Business-to-business manufacturing firm Zetwerk reports a strong revenue rise to ₹15,900 crore for FY26, backed by a ₹12,000 crore order book. As the company prepares for its IPO, investors are tracking its strategic move away from low-margin civil construction toward product-led manufacturing, balanced against risks like debt pressure and thin operating margins.

What Happened

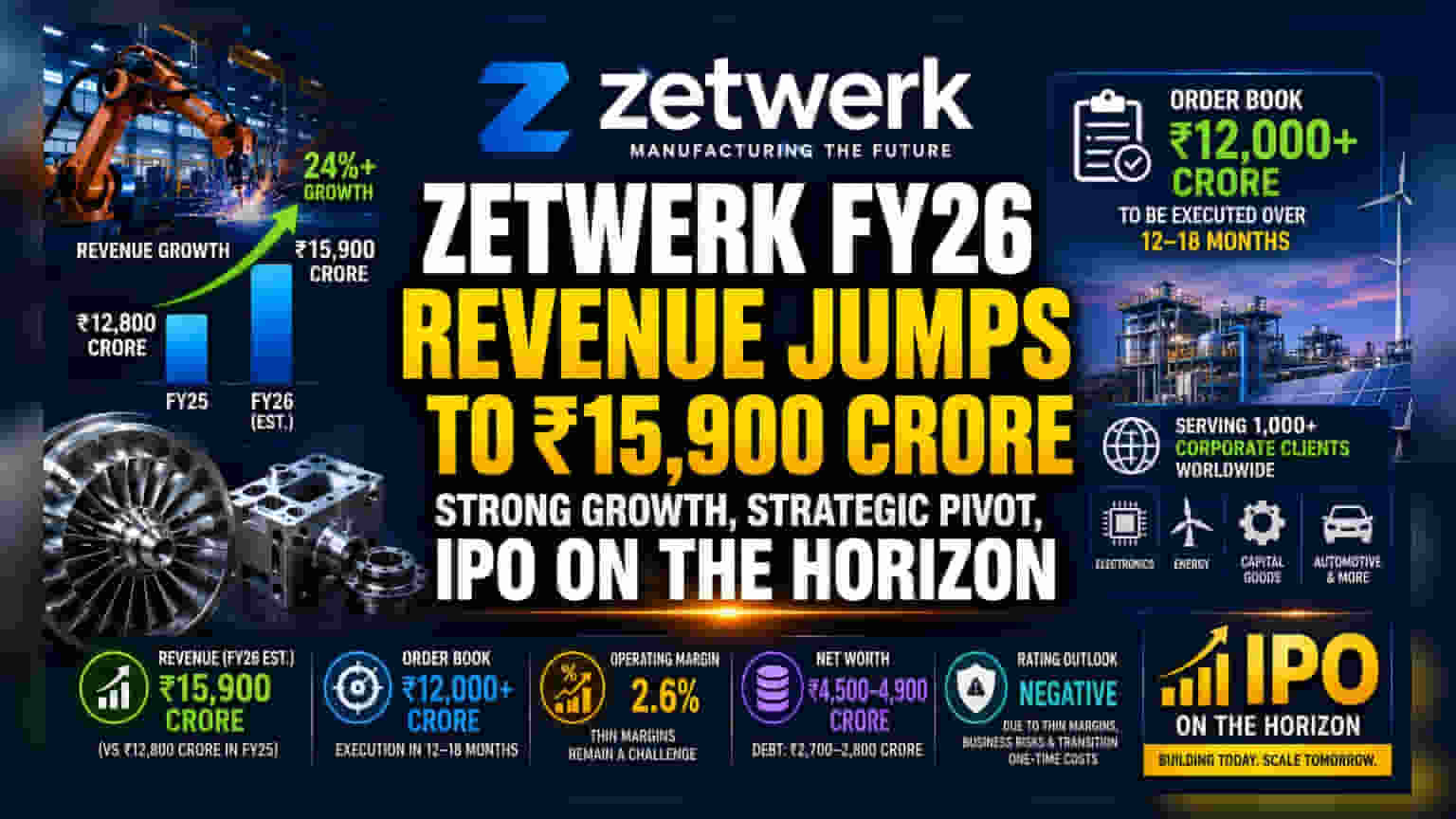

Zetwerk, the Bengaluru-based B2B manufacturing platform, has reported a strong performance for the fiscal year 2025-26. The company’s revenue for the year is estimated at ₹15,900 crore, showing significant growth from the ₹12,800 crore recorded in FY25. This expansion aligns with the company’s ongoing efforts to streamline its operations and focus on high-value manufacturing segments. Alongside this revenue growth, Zetwerk maintains a robust order book exceeding ₹12,000 crore, which is expected to be executed over the next 12 to 18 months.

Why This Matters For Investors

For investors, this growth trajectory reflects the company’s strategic transition. Zetwerk has been actively scaling down its footprint in the civil infrastructure business—an area typically characterized by lower profit margins and higher operational risks. By shifting focus toward precision manufacturing, energy, and capital goods, the company aims to improve its quality of revenue. This transition is a critical part of the company’s broader plan as it moves toward an Initial Public Offering (IPO). The ability to maintain this momentum while shifting its business model will be a key indicator of its long-term health.

The Rating Outlook And Financial Health

While the company shows strong growth, rating agencies have maintained a 'Negative' outlook on its credit ratings. This outlook is not a reflection of immediate default risk but serves as a cautionary note. Rating agencies have highlighted challenges such as thin operating margins, which remain around 2.6 percent, and the operational risks involved in a diversified business model. Furthermore, the transition away from the civil EPC business involves potential one-time costs and provisions that can impact short-term profitability. With net worth estimated between ₹4,500 crore and ₹4,900 crore and debt levels around ₹2,700-2,800 crore, maintaining a stable balance sheet while managing working capital needs remains a core focus for the management.

The Strategic Pivot

Zetwerk’s current strategy is to shift from project-based, capital-intensive work to product-led manufacturing. This move is designed to provide better revenue visibility. The company serves over 1,000 corporate clients globally, including notable names in sectors like electronics and energy. By moving toward higher-value manufacturing, the company hopes to improve its profitability, which has historically been under pressure due to the nature of its earlier business mix.

What Investors Should Track

As Zetwerk prepares for its upcoming public listing, investors may want to monitor several key areas. First, the progress in margin expansion will be vital; sustaining low margins while scaling requires strong operational efficiency. Second, the company’s ability to execute its ₹12,000 crore order book without significant cost overruns or delays is essential. Finally, management’s commentary on debt levels and the successful completion of the ongoing pre-IPO funding rounds will provide insights into the company’s financial stability. The IPO filing status and market conditions will also play a significant role in determining how the company's value is perceived by public market participants.