📉 The Financial Deep Dive

Shish Industries Limited announced its Q3 FY26 financial results, showcasing a stark divergence between its standalone and consolidated performance.

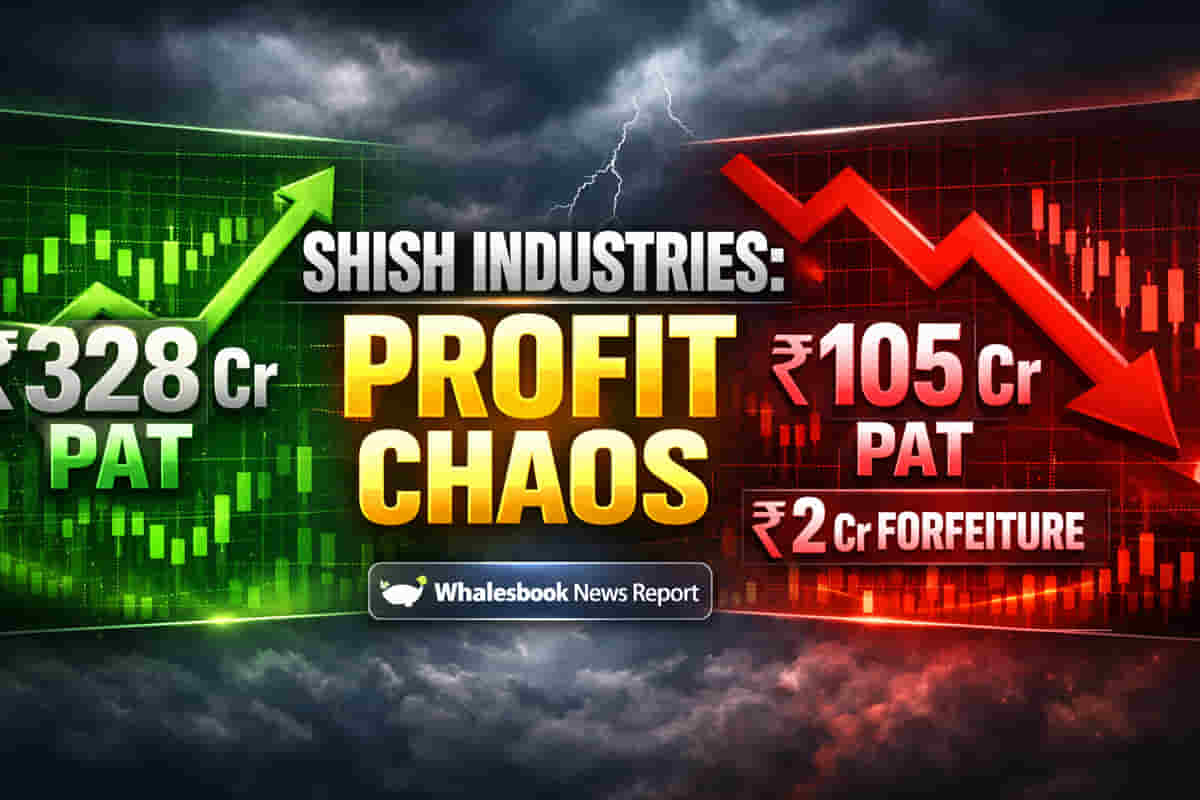

The Numbers:

Standalone Performance: The company reported a robust Revenue from Operations of ₹3,123.70 Lakhs, marking an impressive 11.7% Year-on-Year (YoY) growth from ₹2,796.47 Lakhs in Q3 FY25. This was further bolstered by a significant Profit After Tax (PAT) increase of 89.7% YoY to ₹328.37 Lakhs, up from ₹173.11 Lakhs in the prior year. Basic Earnings Per Share (EPS) climbed 80% YoY to ₹0.09. Quarter-on-Quarter (QoQ), standalone revenue saw a healthy 22.2% rise.

Consolidated Performance: In contrast, the consolidated financials revealed a troubling trend. Revenue from operations declined by 4.8% YoY to ₹3,335.58 Lakhs from ₹3,503.56 Lakhs in Q3 FY25. More alarmingly, consolidated PAT plummeted by 44.5% YoY to ₹105.48 Lakhs, a significant drop from ₹190.16 Lakhs in the corresponding quarter last year. Consequently, consolidated Basic EPS fell 40% YoY to ₹0.03.

The Quality & Concerns:

The significant drop in consolidated profitability, despite a modest QoQ revenue growth of 12.1%, suggests potential margin pressures or increased operational costs at the subsidiary level. A key concern is the cancellation of 6,72,914 warrants and the subsequent forfeiture of ₹2,02,21,065.70 (approximately ₹2.02 Cr) due to non-payment. This event, coupled with a noted statement of deviation/variation in the utilization of funds raised via Preferential Issue, raises questions about capital management and investor commitment.

The Grill:

The announcement highlighted a 'statement of deviation/variation in the utilization of funds' from a preferential issue raised on November 9, 2025. Crucially, the explanation for the deviation was marked as 'NA' (Not Applicable), with no specific comments from the Audit Committee or auditors provided. This lack of transparency on fund utilization variances and the forfeiture of warrants are critical points that warrant investor scrutiny and likely would face tough questions from analysts.

Risks & Outlook:

While the standalone performance is commendable, the declining consolidated profitability and revenue are major risks. The related party transactions (RPTs) with subsidiaries, Interstar Polyfab Private Limited and Shish Advanced Composites Private Limited, require shareholder approval beyond the materiality threshold, indicating potentially significant inter-company dealings that need careful monitoring. The lack of forward-looking guidance from management in this announcement leaves investors with uncertainty regarding future performance drivers and strategies to address the consolidated slowdown.

Investors should closely monitor the financial health and operational efficiency of the subsidiaries, the implications of the RPTs, and seek clarity on the reasons behind the consolidated performance dip and fund utilization deviations in future communications.