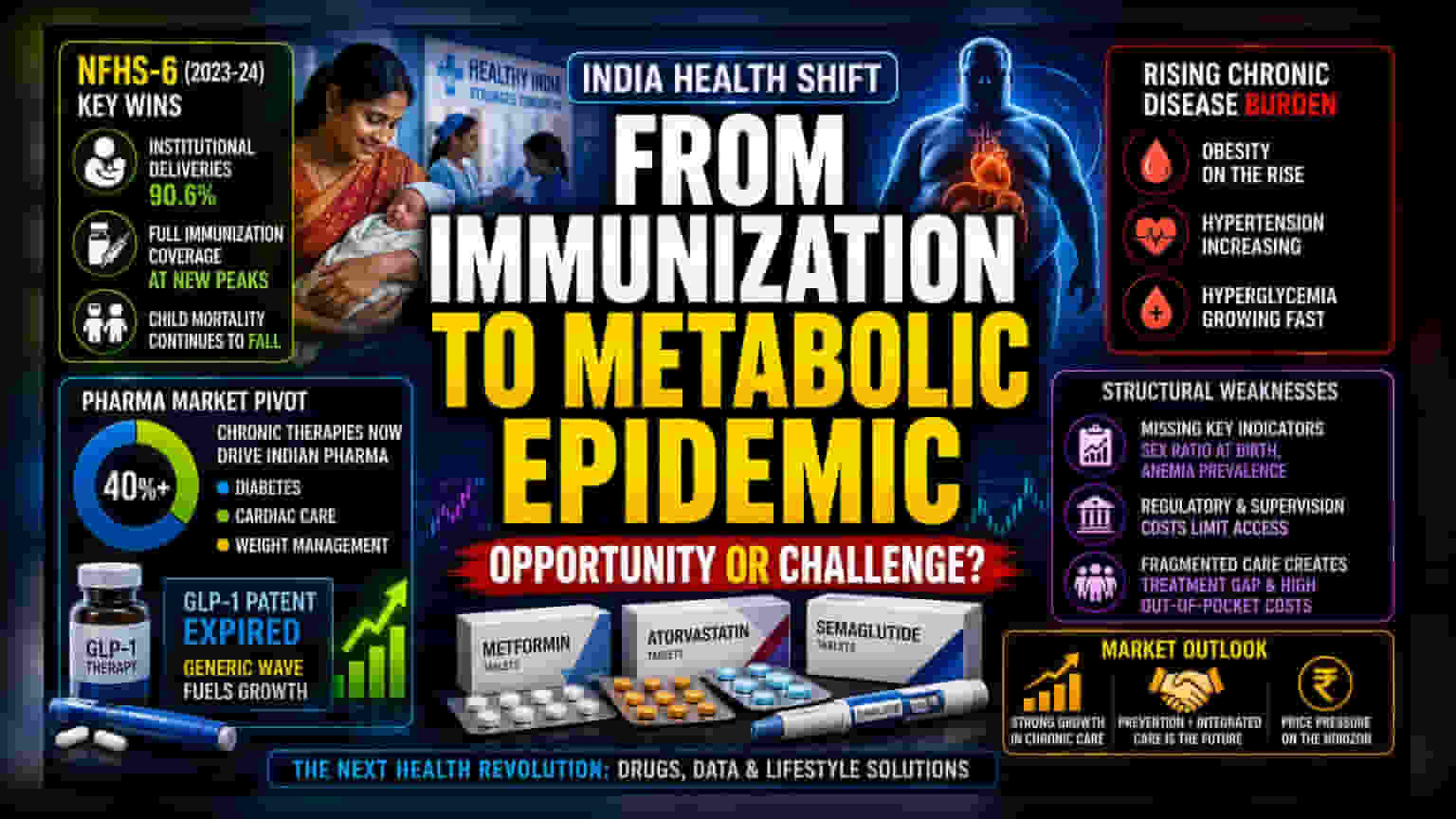

The Shift to Chronic Disease

The release of the NFHS-6 (2023-24) data confirms that India’s public health trajectory has entered a new phase. While the survey celebrates institutional delivery rates hitting 90.6% and immunization coverage reaching new peaks, these markers of acute health success are increasingly overshadowed by a structural rise in non-communicable diseases. The data points to a population increasingly defined by a dual health profile: falling child mortality alongside a rapidly expanding cohort of adults struggling with obesity, hypertension, and hyperglycemia.

The Pharmaceutical Pivot

This epidemiological transition is fundamentally reshaping the commercial healthcare market. Financial data from the pharmaceutical sector suggests that chronic therapy segments—specifically diabetes, cardiac care, and weight management—now account for over 40% of the total domestic market. This shift is not merely statistical; it is a volume-driven response to the chronic disease burden. With the recent patent expiration of GLP-1 receptor agonists, competition has intensified, leading to a surge in affordable generic alternatives. Major domestic players have aggressively reallocated R&D and supply chain resources toward the anti-obesity and metabolic health categories, treating them as the primary engines for future revenue growth.

The Structural Weakness

Despite the clear data on rising metabolic risks, the survey’s methodological gaps present a significant challenge for long-term health policy. The omission of granular indicators like the sex ratio at birth and detailed anemia prevalence complicates the ability of firms and policymakers to accurately forecast healthcare resource allocation. Furthermore, while the adoption of generic obesity treatments is rising, the industry faces significant friction from regulatory hurdles and the high cost of comprehensive clinical supervision. The reliance on fragmented private markets for specialized chronic care creates a 'treatment gap' where medicine availability often outpaces public health infrastructure, leaving middle- and lower-income populations vulnerable to high out-of-pocket expenses.

Market Outlook and Future Risks

Broader market sentiment remains cautiously bullish on the pharmaceutical sector’s ability to monetize this chronic disease shift. However, analysts warn that the dependence on lifestyle-based drugs carries long-term margin pressure, as intense competition among generic manufacturers drives prices downward. Looking ahead, the focus for both the state and private stakeholders is shifting toward preventive wellness. The successful penetration of GLP-1 therapies in the Indian context will likely hinge on the industry’s ability to move beyond simple drug manufacturing and into integrated care models that can address the root causes of the lifestyle disease surge.