Strong Q4 Performance Boosts Analyst Targets

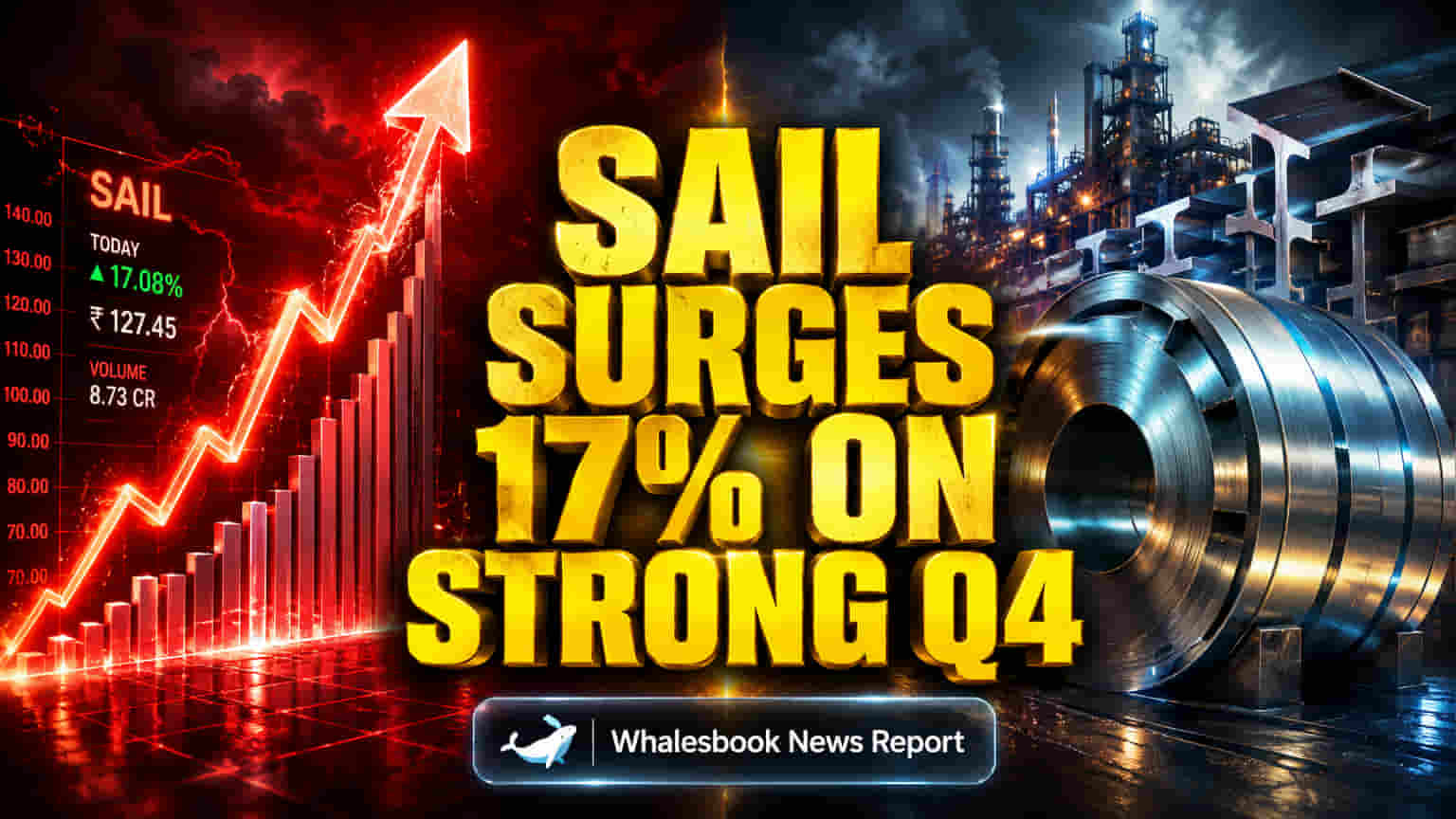

Steel Authority of India Ltd (SAIL) reported strong operational results for Q4 FY26, driven by higher steel prices and improved revenue. This performance led Motilal Oswal to reaffirm its 'Buy' rating and raise its price target to ₹225 per share, signaling a potential 17% upside. The company's profits significantly exceeded forecasts, with EBITDA reaching ₹4,490 crore and adjusted profit at ₹2,170 crore. SAIL produced 5.1 million tonnes of crude steel and sold 5.3 million tonnes, benefiting from inventory management and market efforts. The company also moved to optimize its product mix by discontinuing sales from NMDC steel.

Sector Outlook and Valuation Concerns

Despite SAIL's strong quarterly results, the wider steel market presents a mixed picture. India's domestic steel demand remains robust, fueled by infrastructure and construction projects, with plans to expand capacity significantly by 2030. Globally, however, steel demand is expected to be weak in 2026, with rising material costs and supply chain issues creating challenges.

SAIL's current price-to-earnings ratio ranges from 26.96x to 34.3x. This valuation is higher than some competitors, such as JSW Steel, which trades at 12.43x. While Motilal Oswal is optimistic, other analysts are cautious. Centrum, for instance, downgraded SAIL to a 'Sell' rating with a ₹160 target price, citing a less favorable risk-reward balance despite the strong Q4 profits.

Key Risks: Spending, Debt, and Compliance

Several significant risks temper SAIL's outlook, despite its positive Q4 results. The company plans substantial investments: around ₹150 billion for FY27, rising to ₹180-190 billion by FY28. These large spending plans could increase debt levels and slow down debt reduction efforts, even though SAIL managed to reduce debt by ₹8,148 crore in FY26.

Compliance issues also present a challenge. SAIL faces non-compliance with SEBI listing rules regarding its board makeup. Auditors have flagged concerns over certain accounting treatments and provisions, including an ₹111.43 crore disputed entry tax liability. These regulatory and accounting issues, combined with valuation worries, suggest the road ahead could be bumpy. The cyclical nature of the steel industry means high valuations can lead to greater stock price swings during market downturns.

Analyst Views and Key Challenges Ahead

Most analysts hold a positive view, with ratings generally leaning towards 'Buy'. Average 12-month price targets range from ₹156 to $21.25. India's growing steel sector, supported by infrastructure development, offers a favorable market trend. SAIL's focus on increasing its sales of value-added steel products could also boost future profits and its market standing.

However, realizing its full potential will depend on SAIL's ability to manage its high investment spending, control debt levels, resolve compliance issues, and keep pace with competitors like JSW Steel, which currently has a lower valuation.