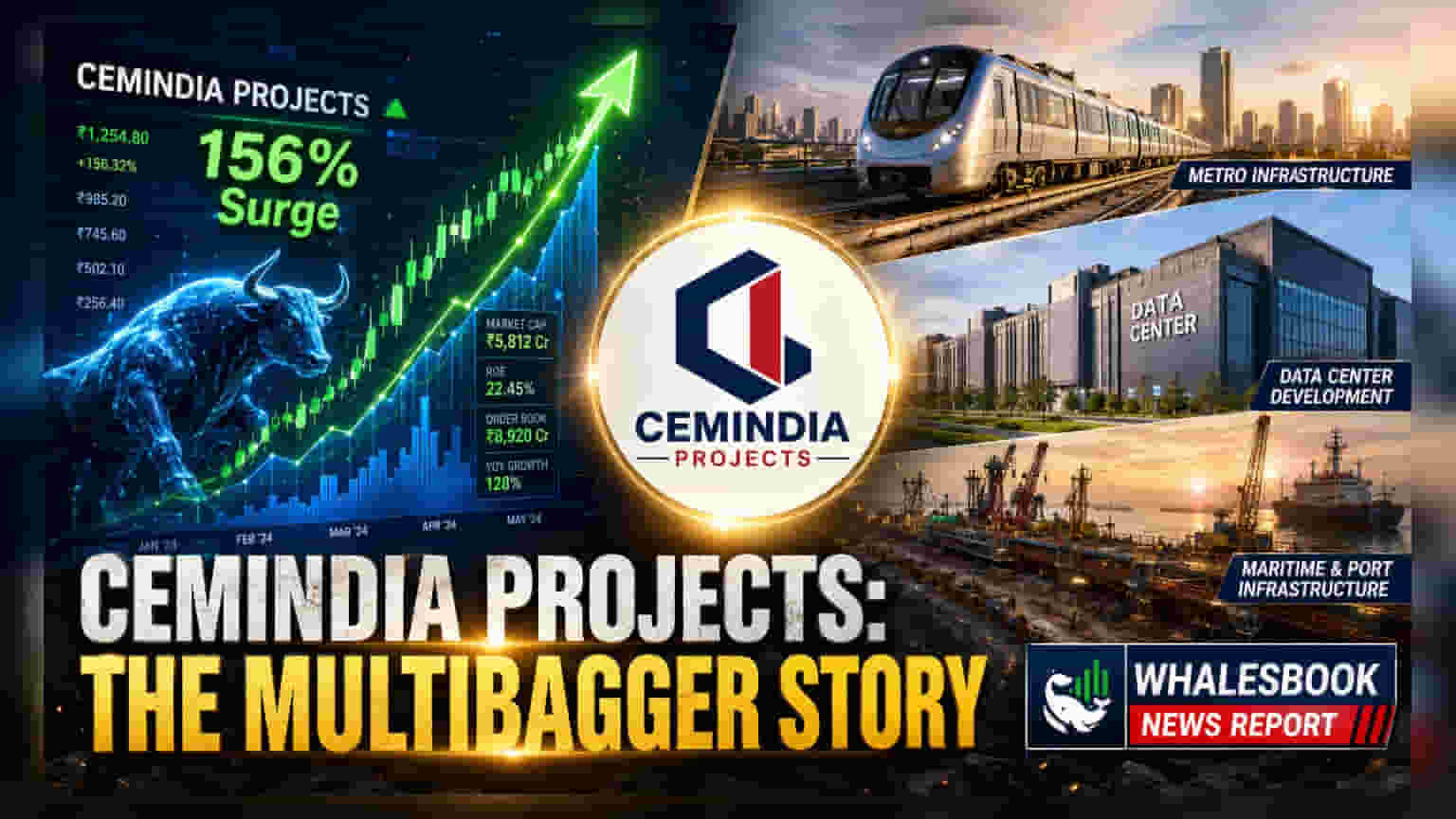

Cemindia Projects stock has rallied 156% in three months, hitting a 52-week high after reporting strong Q4 FY26 results. The company, now under Adani Group ownership, reported a 113.6% jump in quarterly net profit and a record order book. Investors are now balancing this growth against a higher valuation compared to historical averages.

What Happened

Cemindia Projects Limited, the infrastructure company formerly known as ITD Cementation, has seen its stock price surge by approximately 156% over the last three months. On July 1, 2026, the stock touched a new 52-week high of Rs 1,363.75, following a sustained period of market interest. This rally was primarily triggered by the company's Q4 FY26 results released in late April, which exceeded market expectations. The company reported a 113.6% year-on-year growth in Profit After Tax (PAT) for the quarter, reaching Rs 242.17 crore on revenue of Rs 2,973.49 crore. This performance helped the company cross the milestone of Rs 10,000 crore in annual revenue for the first time.

The Adani Acquisition Context

This upward momentum follows a period of consolidation after the company was acquired by Renew Exim DMCC, an Adani Group entity, in May 2025. Following the acquisition, the stock experienced a phase of volatility, with a significant drawdown from its 2025 peak as investors waited for evidence that the new promoter ownership would translate into better operational execution. The recent quarterly results provided that evidence, signaling to the market that the company’s business model is delivering on its growth targets under the new management. The market now views the company as a potential key beneficiary of the Adani Group's extensive infrastructure project pipeline.

Financial Performance and Order Book

Cemindia Projects ended FY26 with a record order book of Rs 24,545 crore, which is approximately 2.4 times its annual revenue. This provides the company with significant revenue visibility for the next two to two-and-a-half years. A key driver for this financial improvement has been margin expansion; the company reported an EBITDA margin of 15.1% in Q4 FY26, a notable improvement from 10.7% in the same quarter last year. The company is actively diversifying its project mix, with data centers emerging as a strategic growth segment, currently contributing around Rs 3,000 crore to the order book.

Valuation and Market Concerns

With the sharp rise in share price, the company’s valuation has shifted. Cemindia Projects is currently trading at a Price-to-Earnings (P/E) ratio of 39.8x, which is significantly higher than its three-year median P/E of 27.9x. While earnings growth has been strong, investors should note that the stock is now trading at a premium. The PEG ratio—a measure of valuation relative to expected growth—stands at 0.58, suggesting that the current valuation is supported by the aggressive growth narrative, but the stock remains sensitive to any sign of a slowdown in execution or profitability.

What Investors Should Track

As Cemindia Projects enters FY27 with ambitious growth targets, investors may monitor a few key areas. First is the sustainability of the improved EBITDA margins, which will depend on controlling input costs in a cyclical infrastructure sector. Second, the company has guided for 20-25% revenue growth in FY27; meeting this will require consistent project execution. Finally, while the order book is at a record high, investors should watch for the pace of actual order conversion and the ability of the company to manage its working capital effectively in a capital-intensive environment.