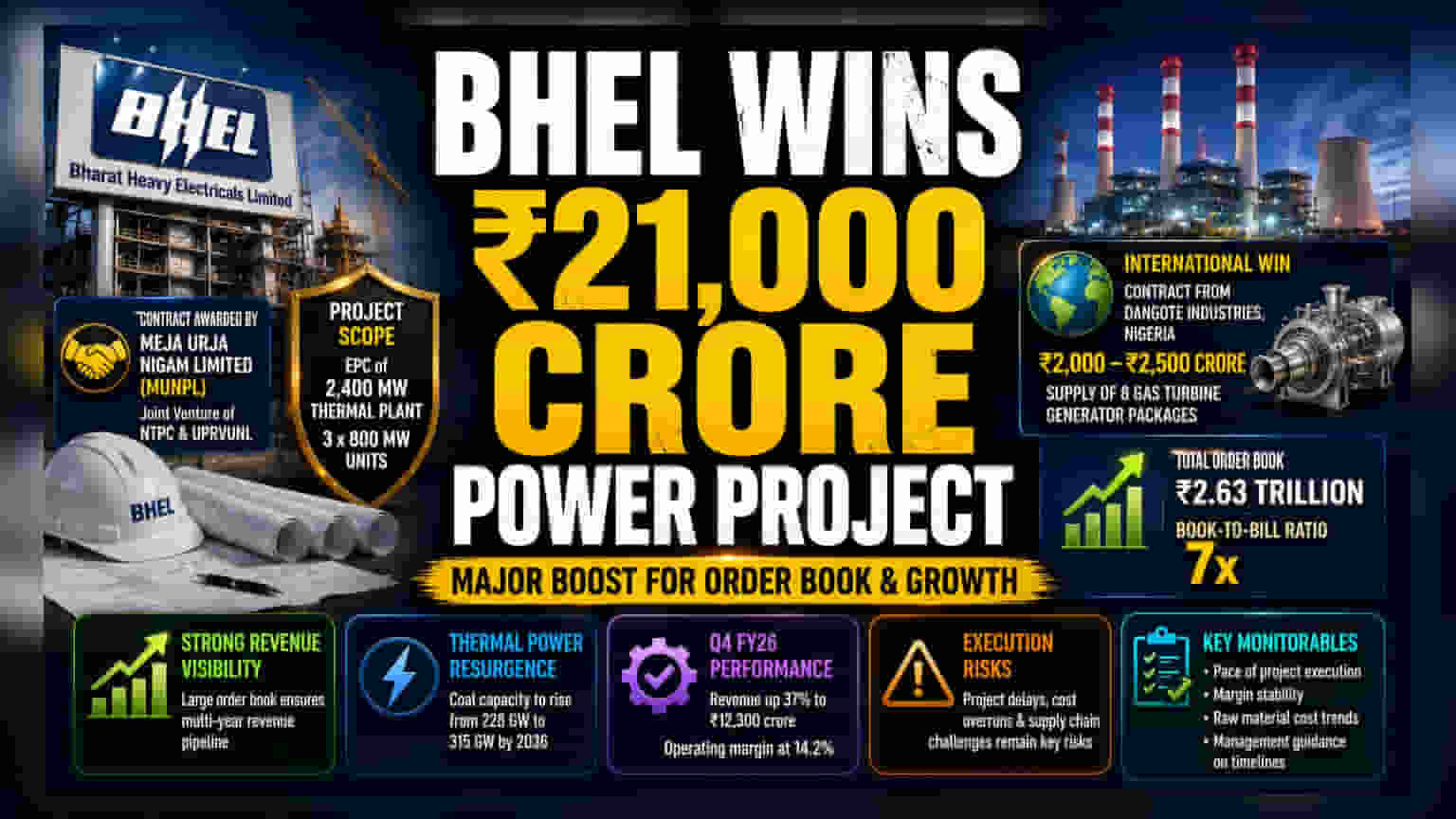

What Happened

Bharat Heavy Electricals Limited (BHEL) has landed a major project worth Rs 21,000 crore to build a thermal power plant. The contract was awarded by Meja Urja Nigam Limited (MUNPL), a joint venture between NTPC and the Uttar Pradesh Rajya Vidyut Utpadan Nigam. The scope of work includes the engineering, procurement, and construction (EPC) of a 2,400-megawatt thermal plant, structured as three 800-megawatt units. In addition to this large domestic win, BHEL also secured a contract valued between Rs 2,000 crore and Rs 2,500 crore from Dangote Industries in Nigeria to supply eight gas turbine generator packages. These combined wins have pushed BHEL's total order book to Rs 2.63 trillion.

Why This Matters For Investors

The size of this order is significant because it provides clear revenue visibility for the next several years. In the engineering and construction business, a strong order book acts as a buffer against future demand fluctuations. With this addition, BHEL's book-to-bill ratio, which measures the amount of work on hand compared to annual revenue, now stands at 7x. This indicates that the company has a substantial pipeline of work to execute, which can support top-line growth if the projects are delivered on time and within budget.

The Growth in Thermal Power

This order highlights the recent shift in the Indian power sector. After a long period where the industry focused heavily on renewables, there is renewed interest in thermal power to act as a reliable baseload provider for the electricity grid. Official projections suggest that India’s total installed capacity will see a sharp rise in the coming decade, with thermal coal capacity expected to expand from the current 228 gigawatts to 315 gigawatts by 2036. For BHEL, this represents a long-term opportunity, as the company is one of the few major players capable of executing large-scale, complex power projects in the country.

Execution and Margin Risks

While winning the order is a positive step, the real test for BHEL lies in execution. Large EPC projects often face challenges like project delays, cost overruns, and supply chain disruptions, which can quickly turn a profitable order into a burden. The company’s financial performance has shown improvement, with Q4 FY26 revenue jumping 37% to Rs 12,300 crore and operating margins reaching 14.2%. However, investors often look at how BHEL compares with competitors like Thermax, which historically manages project execution and profit margins with more consistency. If BHEL can improve its own execution efficiency, it could see a stronger improvement in its valuation.

What Investors Should Track

Moving forward, the primary monitorables for shareholders will be the pace of project execution and the stability of profit margins. Rising raw material costs and inflation can create pressure on project costs, which may impact bottom-line profitability. Investors may keep a close eye on management commentary regarding the timeline for the Meja Urja Nigam project and whether the company can maintain its margin improvements in the upcoming quarters. The ability to complete these projects without delays will be essential for the company to convert its large order book into sustained earnings growth.