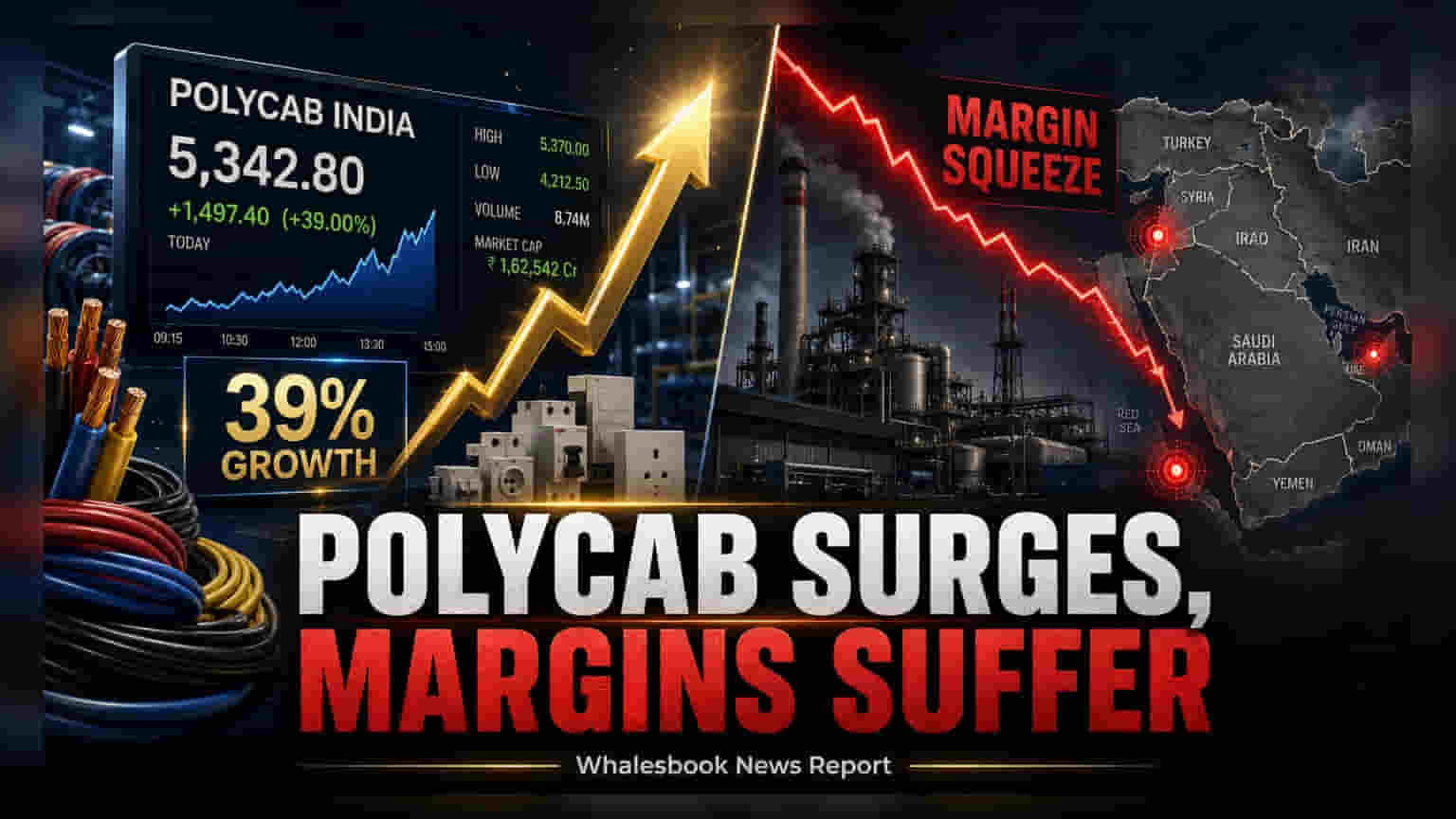

Polycab India reported a 39% revenue increase for Q1 FY27, led by strong performance in its Wires and Cables and FMEG divisions. However, profit margins faced pressure due to higher raw material costs and supply chain issues in the Middle East. Investors are now monitoring how the company manages international trade disruptions and shifting commodity prices.

Polycab India Limited began the 2026-27 financial year with a sharp 39% year-on-year rise in revenue. The company’s primary segment, Wires and Cables, which contributes 87% of its total revenue, saw growth supported by higher copper prices, although volume growth remained moderate. Meanwhile, the Fast Moving Electrical Goods division grew by 71%, with solar products showing significant demand.

Impact of Margin Pressure and Supply Chain Issues

Despite the revenue gains, the company's operating profit margin, or EBITDA margin, contracted by 70 basis points. This decline was largely driven by rising raw material costs and ongoing logistical problems in the Middle East, a key export market for Polycab. As a result, the company’s international business revenue fell 13% compared to the previous year. To adjust to these changes in commodity prices, Polycab implemented a 3-4% price reduction for its Wires and Cables products in July 2026.

Segment Performance and Strategic Outlook

The FMEG segment showed improvement in profitability, with EBIT margins rising by 590 basis points. This growth was aided by a higher proportion of premium products, which now make up 25% of the segment's revenue. In contrast, the Engineering, Procurement, and Construction business saw an 11% decline in revenue, which the company attributed to the timing of project completions rather than a lack of demand. The management team expressed confidence in the company's order book and expects execution to pick up in the coming quarters.

Capital Allocation and Market Context

Polycab continues its Project SPRING initiative, which focuses on expanding its Wires and Cables market share while targeting domestic operating margins between 11% and 13%. The company has set a capital spending budget of ₹1,200 to ₹1,600 crore for the full fiscal year. While the business benefits from long-term demand related to power transmission, renewable energy, and data centers, the stock is currently trading at approximately 36 times its estimated FY28 earnings. Moving forward, investors may track how the company manages potential industry overcapacity and whether it can navigate international supply chain problems to restore margin stability.