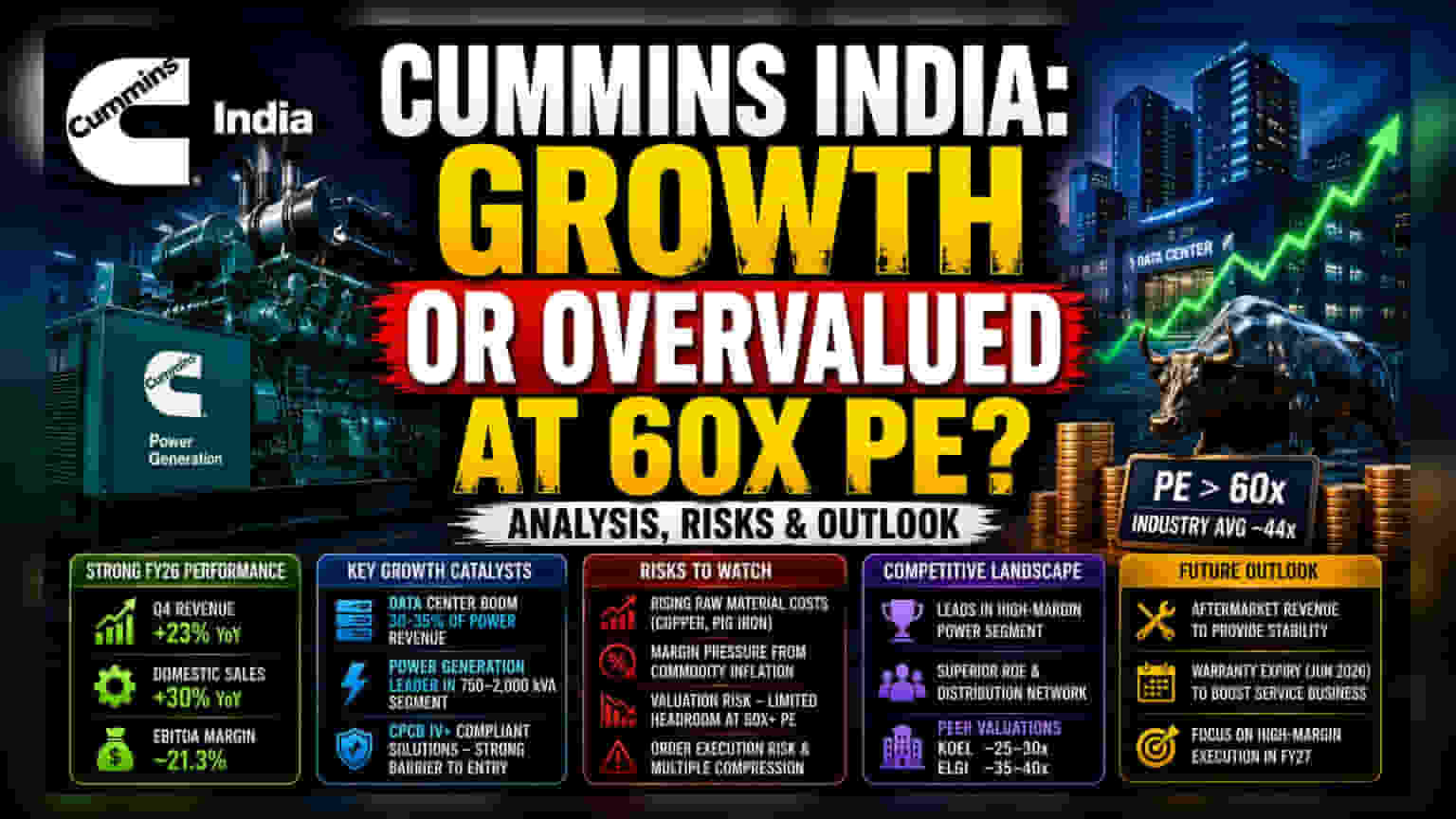

The Valuation Gap

Despite posting strong fiscal results, Cummins India’s recent market performance highlights the friction between operational success and investor expectations. The company recorded a 23% year-on-year revenue increase in the fourth quarter of fiscal 2026, largely bolstered by a 30% surge in domestic sales. However, the market’s reaction has been increasingly defensive. Trading at trailing price-to-earnings multiples exceeding 60x, the equity currently sits at a significant premium compared to the industrial engine sector average of roughly 44x. This valuation mismatch suggests that even as the company captures demand from India’s hyper-scale data center expansion, the stock price has likely already priced in the best-case growth scenarios.

The Catalyst and Competitive Landscape

Power generation revenue remains the primary engine of growth, benefiting from high-margin demand across data centers, pharmaceutical plants, and luxury real estate. Cummins India continues to lead in the 750–2,000 kVA power segment, a domain where its ability to provide localized, CPCB IV+ compliant solutions serves as a critical barrier to entry for smaller competitors. While peers such as Kirloskar Oil Engines and Elgi Equipments operate with lower valuation multiples, Cummins maintains its lead through superior return on equity metrics and a robust distribution footprint. The data center boom—accounting for roughly 30-35% of annual power generation revenue—has proven to be a structural, rather than cyclical, tailwind for the firm.

The Forensic Bear Case

Institutional skepticism is mounting not due to a lack of operational excellence, but due to margin vulnerability and valuation exhaustion. The company is currently grappling with rising costs for key raw materials such as copper and pig iron. While the company has successfully utilized operating leverage to maintain EBITDA margins near 21.3%, channel checks suggest that further price hikes may struggle to keep pace with persistent commodity inflation. Furthermore, the stock’s recent descent from record highs, underperforming broader market indices, signals that institutional investors are taking profits. Any disappointment in the execution of the order-to-revenue pipeline could lead to sharp multiple compression, given the stock's lack of headroom at current levels.

The Future Outlook

Looking ahead to FY27, management guidance remains cautiously optimistic, focusing on the aftermarket segment as a steady revenue floor. The expiration of warranty periods for CPCB IV+ compliant units starting in June 2026 is projected to catalyze a shift toward recurring service revenues. However, with brokerage consensus recalibrating price targets and some analysts shifting toward a defensive stance, the focus for the coming quarters will be on whether the company can sustain its premium valuation through consistent, high-margin execution in a volatile macro environment.