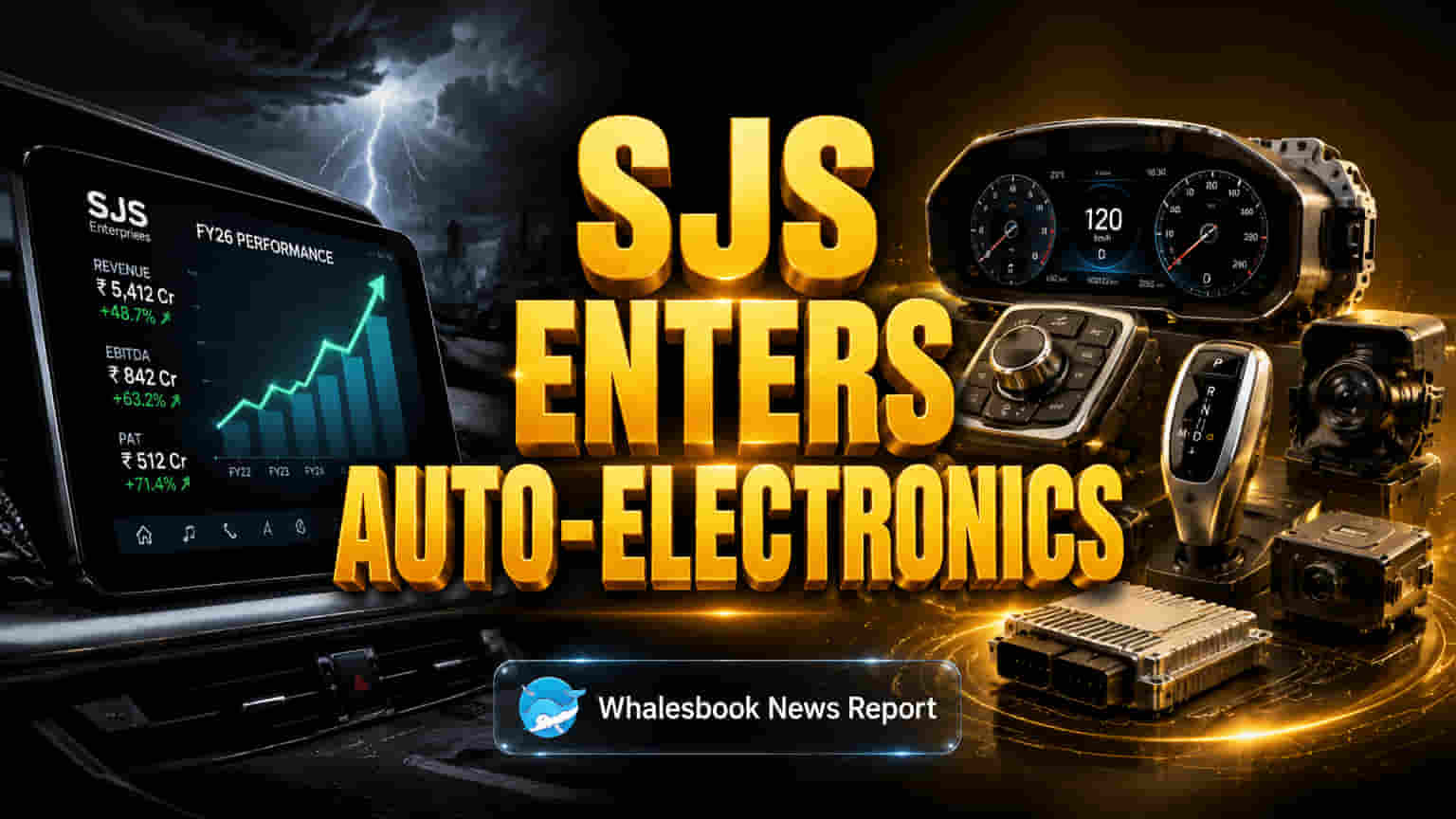

Record Quarter Fuels Expansion and Electronics Pivot

SJS Enterprises ended fiscal year FY26 with a strong fourth quarter, reporting consolidated revenue up about 30% year-on-year to ₹260 crore. This performance was driven by high demand in the two-wheeler and passenger vehicle sectors, where SJS Enterprises grew twice as fast as the industry. Earnings before interest, taxes, depreciation, and amortization (EBITDA) jumped nearly 50% year-on-year. EBITDA margins also expanded significantly, by 420 basis points to 30.3%. This improved operational efficiency led to a 45% year-on-year increase in net profit, reaching ₹49 crore.

The company is undergoing a strategic transformation, investing heavily in expanding capacity and shifting focus towards higher-value automotive electronics. Partnerships, such as with BOE Varitronix Limited for automotive displays, mark a move from decorative parts to advanced components. This strategy, along with integrating Walter Pack India, aims to boost revenue from new-generation products, which currently make up 24% of sales and increase the value of components per vehicle. Export revenue also grew strongly, up 75% year-on-year in Q4 to ₹25.5 crore (10% of total sales). Management aims for exports to reach 14-15% of sales by FY28.

Stock Price Surges, Valuation Faces Questions

Following strong quarterly results and its strategic plans, SJS Enterprises' stock price hit an all-time high of ₹2,000 on May 7, 2026. The stock is up about 107% year-on-year, far surpassing market indices. With a market capitalization of ₹6,237 crore, the current price shows high investor confidence. However, SJS Enterprises trades at a trailing twelve-month (TTM) Price-to-Earnings (P/E) ratio between 38.8x and 51x. This valuation is high compared to auto component sector peers (around 31.9x) and the industry average (about 29.5x). While an 85% order book secures much of its FY27 sales target, and analysts give it a 'Strong Buy' rating with potential for around 20% upside, its current price multiples need careful watching, especially with possible sector-wide issues.

Industry Trends and Competitive Landscape

