Global brokerage Jefferies expects India's power transmission and distribution demand to double, driven by data centers and renewable infrastructure. The firm has issued 'Buy' ratings for Hitachi Energy India and Siemens Energy India, while initiating 'Hold' coverage on GE Vernova T&D India.

What Happened

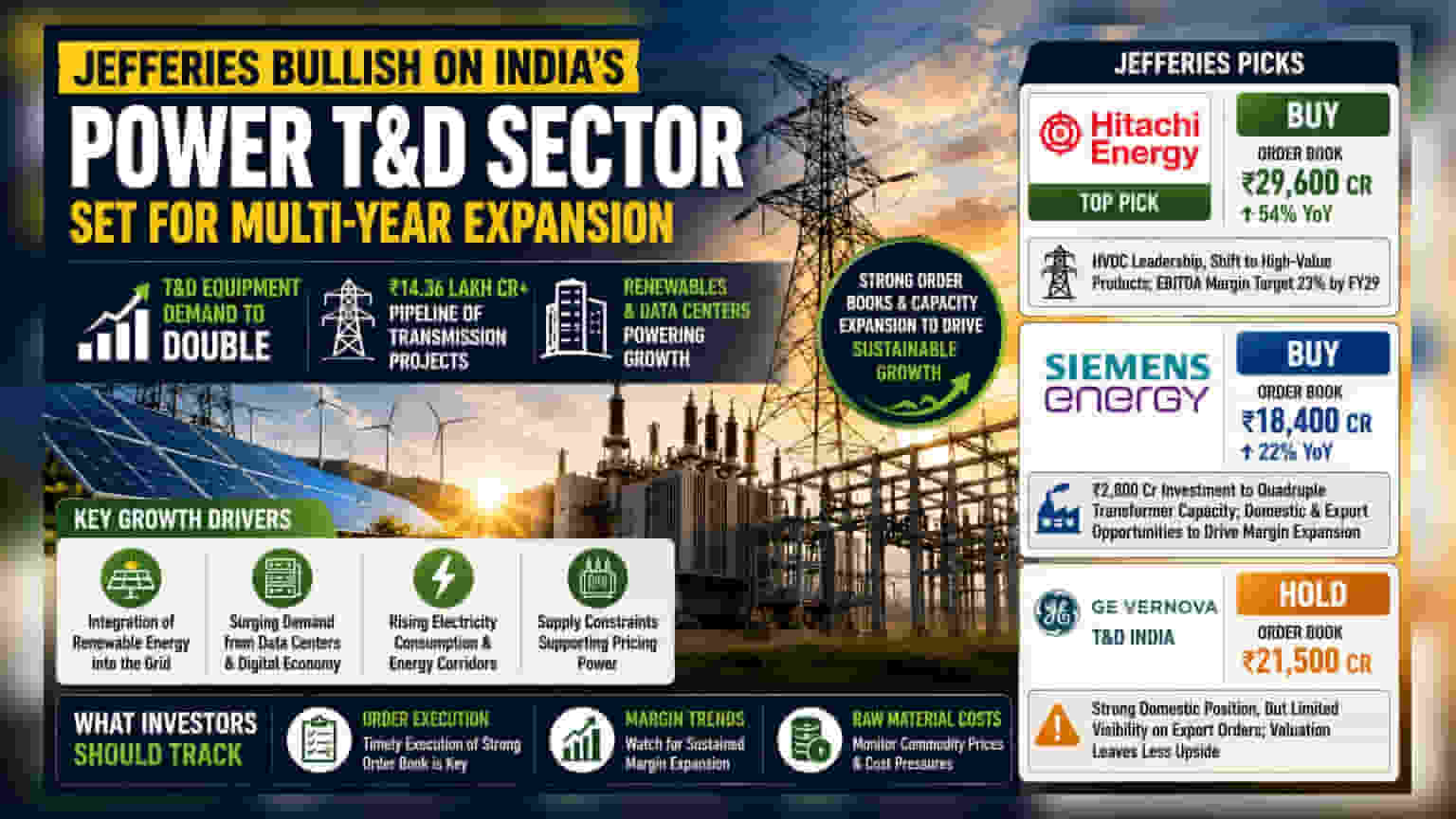

Global brokerage Jefferies has released a positive outlook for India's power transmission and distribution (T&D) sector. The firm expects a major multi-year expansion, driven by the need for more infrastructure to support renewable energy and the rising number of data centers. Jefferies projects that demand for T&D equipment could double in the coming years. Based on this, the brokerage has issued 'Buy' ratings for Hitachi Energy India Ltd. and Siemens Energy India Ltd., while initiating coverage on GE Vernova T&D India with a 'Hold' recommendation.

The Growth Drivers

This growth cycle is supported by a large pipeline of national transmission projects, estimated at over ₹14.36 lakh crore. These projects include the integration of renewable energy sources into the national grid and the development of major energy corridors. As demand for electricity rises, the need for new substations, transformers, and high-voltage transmission lines has grown. The brokerage notes that the supply of critical electrical equipment has not kept pace with this demand, which may help manufacturers maintain healthy pricing power.

Hitachi Energy India: Margin Focus

Jefferies identified Hitachi Energy India as a top pick in the sector. The company's order book stood at ₹29,600 crore as of March 2026, showing a 54% increase compared to the previous year. A major factor behind this growth is the company's focus on High Voltage Direct Current (HVDC) projects, where it maintains a significant share of the market. The business is also moving away from simple construction-heavy (EPC) work toward more specialized product design and engineering. This shift is expected to help the company improve its profit margins, with the brokerage projecting EBITDA margins to reach 23% by FY29.

Siemens Energy India: Capacity Expansion

Siemens Energy India also received a 'Buy' rating. The company is actively expanding its production capacity, including an investment of ₹2,800 crore to quadruple its power transformer manufacturing. This expansion is designed to capture both domestic demand and export opportunities, including needs from global data center operators. As the company increases its factory utilization, fixed costs are expected to spread over more units, which could boost profit margins. Its order book was reported at ₹18,400 crore, reflecting a 22% year-on-year increase.

GE Vernova T&D India: A Cautious Approach

Jefferies initiated coverage on GE Vernova T&D India with a 'Hold' rating. While the company is well-positioned to benefit from the domestic transmission cycle, with an order book of ₹21,500 crore, the brokerage expressed caution regarding its export business. Historically, the company relied on orders linked to its parent firm to boost margins, but visibility on these export orders has declined. Consequently, the brokerage noted that current stock valuations leave less room for further growth compared to peers.

What Investors Should Track

Investors looking at this sector should track three main areas: order execution, margin trends, and raw material costs. While order books are strong, the ability of these companies to turn those orders into revenue without delays is critical. Furthermore, margin expansion remains a key performance indicator; investors may watch for updates on whether these companies can successfully improve efficiency as planned. Finally, any change in raw material prices or export demand could influence future financial performance.