PL Capital has maintained a 'Buy' rating on RITES Ltd with a target price of ₹275, citing strong execution prospects. The company is shifting toward a sustainable profit margin band of 18-20%, down from historical peaks. Investors are focused on the firm's ability to balance revenue growth with this changing margin profile while executing a large order book.

What Happened

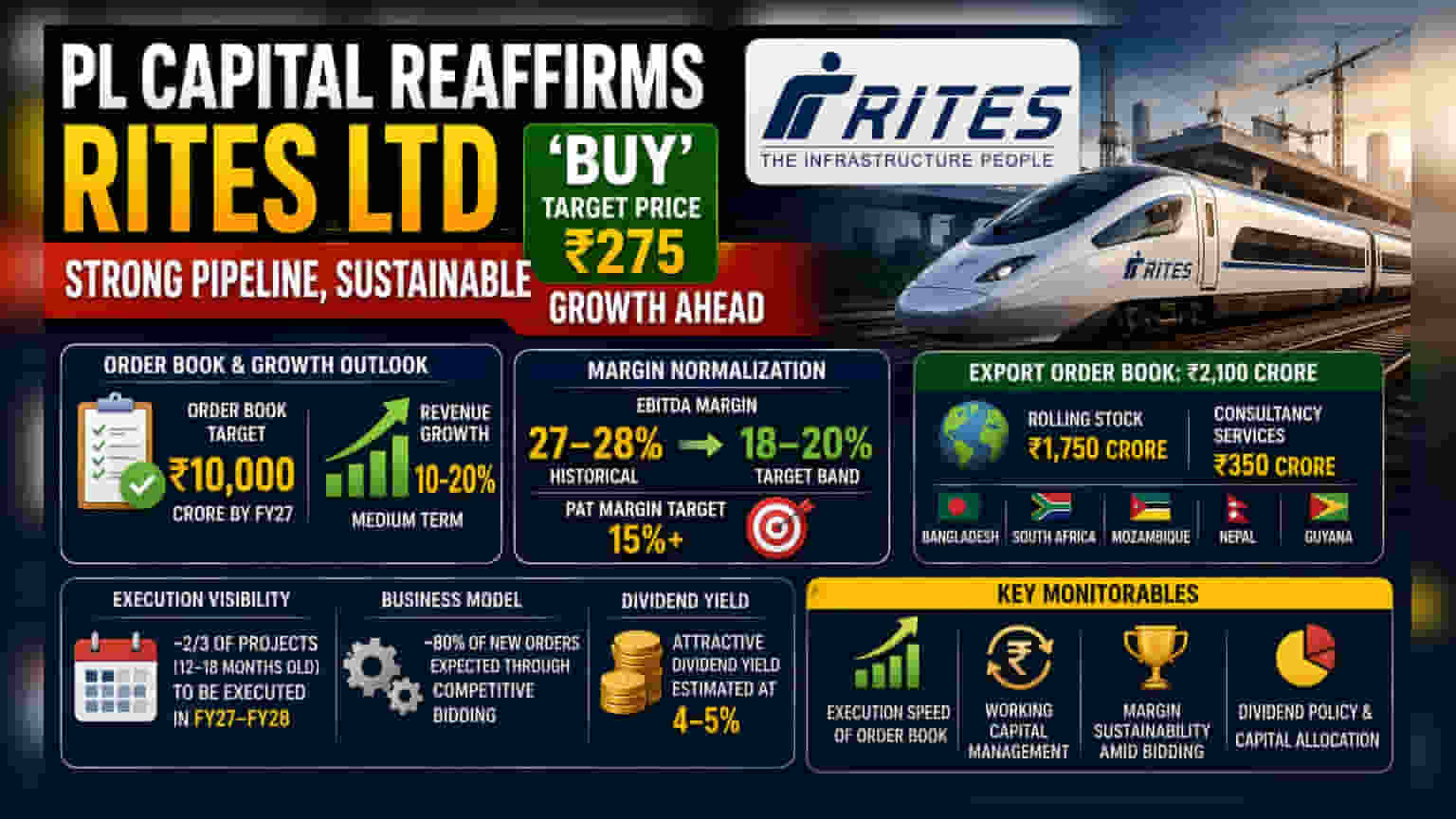

PL Capital has reaffirmed its 'Buy' rating on RITES Ltd, setting a target price of ₹275 per share. The brokerage highlighted that RITES’ growth strategy remains on track, driven by a strong pipeline of orders that are now entering the execution phase. The firm’s management has expressed confidence in its medium-term growth trajectory, supported by an order book that it aims to grow to ₹10,000 crore by the end of fiscal year 2027.

The Margin Normalization Story

For investors, the most significant update is the management's guidance on profit margins. RITES has historically operated with EBITDA margins in the range of 27-28%. However, the company is now preparing for a transition toward a more sustainable band of 18-20%.

This shift is important to understand. As the company takes on new projects through competitive bidding, the nature of the business mix changes. While revenue is expected to grow by 10-20%, the profit after tax (PAT) growth may track slightly differently as margins adjust. The company is targeting a minimum PAT margin of 15% during this period. Investors should note that while this represents a lower margin compared to historical peaks, the company aims for a more consistent and sustainable business model.

Order Execution and Export Growth

The company’s growth plan relies heavily on timely execution. Roughly two-thirds of its projects, which are between 12 and 18 months old, are scheduled to be completed between FY27 and FY28.

Additionally, the firm has secured a record export order book worth ₹2,100 crore. This includes ₹1,750 crore for rolling stock and ₹350 crore for consultancy services. These international orders are spread across various countries, including Bangladesh, South Africa, Mozambique, Nepal, and Guyana. This export visibility is a key differentiator, though it introduces exposure to international geopolitical and currency factors.

The Competitive Bidding Risk

The company expects that at least 80% of its new orders will be secured through competitive bidding processes. This is a critical monitorable for shareholders. While bidding allows for growth, it also brings the risk of margin pressure if competitors bid aggressively to capture market share. Investors may track whether the company can maintain its 18-20% margin target amid intense sector competition.

What Investors Should Monitor

Looking ahead, there are several key factors to watch. First is the actual execution speed of the existing order book versus the company’s guidance. Second, investors should observe how the company manages working capital as it scales up, given its historical asset-light business model. Finally, dividend payouts will remain a key area of interest, as RITES has traditionally maintained an attractive dividend yield, which the brokerage currently estimates between 4-5%. The company’s ability to maintain these payouts while funding growth through internal accruals will be a test of its capital allocation strategy.