India’s stainless steel industry is calling for a dedicated national policy to address systemic issues, including a ₹12 lakh crore annual loss due to corrosion. This push comes as domestic manufacturers struggle with underutilized capacity and a sharp increase in imports from China following recent regulatory shifts.

What Happened

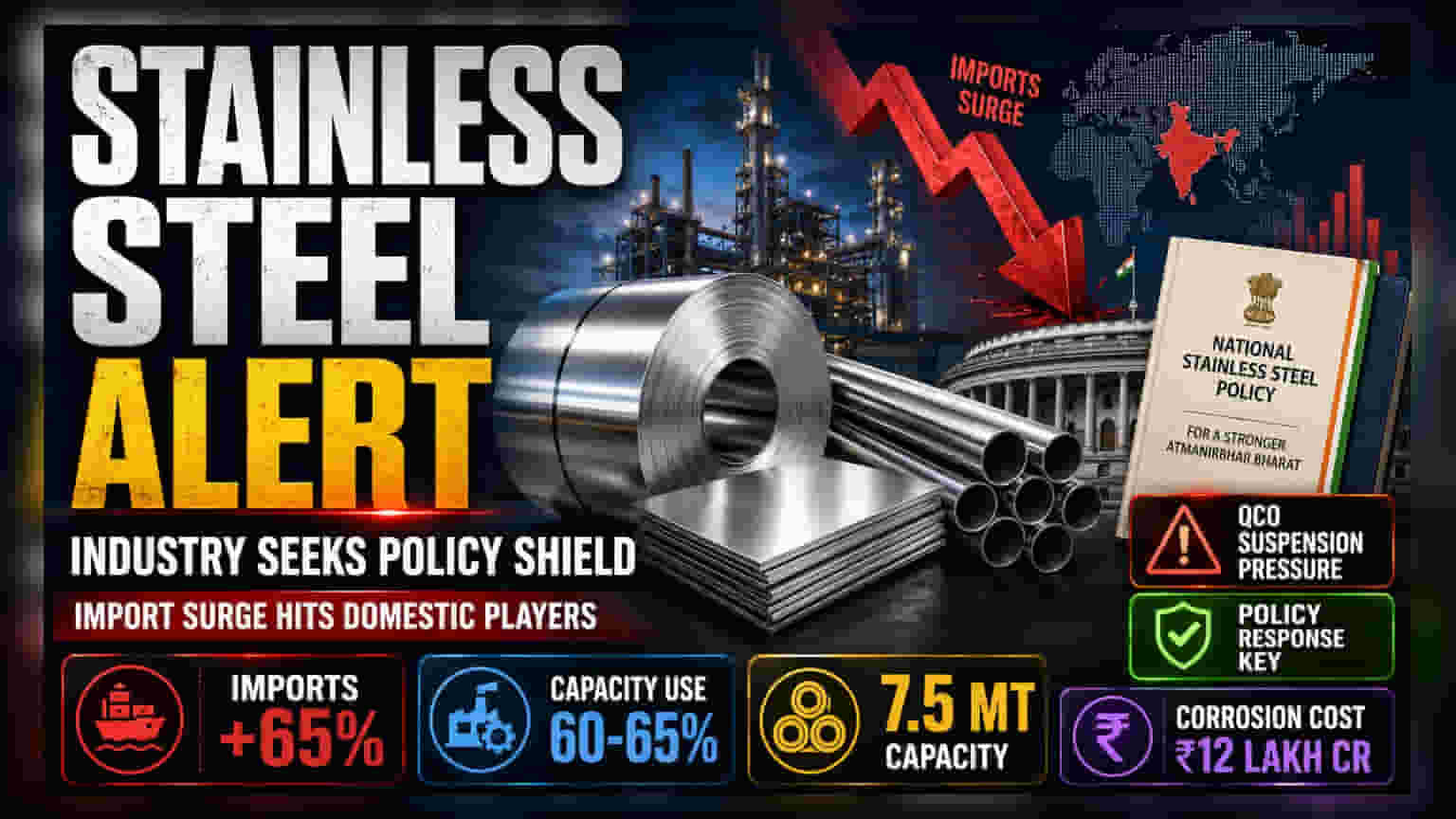

The Indian stainless steel industry, led by bodies like the Indian Stainless Steel Development Association (ISSDA), is urging the government to frame a National Stainless Steel Policy and a separate Anti-Corrosion Policy. Industry stakeholders argue that the sector requires a unique framework distinct from broader steel policies to improve capacity utilization, safeguard investments, and encourage the use of high-quality stainless steel in public infrastructure.

This demand comes amid rising stress in the sector. Recent industry data shows that stainless steel imports jumped 65% year-on-year in April 2026, following a government decision to temporarily suspend Quality Control Orders (QCO) for certain products. Manufacturers, particularly smaller units, argue that this has allowed low-priced, non-compliant material to flood the market, putting pressure on domestic players.

The Economic Toll of Corrosion

A major pillar of the industry's argument is the staggering economic cost of corrosion. Estimates suggest that India loses approximately ₹12 lakh crore every year—nearly 4% of its GDP—to corrosion-related damage across infrastructure, transport, and industrial assets. Industry leaders, including representatives from Jindal Stainless, contend that mandating stainless steel in key projects could significantly reduce this cost. They suggest that switching to durable, corrosion-resistant stainless steel for public infrastructure would lower long-term maintenance expenses, despite a potentially higher initial cost.

The Import Pressure

The stainless steel sector is currently operating at only about 60-65% of its 7.5 million tonne capacity. Domestic producers claim that they have the capability to meet local demand but are struggling to compete with imports, particularly from China, which are often priced lower. The recent suspension of QCOs—originally intended to help smaller manufacturers by easing compliance—has instead become a source of contention. Industry associations have written to the steel ministry, warning that the influx of cheap, non-BIS-compliant imports is threatening jobs and domestic manufacturing investments.

Business and Sector Context

For major players like Jindal Stainless, which has been vocal about these challenges, the situation impacts profitability and operational volume. While the government has previously implemented measures such as duties to protect the steel industry, the current situation highlights the challenge of balancing raw material access for downstream industries with the need to protect primary domestic producers from predatory pricing. The market is currently seeing a tug-of-war between downstream users who want cheaper raw materials and primary manufacturers seeking protection from import dumping.

What Investors Should Track

Investors may monitor a few key developments in the coming months:

- Government Policy Response: Any official move toward a dedicated 'National Stainless Steel Policy' or the reintroduction of stricter quality controls (QCOs) will be a critical trigger for the sector.

- Import Data Trends: Monthly import figures will indicate whether the surge is being contained or if it continues to erode the market share of domestic manufacturers.

- Capacity Utilization: A rise in domestic utilization rates would suggest that manufacturers are successfully reclaiming market share or that demand is picking up.

- Margin Performance: For listed companies in this space, watch for any impact on operating margins as they navigate the competing pressures of input costs and import pricing competition.