Hitachi Energy India reported strong FY26 results with a 157% profit jump and an order backlog worth Rs 29,555 crore. The company also announced a Rs 4,000 crore investment to expand capacity. We analyze the growth, high valuation, and what investors should watch next.

What Happened

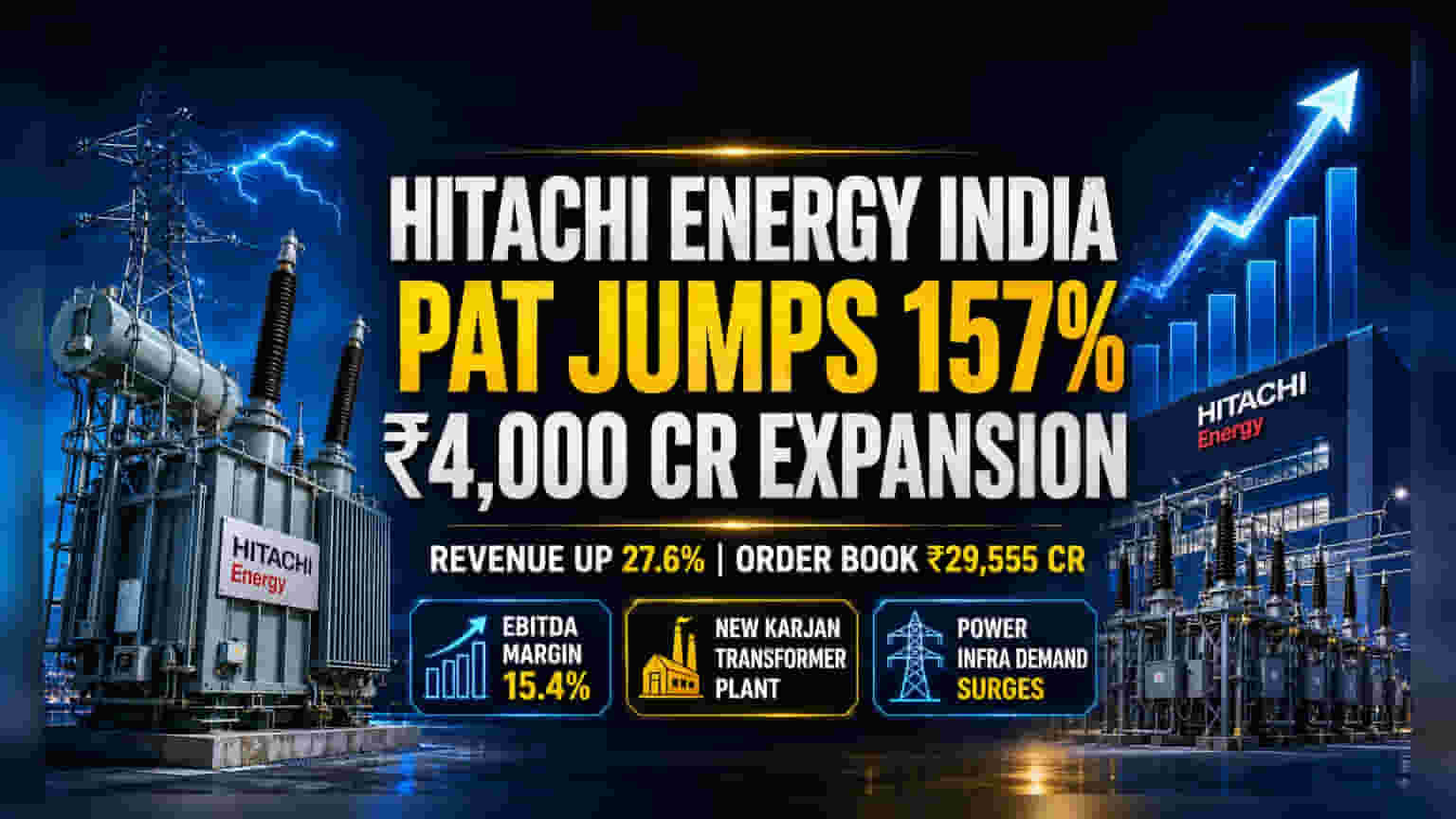

Hitachi Energy India reported a strong performance for the financial year 2026, driven by rising demand for power infrastructure. The company’s revenue for the year grew by 27.6%, while Profit After Tax (PAT) saw a sharp increase of 157.3%. A key highlight of the year was the expansion of the EBITDA margin, which rose to 15.4% from 9.3% in the previous year. Alongside these financial results, the company announced a significant capital spending plan of Rs 4,000 crore to build a new large power transformer facility in Karjan, Vadodara, which is expected to begin production in late 2028.

The Order Book Strength

One of the most important metrics for an industrial company is its order backlog—the value of orders received but not yet completed. Hitachi Energy India finished FY26 with an order backlog of Rs 29,555 crore. This is a 53.6% increase compared to the previous year. For investors, this backlog is crucial because it offers revenue visibility of roughly 3.6 times the company's annual revenue. This means the company has a strong pipeline of work, which helps reduce uncertainty about future income, provided the company can execute these projects on time.

Why Margins Improved

The jump in profit margins from 9.3% to 15.4% is a notable shift. This usually happens due to what analysts call operational leverage. In simple terms, as the company scales up its operations and handles a larger volume of work, its fixed costs (like overheads and administrative expenses) do not rise at the same speed as its revenue. This allows a larger portion of every rupee earned to flow directly to the bottom line as profit. Investors should watch if the company can maintain these higher margin levels as it takes on new projects.

The Capex Strategy

The management has committed Rs 4,000 crore for a new manufacturing facility. This is a clear signal that the company anticipates long-term demand for power infrastructure, specifically in areas like renewable energy and data centers. By investing in capacity, the company is aiming to secure its future growth. However, such large projects involve execution risks. Investors will need to track the progress of this project to ensure it remains on schedule and within budget, as any delays or cost overruns could impact the company’s cash flow.

How Investors May Read This

Hitachi Energy India’s stock currently trades at a price-to-earnings (P/E) multiple of around 149x. This is a premium valuation compared to the broader industrial sector. This high valuation suggests that the market has high expectations for the company's future growth and earnings potential. While the fundamentals show strong momentum, a premium valuation leaves less room for error. If the company fails to meet these high growth expectations, the stock price could become sensitive to such news.

What Investors Should Track

Moving forward, the primary monitorables for investors include the execution of the existing Rs 29,555 crore order book and the timeline of the new Karjan facility. Any updates on supply chain constraints or raw material price fluctuations could affect margins. Furthermore, investors should watch for management commentary on order inflows, as the company’s growth is heavily tied to India’s massive transition toward renewable energy and the expansion of the national transmission grid. Maintaining current profit margins while scaling up capacity will be the real test for the company in the coming years.