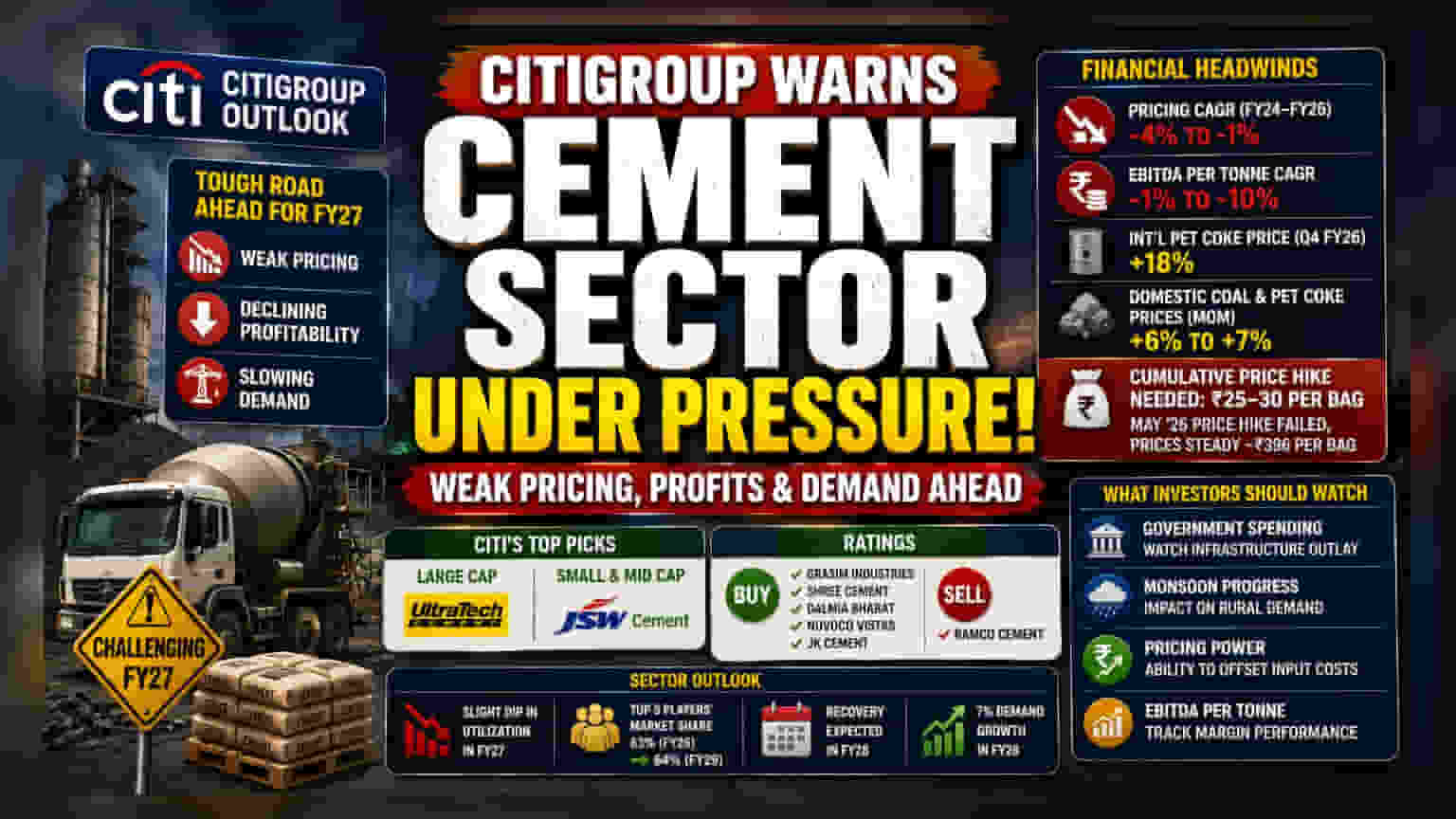

Citigroup predicts a challenging fiscal year 2027 for India's cement industry, citing weak pricing and demand slowdowns. While the brokerage maintains a cautious outlook for the sector, it favors Ultratech Cement and JSW Cement as top picks. It also assigned 'Buy' ratings to several major players while labeling Ramco Cement as a 'Sell'.

What Happened

Citigroup has issued a cautionary outlook for the Indian cement sector, predicting significant difficulties for the upcoming fiscal year 2027. The report highlights that cement companies are likely to face pressure from weak pricing, declining profitability, and a slowdown in demand. These issues are partly attributed to a potential reduction in government infrastructure spending and concerns regarding a weak monsoon season. According to the analysis, these factors could lead to lower capacity utilization and squeezed profit margins for many industry players.

Financial and Business Context

The data provided by Citigroup paints a difficult picture of the recent past. Between fiscal years 2024 and 2026, many companies experienced a negative compound annual growth rate in pricing, ranging from -4% to -1%. Similarly, operating profit (EBITDA) per tonne also showed a negative trend for most firms, falling between 1% and 10%.

Input costs have added to the burden. International pet coke prices rose by 18% in the fourth quarter of fiscal year 2026. Domestic prices for coal and pet coke also saw month-on-month increases of 6% to 7%. The report suggests that to recover these costs and stabilize margins, the industry may require a cumulative price hike of Rs 25 to 30 per bag. However, attempts to raise prices in May 2026 largely failed due to intense competition and soft demand, keeping prices steady around Rs 396 per bag.

Sector Picks and Ratings

Despite the broader sector challenges, Citigroup identified specific companies that it prefers. Ultratech Cement is highlighted as a top pick among large-cap stocks, while JSW Cement is preferred in the small and mid-cap categories. The brokerage assigned 'Buy' ratings to Grasim Industries, Shree Cement, Dalmia Bharat, Nuvoco Vistas, and JK Cement, suggesting confidence in their specific business models. Conversely, the brokerage maintained a 'Sell' rating on Ramco Cement.

Market and Demand Risks

The report anticipates that the cement sector will struggle through fiscal year 2027, with a slight dip in overall utilization levels. While consolidation is expected to continue—with the top five players projected to increase their market share from 63% in fiscal year 2026 to 64% by fiscal year 2029—it is not expected to happen at a rapid pace. The firm projects a potential recovery only in fiscal year 2028, driven by an expected 7% growth in demand and better industry utilization.

What Investors Should Track Next

Investors may want to monitor several key indicators that could impact the sector's performance:

- Government Spending: A sustained slowdown in government infrastructure projects could continue to dampen demand.

- Monsoon Progress: The impact of monsoon rains on rural construction demand remains a critical factor.

- Pricing Power: The ability of companies to successfully implement price hikes to offset rising input costs like pet coke and coal.

- EBITDA Per Tonne: Future quarterly results will show if companies can maintain or improve their profit margins despite the pricing pressure.