The automotive component sector is forecast to grow 7-9% in fiscal year 2027, though the broader auto industry's growth is slowing to an estimated 3-6%. A main concern for the next fiscal year is potential pressure on profit margins due to rising commodity and energy costs, like steel and rubber. This inflation, combined with a higher base from the previous strong fiscal year, will make maintaining profitability difficult. Despite SJS Enterprises' strong financial health, shown by a net cash position of ₹240 crore and a ROCE of 35.5% for FY26, its current P/E ratio places it at a premium to many competitors. While rivals like FIEM Industries and Jamna Auto Industries operate in similar areas, SJS's move into electronics brings new competition from companies possibly more established in that technology-focused segment.

Risks and Challenges Ahead

Despite strong quarterly results and positive guidance, several risks temper the outlook. The ambitious move into automotive electronics, while promising, carries significant execution risk. This field requires different technological skills, more R&D investment, and faces competition from established electronics makers. Successfully integrating these new abilities while keeping the quality of existing aesthetic products will be key. Additionally, the company's goal to maintain EBITDA margins at 28-29% faces challenges from expected industry-wide margin pressures in FY27 due to rising commodity and supply chain costs. SJS's planned capital expenditures of ₹260 crore from FY26-28 for expansion and new facilities, though needed for growth, will strain its balance sheet and require careful management to prevent overleveraging, especially if demand forecasts aren't met. SJS's past success in decorative parts might not fully carry over to the complex automotive electronics market, where rapid technological change and high R&D are essential.

What Analysts and Management Expect

Management expects SJS Enterprises to grow 1.5-2 times faster than the industry in FY27, supported by its strong order book and increasing premiumization. The company's focus on exports and new-generation products should boost revenue and profits. Analyst consensus is largely positive, with 'Buy' ratings and price targets suggesting potential upside. However, the durability of these optimistic forecasts depends on SJS Enterprises managing upcoming margin pressures, integrating its new electronics business smoothly, and deploying capital wisely in a slowing automotive market.