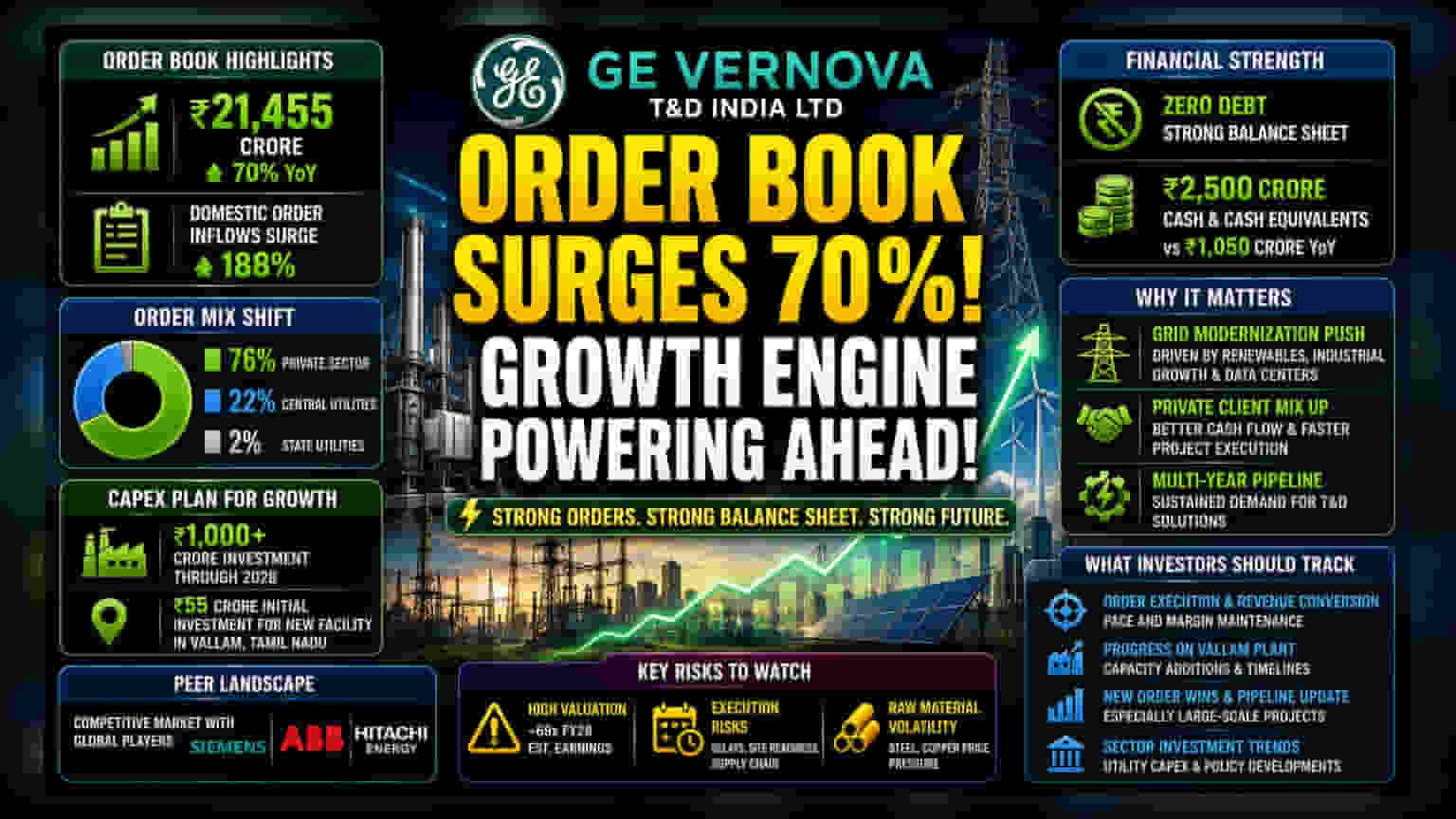

GE Vernova T&D India reported a massive 70% jump in its order book to Rs 21,455 crore, fueled by India’s grid modernization. While the company has zero debt and strong cash reserves, investors are weighing the high valuation, with the stock trading at roughly 69 times estimated FY28 earnings.

What Happened

GE Vernova T&D India Ltd has reported significant growth in its business performance for the quarter ending March 2026. The company’s order book reached Rs 21,455 crore, marking a 70 percent increase compared to the previous year. A key detail in this growth is the 188 percent surge in domestic order inflows. Furthermore, the company has successfully shifted its order mix, with private sector and central utility projects now making up 76 percent and 22 percent of its total backlog, respectively. To support this demand, the company has announced plans to invest over Rs 1,000 crore through 2028, with an initial allocation of Rs 55 crore for a new facility in Vallam, Tamil Nadu.

Why This Matters For Investors

India is currently in the middle of a major push to modernize its electricity grid. This is driven by the need to integrate renewable energy sources like solar and wind, which require stable transmission infrastructure, and a rising demand for power from industrial zones and data centers. For a company like GE Vernova T&D, which specializes in transmission and distribution solutions, this creates a sustained multi-year pipeline of work. The shift toward private sector clients is particularly important because private projects often have different payment cycles and contract terms compared to state utilities, which can help in better cash flow management and faster project execution.

Financial Health

Financially, the company maintains a strong position with zero debt on its balance sheet. This is a significant advantage in the capital-intensive power equipment sector, as it allows the company to fund its growth and capacity expansion without the pressure of interest payments. The company ended the year with Rs 2,500 crore in cash and cash equivalents, up from Rs 1,050 crore the year before. This liquidity provides the necessary cushion to invest in new manufacturing facilities and handle potential fluctuations in working capital requirements.

Peer And Sector Context

GE Vernova operates in a competitive environment alongside major players like Siemens, ABB India, and Hitachi Energy India. These companies also provide similar high-voltage and transmission solutions. The success of these firms is tied to the broader health of the power infrastructure sector. While all these companies benefit from the same national grid modernization plans, investors often look at how effectively each player manages its execution and profit margins amidst rising raw material costs, such as steel and copper, which are essential for manufacturing electrical equipment.

Risks And Concerns

While the growth outlook is positive, investors should be aware of several risks. First, the stock is currently trading at a high valuation—approximately 69 times estimated FY28 earnings. This means that a large part of the company's future growth is already reflected in the stock price, leaving little room for error. Second, the power equipment sector is prone to execution risks. Delays in project site readiness, supply chain bottlenecks, or unforeseen changes in government policy can stall order execution. Finally, as a manufacturer, the company is sensitive to fluctuations in the prices of raw materials. If commodity prices rise unexpectedly and the company cannot pass these costs on to customers, profit margins could come under pressure.

What Investors Should Track

Moving forward, the primary monitorables for investors will be the actual execution speed of the existing order book. Keeping an eye on how quickly the company converts these orders into revenue while maintaining or improving profit margins will be essential. Investors may also track management commentary regarding the progress of the new manufacturing facility in Tamil Nadu and any updates on new large-scale project wins. Finally, observing the broader sector trends, such as the actual pace of investment by private and central utilities in grid infrastructure, will help in assessing whether the demand environment remains supportive.