The Efficiency Trap

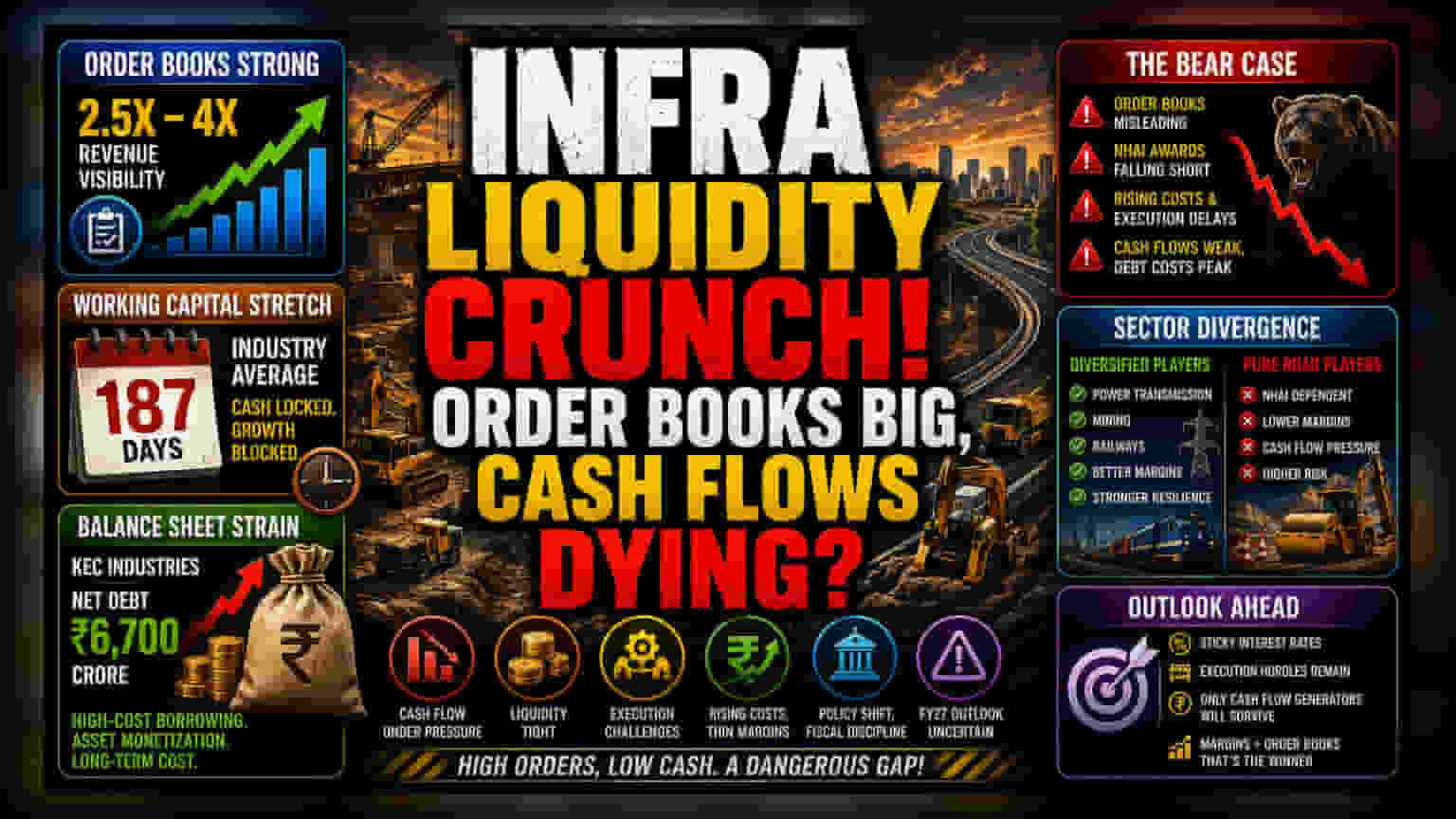

The core issue currently plaguing the infrastructure sector is not a lack of work, but an inability to convert that work into cash efficiently. While order books for many road majors remain robust—often cited at 2.5 to 4 times revenue—these metrics mask a deterioration in operational quality. The conversion of these orders into revenue is being throttled by both regional instability affecting logistics and a fundamental inability to manage input costs.

The Capital Intensity Problem

Corporate balance sheets are feeling the strain of prolonged working capital cycles. The industry average has stretched to 187 days, effectively starving companies of the liquidity needed to bid on newer, more profitable projects. This liquidity crunch is forcing firms toward high-cost debt to sustain ongoing operations. For instance, the expansion of net debt at KEC Industries to ₹6,700 crore highlights how reliance on short-term funding for long-term projects creates a precarious financial structure. This shift necessitates aggressive asset monetization, which, while providing temporary relief, limits long-term growth potential by stripping away revenue-generating infrastructure assets.

The Forensic Bear Case

The current reliance on order book-to-sales ratios is becoming a misleading metric for investors. When a significant portion of an order book—such as the mining contracts inflating KNR Constructions' figures—is pushed into future fiscal years or represents non-core business, the immediate outlook for core road construction remains grim. Furthermore, the persistent underperformance regarding NHAI award targets suggests that the government is either tightening fiscal discipline or prioritizing alternative sectors, leaving road-focused firms vulnerable. Investors should be wary of firms claiming high ratios without corresponding improvements in cash flow from operations, as these companies are essentially trading future stability for present-day survival.

Sector Divergence and Outlook

Market participants are beginning to distinguish between operators with diversified portfolios and pure-play road developers. Firms that have successfully migrated into power transmission, mining, and railway sectors are demonstrating greater margin resilience compared to those anchored solely in the National Highways Authority of India project ecosystem. As interest rates remain sticky and execution hurdles persist, the anticipated surge in FY27 revenue is unlikely to be uniform. Only companies that can demonstrate sustained margin expansion—rather than just nominal order book growth—are likely to survive the current liquidity squeeze without resorting to equity dilution.