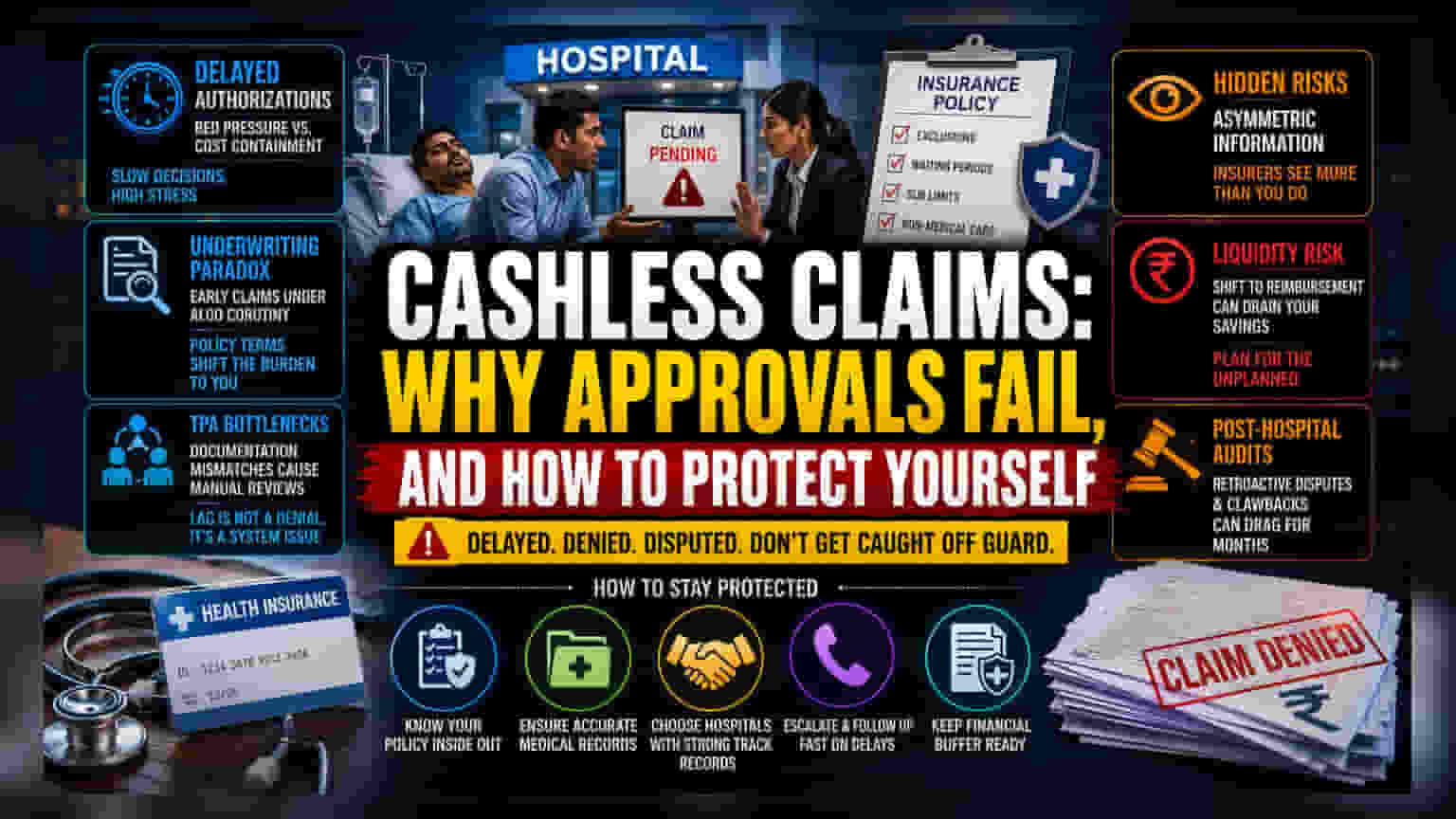

The Operational Friction of Cashless Facilities

The fundamental premise of the cashless insurance model rests on a high-velocity data exchange between healthcare providers and insurers. In practice, this mechanism frequently degrades into a procedural bottleneck. Institutional data suggests that the delay in claim authorization is rarely a result of simple policy non-compliance, but rather a byproduct of the misaligned incentives between hospitals aiming for rapid bed turnover and insurers prioritizing stringent cost-containment measures.

The Underwriting Paradox

Modern insurance contracts are increasingly dense, featuring modular exclusion clauses that shift the burden of proof onto the policyholder. While consumers often focus on the headline sum insured, the actual financial exposure is dictated by specific disease waiting periods and non-medical expense caps. Current market trends indicate that insurers are deploying advanced algorithmic scrutiny for early-term claims—those filed within twelve to twenty-four months of inception—resulting in higher rates of interim denial. This practice effectively functions as an extension of the underwriting phase, moving the risk assessment from the point of sale to the point of care.

Structural Constraints in Hospital Networks

The reliance on Third Party Administrators (TPAs) adds a layer of administrative latency to the authorization workflow. When a hospital's internal medical coding does not perfectly align with an insurer’s specific coverage guidelines, the resulting discrepancy triggers a manual review process. This administrative lag is often misconstrued by consumers as a claim denial. In reality, it reflects the systemic challenge of standardizing electronic medical records across disparate provider networks, where documentation errors remain the primary driver of initial authorization refusals.

The Forensic Bear Case: Asymmetric Information

The current insurance ecosystem suffers from significant asymmetric information. Insurers possess the actuarial data to forecast claim likelihoods with precision, yet policyholders often lack visibility into how specific diagnostic codes impact the speed of approval. For the patient, the critical risk is liquidity; the shift from cashless to reimbursement models requires immediate, unplanned capital. Furthermore, the practice of aggressive post-hospitalization audits means that even if a cashless request is initially approved, insurers may retroactively contest expenses, leading to clawback attempts that can drag on for months. As regulatory bodies continue to push for standardized claims processing, the industry faces mounting pressure to reduce the reliance on TPA intermediaries and force greater transparency in how specific treatments are classified and authorized.