Amber Enterprises has commenced a Rs 6,785 crore expansion in Uttar Pradesh, targeting a $2 billion revenue milestone. The investment focuses on a high-tech PCB and semiconductor substrate joint venture with Korea Circuit, aiming to reduce import dependence while expanding its manufacturing capabilities across consumer durables and electronics.

What Happened

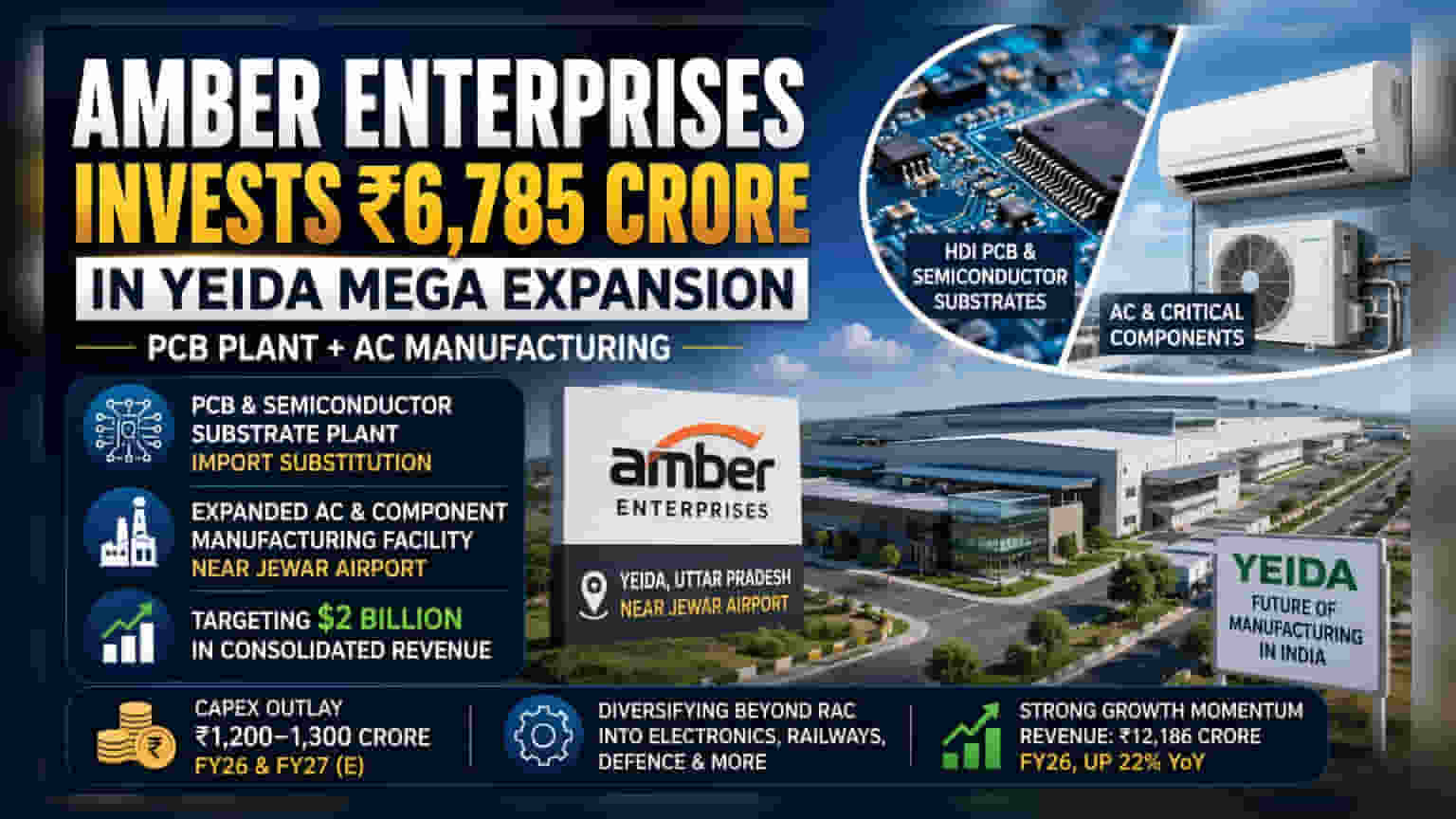

Amber Enterprises has officially launched a major expansion project in the Yamuna Expressway Industrial Development Authority (YEIDA) area of Uttar Pradesh, with a planned investment of Rs 6,785 crore. The company, which is transitioning from a traditional room air conditioner manufacturer to a diversified electronics manufacturing services (EMS) player, is setting up two critical manufacturing facilities near Jewar Airport. One project involves a high-density interconnect (HDI) printed circuit board (PCB) and semiconductor substrate plant, established through a 70:30 joint venture with South Korea’s Korea Circuit. The second project involves an expanded manufacturing complex for air conditioners and critical components. This expansion is designed to drive the company toward its goal of reaching $2 billion in consolidated revenue.

Strategic Focus on Import Substitution

The PCB manufacturing initiative is a key part of the group's strategy to move up the value chain. India’s electronics manufacturing sector relies heavily on imported components, with the PCB market alone valued at approximately Rs 40,000 crore annually. By localizing the production of high-density interconnect (HDI), flexible PCBs, and semiconductor substrates, Amber Enterprises aims to replace these imports with domestic supply. This aligns with government schemes like the Electronics Component Manufacturing Scheme (ECMS), which provide incentives to encourage indigenous manufacturing of electronics components.

Financial and Business Context

Amber Enterprises reported a consolidated revenue of Rs 12,186 crore for FY26, representing a 22% year-on-year increase. While the electronics division is experiencing strong growth—cited by management as 40-45% annually—the consumer durables segment, which traditionally accounted for a significant portion of revenue, has faced a more moderate environment characterized by slower volume growth and margin pressure. The company is actively diversifying its portfolio to reduce its dependence on the cyclical room air conditioner (RAC) business, which previously formed the bulk of its revenue. Through acquisitions and capacity expansion in railway subsystems, defense, and electronics, the firm is attempting to stabilize its revenue base.

Execution and Capital Risks

For investors, the scale of this investment is significant. Amber has outlined a total capital expenditure (capex) of Rs 1,200–1,300 crore for the current financial year, with a similar outlay expected in the following year. This capital spending is being funded through a combination of internal accruals, debt, and equity, including foreign direct investment. While these investments are aimed at long-term growth, they carry execution risks. Large-scale infrastructure projects require successful commissioning and ramp-up to ensure expected returns. Additionally, as the company enters more complex segments like semiconductor substrates, it faces the challenge of maintaining profit margins amidst potential pricing pressure and competition from existing global players.

What Investors Should Track

The primary monitorable for investors will be the commissioning timeline of these YEIDA facilities and the subsequent speed of production ramp-up. The company's ability to maintain its margin profile, despite higher capital spending and potential competitive pressure in the component space, remains critical. Additionally, stakeholders should watch for updates on revenue growth targets and how effectively the group manages its debt levels while funding these large-scale expansion plans.