Revenue Growth vs. Profit Pressure

Larsen & Toubro (L&T) anticipates strong double-digit revenue growth for the January-March 2026 quarter, driven by its large order backlog and solid project execution. However, profitability is expected to lag, showing that revenue growth alone isn't enough to boost profits without tackling margin challenges and operational changes. This contrast is drawing investor attention to the company's strategic shift.

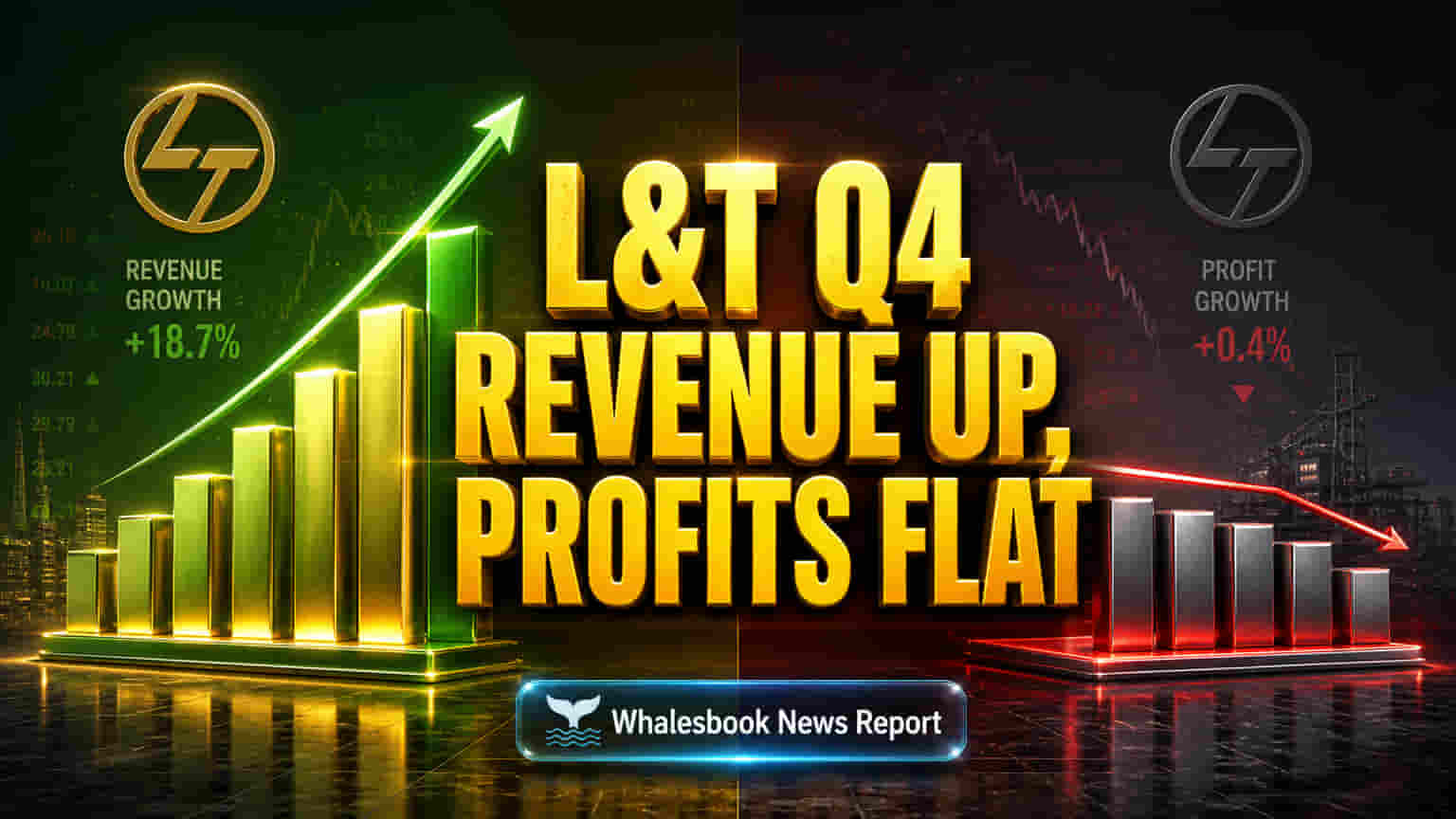

Q4 Revenue Expected to Rise Sharply, Profits Lag

With Q4 FY26 results due May 5, 2026, L&T is expected to report strong revenue. Brokerage estimates suggest revenues could hit ₹83,830 crore, up 12.7% year-on-year. This is mainly due to strength in its Core Engineering & Construction (E&C) segment, supported by domestic and international projects, particularly in the Middle East. However, profit growth is expected to be slow. Net profit is forecast around ₹5,501.73 crore, barely up from last year. This profit stagnation, despite higher revenue, indicates ongoing margin squeeze and rising operational costs are impacting earnings. L&T's stock, trading around ₹4,014, shows investors are watching its ability to turn revenue into profits.

Diversification Strategy and High Valuation

L&T is pursuing a future beyond traditional infrastructure by selling non-core assets, like the Hyderabad Metro stake, to invest in emerging sectors like green energy, semiconductors, and data centers. This shift is happening as India's capital goods sector shows strong growth, partly due to government spending plans of ₹12.2 lakh crore for FY 2026-27 on infrastructure such as railways and energy. While L&T's broad business model is distinct, its P/E ratio of around 34.67x to 37.0x is high compared to the Indian Construction industry average of 16.5x. This suggests the market expects significant future growth. The company must deliver on both revenue and profit, especially as its IT units face challenges from AI developments. Analysts generally rate L&T a 'Buy' with price targets near ₹4,485, expecting upside if execution and margin management are strong.

Risks: Middle East Exposure and Margin Compression

Significant risks remain despite the positive outlook. L&T's large order book (about 37%) from the Middle East creates exposure to geopolitical risks and operational problems. The Core E&C segment's EBITDA margins are expected to drop by 30 basis points to 9.6%, showing challenges in maintaining profitability amid project disruptions and rising costs. Although L&T has a market capitalization of ₹5.52 trillion, its high P/E ratio compared to peers and its own history could mean it's overvalued if earnings growth slows. L&T's traditional business lines face competition and economic cycles, unlike some competitors in higher-margin digital services. Issues with project execution, like those in the Middle East, can hurt margins. Investors should also track asset sales, as delays or lower returns could limit future investment. L&T Technologies Services Ltd.'s net profit also fell in Q3 FY26 due to labor code changes, illustrating the complex operational issues across L&T's various businesses.

Navigating Growth and Challenges Ahead

For L&T, successfully managing margin pressures while seizing growth opportunities in new sectors will be key. Analysts' average 12-month price target is around ₹4,485, suggesting an 11.54% potential upside, though sentiment is mixed. Firms like Motilal Oswal and PL Capital maintain 'Buy' ratings, focusing on Middle East order execution and the success of L&T's asset sales and new ventures. L&T aims for ambitious growth, projecting revenue and adjusted PAT (profit after tax) to grow at 14% and 22% compound annual rates respectively from FY25 to FY28. This plan relies on shifting towards higher-margin, technology-focused businesses. The market will closely observe L&T's execution of this significant strategy change.