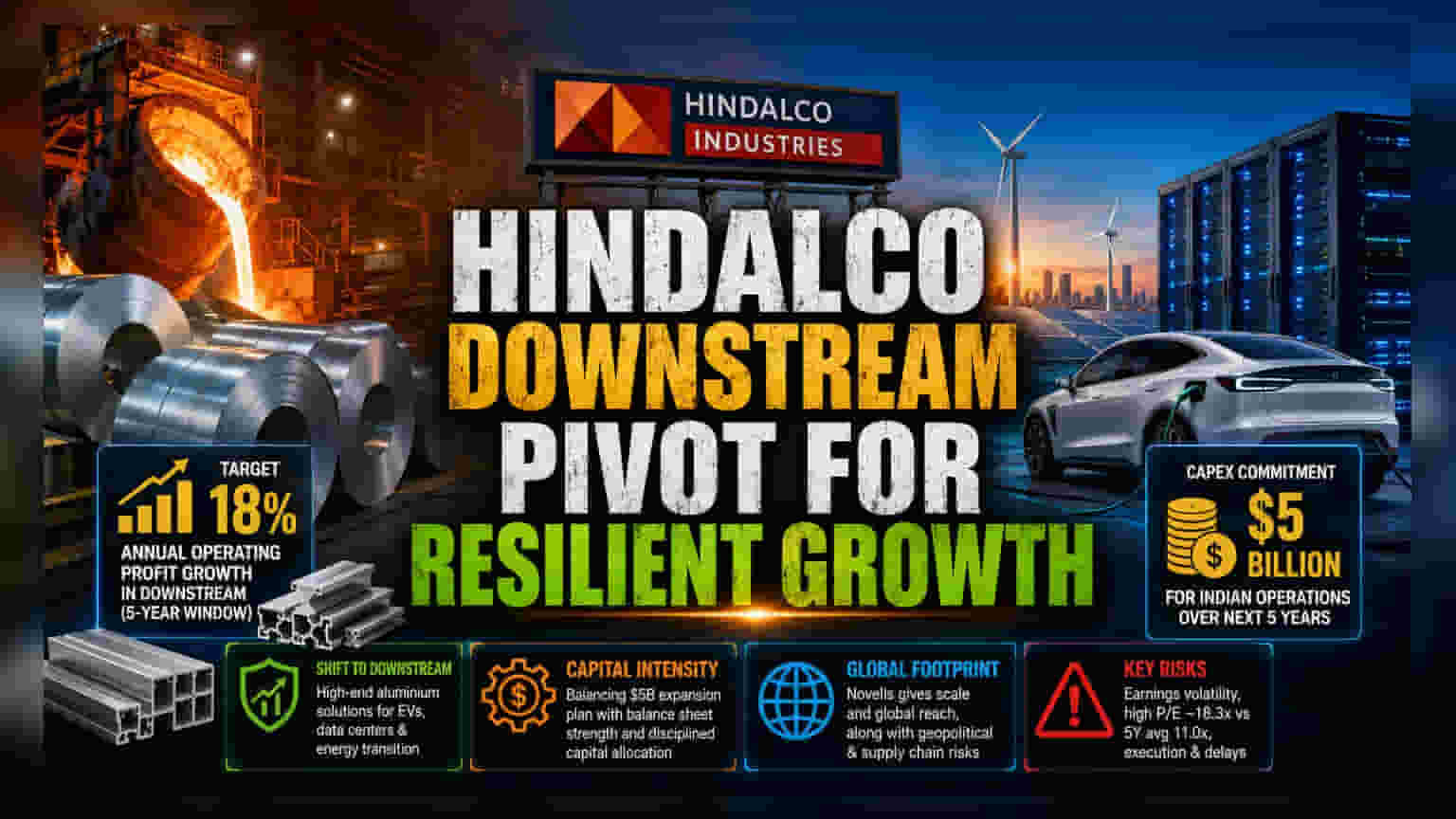

The Shift to Downstream Resilience

Hindalco Industries is executing a strategic pivot to buffer its earnings against the inherent volatility of the London Metal Exchange (LME). By directing its capital expenditure toward downstream operations, the company seeks to move beyond its traditional role as a primary metal producer. Management aims to capitalize on the increasing demand for high-end aluminium applications, specifically in electric vehicles, data centers, and the energy transition sector. This transition from a volume-heavy commodity player to a solution-oriented manufacturer is designed to secure more stable, premium-priced revenue streams, with the company specifically targeting an 18% annual operating profit growth in its downstream business over the coming five-year window.

The Capital Intensity Dilemma

While the downstream push offers a pathway to margin stability, it demands significant financial commitment. Hindalco has earmarked approximately $5 billion for Indian operations over the next five years to support both upstream and downstream expansion. This expenditure comes at a time when the company must balance its growth ambitions with the need for a healthy balance sheet. Despite recent deleveraging efforts, the company’s capital allocation strategy remains under scrutiny by investors who are weighing the long-term benefits of portfolio enrichment against the potential for temporary margin compression during the construction and commissioning phases of these projects.

Competitive Positioning and Market Context

In the domestic arena, Hindalco faces a high-stakes competitive landscape. Its primary rival, Vedanta, is also engaged in aggressive capacity expansion to capture the growing demand for non-ferrous metals. Unlike smaller competitors such as NALCO, which remain focused on integrated upstream efficiencies, Hindalco’s scale allows it to compete on a global stage through its subsidiary, Novelis. However, this global exposure acts as a double-edged sword, subjecting the company to international geopolitical tensions and supply chain disruptions that do not impact pure-play domestic producers to the same degree.

The Forensic Bear Case: Risks and Structural Weaknesses

Investors must account for several structural risks inherent in the current growth trajectory. A primary concern is the company's susceptibility to earnings quality, as recent fiscal reports have highlighted the impact of unusual expenses and margin volatility. Furthermore, the company’s reliance on capital-intensive expansion projects leaves little room for error should global demand for transportation and green-energy products stagnate. While the firm has maintained a "Buy" consensus among many analysts, there is a clear valuation split; the stock’s current price-to-earnings (P/E) ratio—hovering around 18.3x—is frequently flagged as overvalued when measured against its five-year historical average of 11.0x. This suggests that much of the future growth is already priced into the shares, leaving the stock vulnerable to corrections if upcoming operational milestones or quarterly margins disappoint. Past litigation and project implementation delays have also tempered enthusiasm for some institutional investors who remain cautious about the execution risk of these massive multi-billion dollar capital outlays.