Premier Explosives Q3 FY26: Revenue Moderates on Execution, Order Book Remains Strong

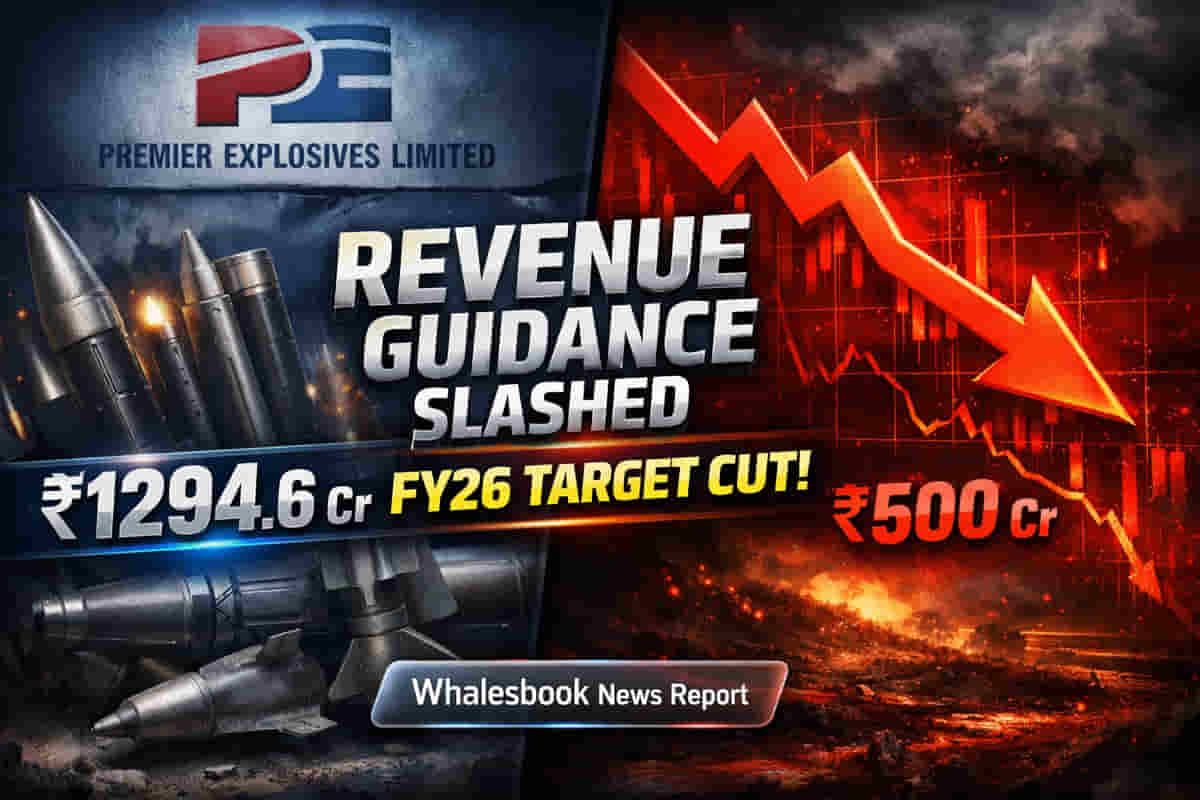

Premier Explosives' order book stands at INR 1,294.6 crore, providing 3.1x revenue visibility. The company has revised its FY26 revenue guidance to approximately ₹500 crore.

Reader Takeaway: Massive defense order book provides strong visibility; revenue recognition challenged by inspection delays.

What just happened (today’s filing)

The company reported a moderation in Q3 FY26 revenue, attributed to a high base from elevated chaff and flare dispatches in the previous year and execution timing issues.

This led to a downward revision of the FY26 revenue guidance to approximately INR 500 crore, from an earlier expectation of INR 600 crore.

However, the outstanding order book remains robust at INR 1,294.6 crore, with defense accounting for 92% of this total, providing significant revenue visibility.

A major INR 429 crore order from the Ministry of Defence (MoD) for chaffs and flares, secured in October, has been incorporated into these totals.

Why this matters

The revenue moderation highlights the challenges Premier Explosives faces in converting its strong order book into actual sales, often due to government inspection processes and execution timing.

Despite these short-term headwinds, the sustained strength in the defense order book indicates long-term demand and PEL's critical role in India's defense manufacturing ecosystem.

The revision in guidance and the upcoming contribution from the Katepally expansion facility will be key factors for investor assessment.

The backstory (grounded)

Premier Explosives is a leading Indian manufacturer of explosives, propellants, and detonators, catering to both defense and civil sectors.

The company holds a significant position in supplying propellants for prestigious Indian missile programs and is the sole domestic manufacturer of certain defense countermeasures.

In April 2025, a serious accident at the company's rocket motors facility in Katepalli caused a business loss of INR 20-30 crores and resulted in casualties.

Recently, SEBI initiated an inquiry into suspected insider trading activities involving the company's shares, with Premier Explosives cooperating with the regulator.

What changes now

Shareholders can expect a revised revenue trajectory for FY26, with management focusing on managing execution and inspection-related delays.

The planned capex of INR 60 crore for FY27, directed towards the Katepally and PDK plants, aims to bolster future production capabilities.

The Katepally expansion for RDX/HMX is slated to start production in Q1 FY27, expected to contribute INR 150-200 crore in revenue for that fiscal year.

Risks to watch

Execution timing and delays caused by MoD pre-dispatch inspections remain a recurring challenge, impacting revenue recognition.

Geopolitical conditions have led to delays in importing critical inputs, affecting the supply chain.

The management described the feasibility of hitting the upper end of guidance as "shaky" due to inspection unpredictability.

Sequential margin declines were linked to Liquidated Damages (LDs) on certain MoD orders.

Peer comparison

Premier Explosives competes with players like Solar Industries India Ltd. and GOCL Corporation Ltd. in the explosives and defense materials market.

Solar Industries is recognized for its broad defense product range, while GOCL operates in industrial explosives and has defense exposure.

Context metrics (time-bound)

- The outstanding order book stood at INR 1,294.6 crore as of Q3 FY26 (Consolidated).

- FY26 revenue guidance has been revised to approximately INR 500 crore (Consolidated).

- The Katepally expansion is expected to contribute INR 150-200 crore in revenue for FY27 (Consolidated).

- Planned capex for FY27 is INR 60 crore (Consolidated).

What to track next

Monitor the conversion of the order book to revenue, with a close watch on MoD inspection timelines.

Track the commencement of production at the Katepally RDX/HMX facility in Q1 FY27 and its revenue contribution.

Observe the company's ability to achieve its revised FY26 revenue guidance and the FY27 outlook of INR 500-600 crore.

Keep an eye on any further developments regarding the SEBI inquiry into suspected insider trading.

Evaluate the impact of geopolitical factors on raw material imports and supply chain stability.