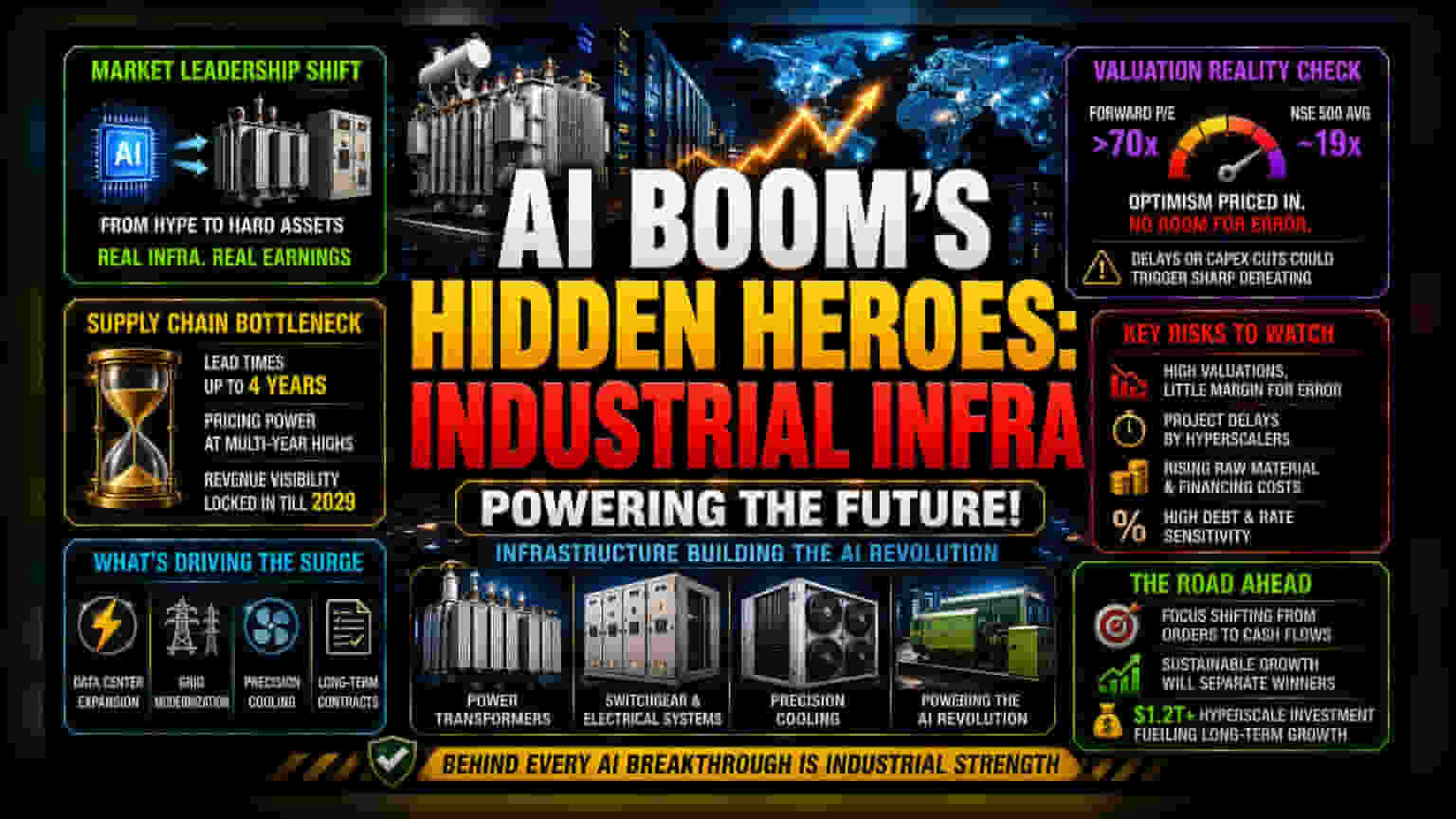

The Shift in Market Leadership

The narrative that Indian markets were bypassed by the artificial intelligence boom overlooks a critical, high-margin reality currently playing out in the industrial sector. While domestic benchmarks struggle with broader selling pressure, a specialized subset of manufacturers providing the physical backbone for AI—transformers, switchgear, and precision cooling—has realized substantial market cap expansion. This performance divergence highlights a pivot from speculative thematic growth to verifiable infrastructure-linked earnings. The current valuation expansion among these providers is largely supported by non-discretionary capital expenditure cycles, as global technology giants scale regional infrastructure to meet localized compute demands.

The Infrastructure Bottleneck

The supply chain for digital expansion is currently operating in a state of chronic scarcity. Lead times for critical power components now extend to four years in certain categories, granting suppliers significant pricing power. This structural backlog effectively anchors revenue visibility into 2029, a stark contrast to the volatility typically found in broader equity sectors. By focusing on the tangible inputs of the AI transition—rather than software-as-a-service or algorithmic development—investors are backing entities with high barriers to entry and long-duration contracts, effectively creating a hedge against shifting technological trends.

The Forensic Bear Case: Valuation Risks

Despite the underlying strength in order books, the current market pricing reflects a high degree of optimism that leaves little margin for execution errors. Several firms within this sector are now commanding forward price-to-earnings multiples exceeding 70x, a massive premium compared to the broader NSE 500 average of approximately 19x. This valuation gap suggests that the market has priced in several years of perfect execution and flawless margin expansion. Any delay in project commissioning by hyperscalers or a contraction in capital expenditure budgets could trigger significant mean reversion. Furthermore, companies with high historical debt levels or those transitioning from legacy industries remain vulnerable if interest rates remain elevated, as the cost of financing the physical build-out of these facilities remains a non-trivial factor in net profitability.

Forward Trajectory

Looking toward the remainder of 2026, the durability of this trade will likely depend on the transition from contract wins to cash flow realization. The focus is shifting from simple order book growth to the ability of management teams to scale operations without succumbing to margin compression caused by rising raw material costs. While the scale of global hyperscale investment—projected to exceed $1.2 trillion in the coming years—provides a strong macro tailwind, institutional investors are becoming increasingly selective, rewarding firms that can demonstrate consistent earnings growth over those that rely solely on industry-wide tailwinds.