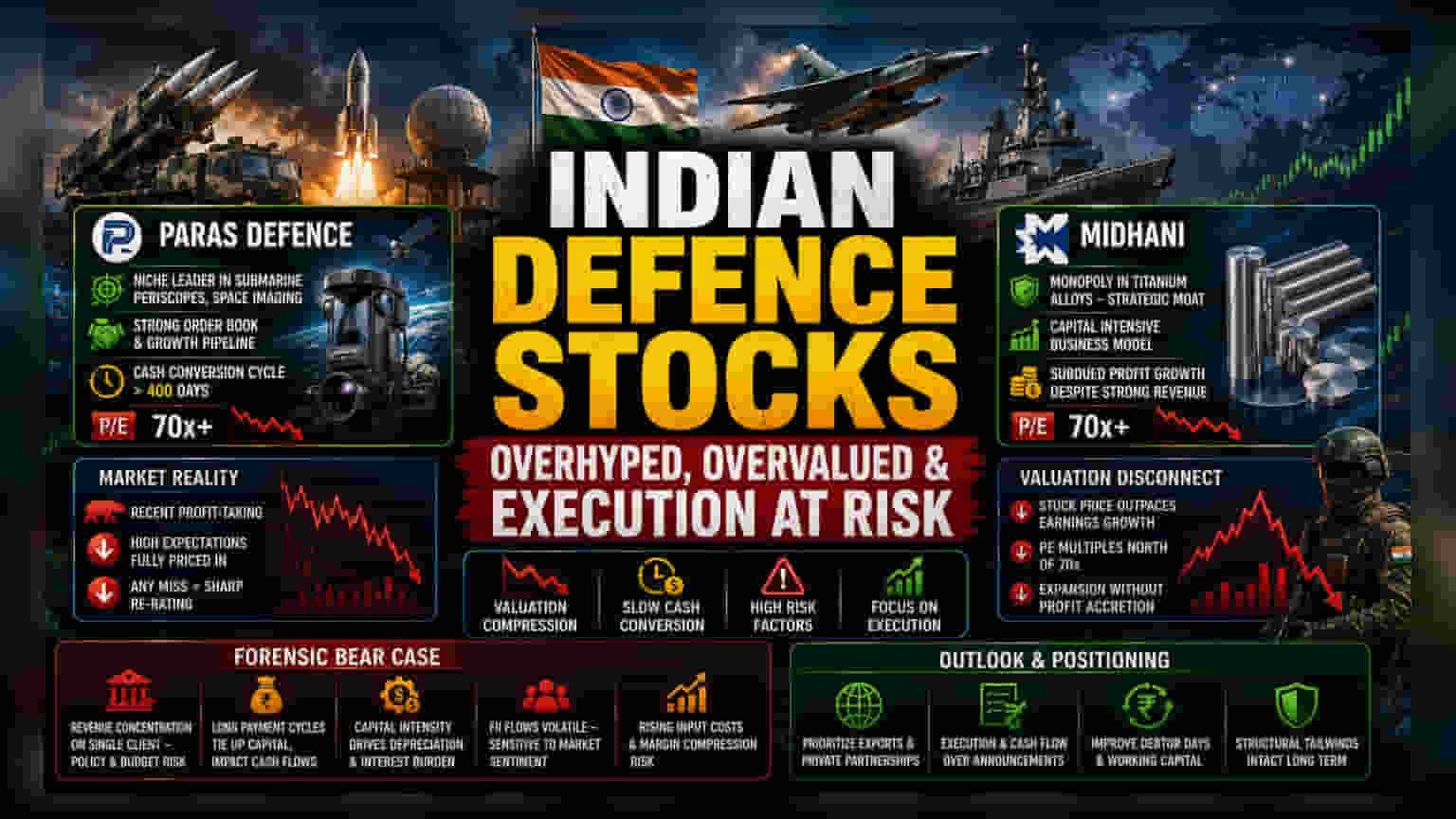

The Valuation Compression Trap

While the narrative surrounding India’s defense industrial expansion remains largely positive, the market's pricing of this growth is showing signs of exhaustion. Companies like Paras Defence and Mishra Dhatu Nigam (MIDHANI) are currently navigating a reality where high market expectations, reflected in price-to-earnings (P/E) multiples often north of 70x, are colliding with the mundane challenges of government-contract business models. Unlike consumer-facing sectors with rapid cash conversion, defense entities often face prolonged debtor days and intensive capital requirements that can suppress free cash flow. When stocks trade at these elevated premiums, even minor misses in quarterly profit growth or guidance lead to immediate and sharp re-pricing, as seen in recent profit-taking cycles.

The Execution Pivot

Sector sentiment has transitioned from an expectation-driven phase into one defined by operational delivery. Investors are no longer content with mere announcements of multi-year collaboration agreements; they are now discounting these order books based on the ability to execute. Paras Defence, for instance, maintains a competitive edge through its niche positioning in submarine periscopes and space-imaging systems, yet it must contend with a cash conversion cycle exceeding 400 days. Similarly, MIDHANI’s monopoly in titanium alloys provides a strategic moat, but the stock has struggled to outpace its own valuation expansion, leading to a disconnect between share price gains and underlying profit growth. For these firms, future performance is predicated on shifting from 'project announcements' to 'realized cash flow.'

The Forensic Bear Case

From a risk-averse perspective, the defense theme carries systemic vulnerabilities that are frequently overlooked during market rallies. First, revenue concentration remains a critical threat; reliance on a single primary client—the central government—exposes these companies to changes in procurement budgets, policy shifts, and payment cycle elongations. Second, capital intensity is a persistent burden. MIDHANI, for instance, faces pressure from fixed-asset depreciation and interest costs, which have contributed to subdued net profit growth despite strong revenue potential. Furthermore, the sector is increasingly sensitive to FII (Foreign Institutional Investor) flows, which have shown signs of volatility. If government capital expenditure slows or if margin compression occurs due to rising input costs, firms with lower operating leverage may struggle to maintain current market valuations.

Outlook and Market Positioning

The path forward for Indian defense players requires a disciplined approach. Analysts are increasingly prioritizing companies that demonstrate diversified revenue streams, particularly through exports and private-sector partnerships, over those tethered strictly to traditional, slow-moving procurement pipelines. While the long-term structural tailwinds of indigenous manufacturing and self-reliance remain intact, the near-term environment suggests that stock returns will be driven by idiosyncratic operational success rather than broad-based sector tailwinds. Investors should watch for improvements in debtor days and EBITDA stability as key indicators of whether these companies can justify their current valuation premiums.