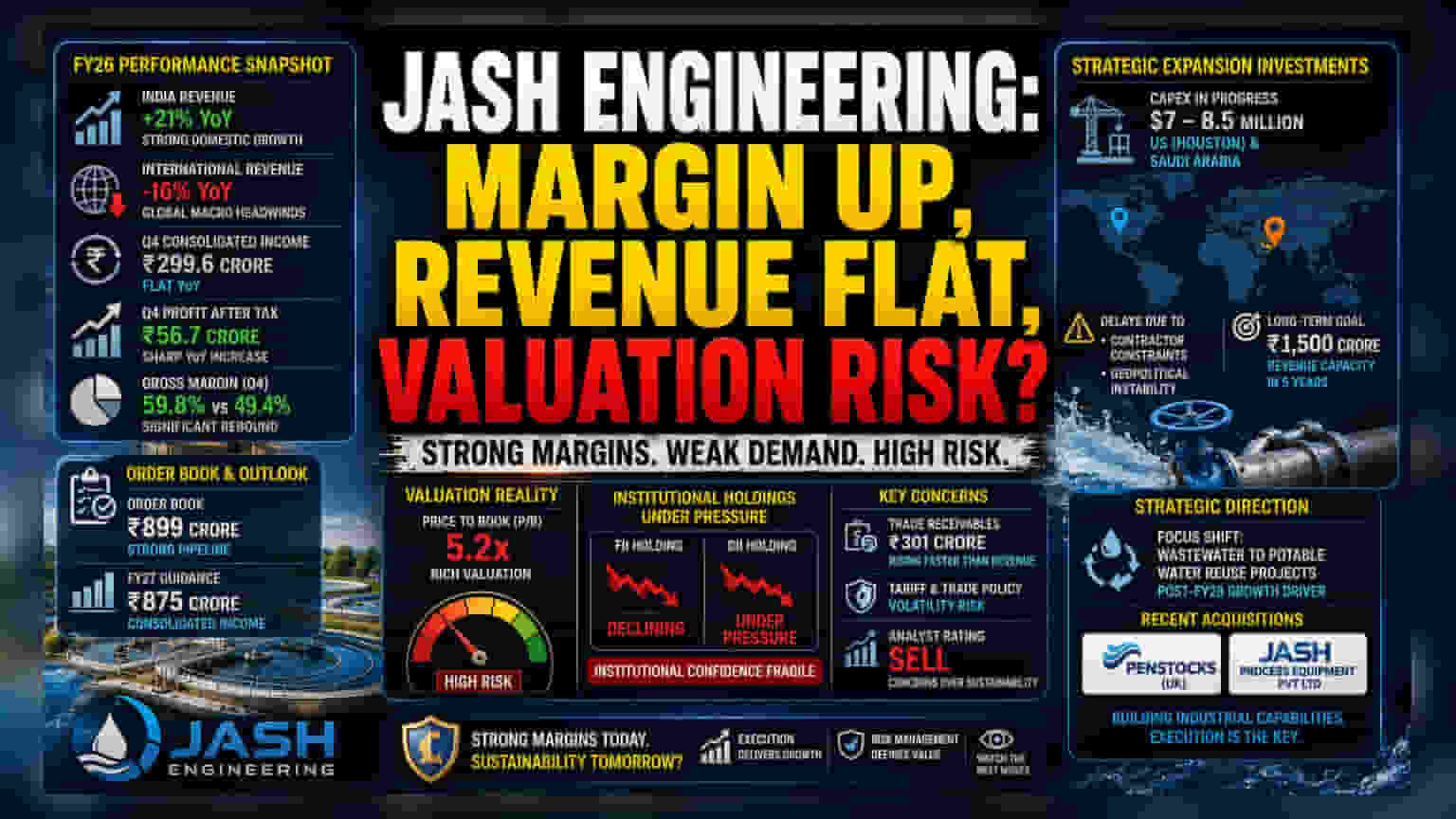

The Margin-Revenue Divergence

Jash Engineering’s fiscal 2026 performance presents a complex narrative of operational resilience clashing with global macroeconomic friction. While domestic growth in India’s water and wastewater infrastructure remains a robust tailwind—contributing to a 21% YoY revenue increase in the India segment—this was nearly neutralized by a 16% revenue contraction in international markets. The contrast in the March quarter was particularly striking; consolidated income of approximately ₹299.6 crore remained flat against the previous year, yet profit after tax surged significantly, reaching ₹56.7 crore. This bottom-line expansion was primarily driven by a sharp rebound in gross margins to 59.8%, contrasting with the 49.4% recorded in the same period last year, rather than top-line acceleration.

Strategic Pivot and Operational Risks

The company is aggressively pivoting toward a long-term water infrastructure play, betting that wastewater-to-potable-water reuse projects will supersede current road and rail capital expenditure cycles post-FY28. However, the execution path remains fraught with friction. Significant capital expenditures in the US (Houston) and Saudi Arabia, now estimated at a combined cost of $7–8.5 million, have faced delays due to contractor availability and geopolitical instability. These projects are critical to the firm's goal of reaching a ₹1,500 crore revenue capacity within five years, but they simultaneously increase the company's risk exposure to fluctuating global trade policies and tariff-related cost pressures.

The Forensic Bear Case

Despite the management’s optimistic growth narrative, a more cynical view emerges from the current valuation and institutional data. Trading at a price-to-book (P/B) ratio of approximately 5.2x, the stock carries a premium valuation that market participants increasingly struggle to justify against cooling profit margins. Institutional confidence appears fragile, with Foreign Institutional Investor (FII) and Domestic Institutional Investor (DII) holdings showing signs of pressure. Furthermore, the company’s recent 'Sell' rating by specific market analysts highlights concerns over whether the current fundamental performance can sustain the historical price appreciation. With trade receivables rising to ₹301 crore—growing faster than annual revenue—the company’s cash conversion cycle remains a critical area of concern for risk-averse investors.

Future Trajectory

Management has issued guidance for consolidated income of ₹875 crore for FY27, signaling an expectation that the order book of ₹899 crore will convert into tangible top-line growth. The integration of recently acquired entities like Penstocks (UK) and Jash Process Equipment Pvt Ltd represents the next phase of the firm's industrialization strategy. However, until these global subsidiaries demonstrate consistent profitability and the company reduces its sensitivity to tariff-related volatility, the stock will likely remain highly reactive to quarterly execution markers.