulatory and Development Authority of India (IRDAI), this facility is designed to provide consumers with flexibility. The most significant benefit of porting is the retention of 'waiting period' credits. If you have already completed a specific waiting period for pre-existing diseases with your current insurer, the new insurer must count that time toward their own waiting period requirements for similar conditions.

The Underwriting Reality

While portability is a consumer right, it is not an automatic approval process. When you apply to switch, the new insurance company treats your application as a fresh proposal. This means they will conduct their own underwriting process. If your health condition has changed significantly since you bought your first policy, or if you have developed new medical issues, the new insurer has the right to evaluate your risk profile. They may accept your application as is, impose a higher premium to cover the increased risk, or in some cases, reject the porting request entirely. It is a common misconception that portability guarantees acceptance regardless of your current health status.

Why Timing Matters

Policyholders must strictly adhere to timelines to ensure a smooth transition. IRDAI guidelines require you to initiate the portability request at least 45 days before the current policy's expiry date. If you wait until the last minute, the administrative process may not be completed in time, leading to a gap in coverage. A lapse in your policy can result in the loss of all accumulated benefits, including the waiting period credits you are trying to preserve.

Comparing Beyond Premiums

Many policyholders choose to switch due to rising premiums, but focusing solely on the price can be a mistake. A cheaper policy may come with a smaller network of hospitals or restrictive terms that make claims difficult. Before switching, evaluate the new insurer’s Claim Settlement Ratio (CSR), which indicates the percentage of claims the company paid out versus the total received. A higher CSR is often considered a positive indicator of the insurer’s willingness to settle claims. Additionally, review the new plan's exclusions, room rent caps, and co-payment clauses to ensure the coverage actually meets your specific needs.

What Investors And Policyholders Should Track

When considering portability, the primary monitorables are the new insurer's underwriting decision and the impact on your total benefits. Check if the 'cumulative bonus'—the bonus you earn for not making a claim—is portable. While waiting periods are usually protected, some insurers do not transfer the full monetary value of accumulated bonuses. Verify this directly with the new company's policy document. Finally, keep all medical records organized, as the new insurer will require full disclosure of your health history. The ultimate goal should be to find a sustainable policy that balances cost, hospital network, and reliable service, rather than just chasing a lower upfront premium.