The Shift Toward Precision Economics

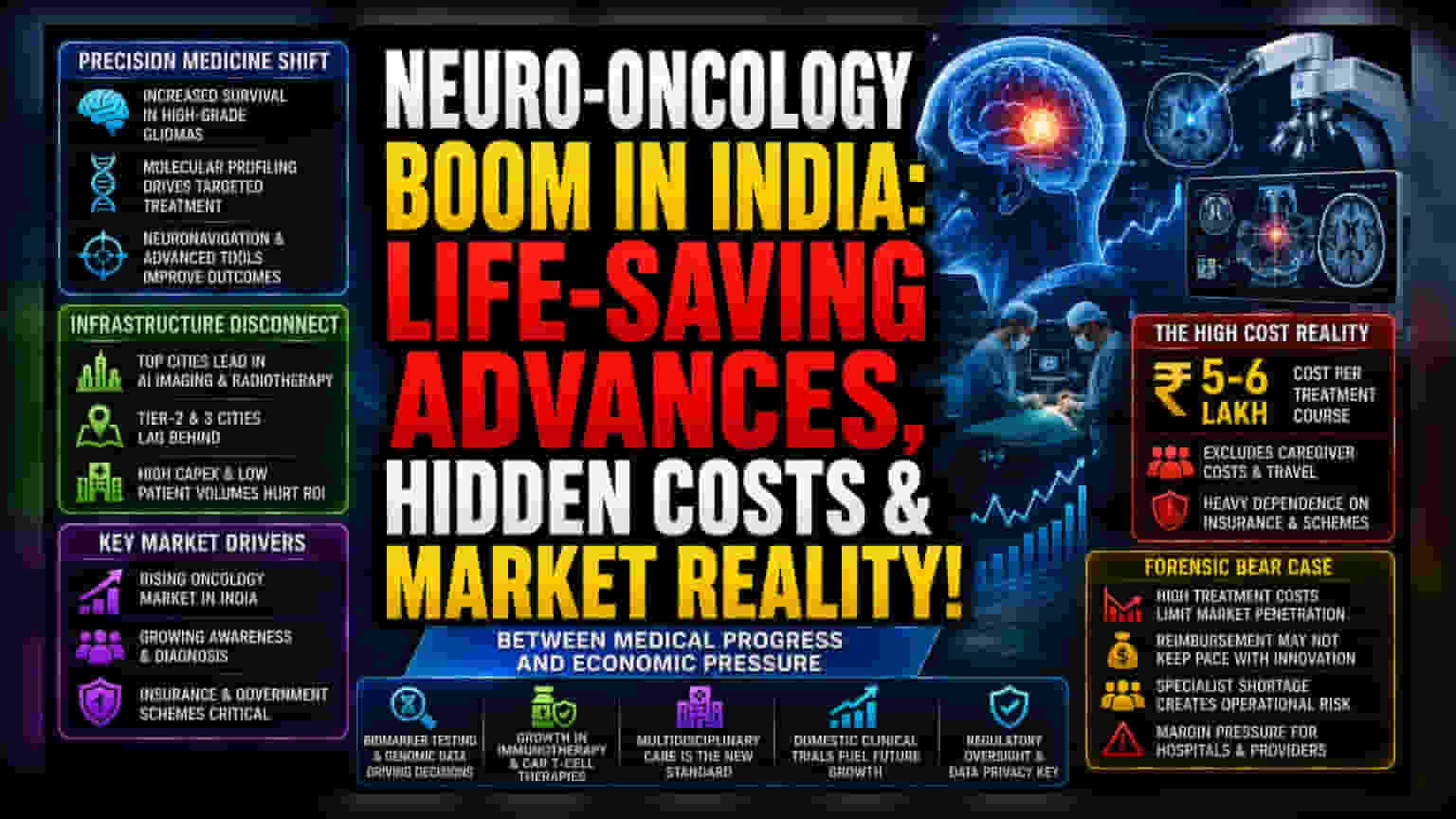

The narrative surrounding neuro-oncological outcomes in India has shifted from palliative management to life-extending intervention. Recent data confirms a marked increase in survival markers for high-grade gliomas, largely attributed to the integration of molecular profiling and neuronavigation tools. This clinical improvement creates a secondary economic reality: the demand for high-end diagnostic infrastructure is surging, placing pressure on private healthcare providers to upgrade technological assets to remain competitive in a rapidly specializing oncology market.

The Infrastructure Disconnect

While major urban hubs like Delhi-NCR and Mumbai have adopted state-of-the-art AI-assisted imaging and targeted radiotherapy, a clear regional disparity persists. The reliance on centralized, high-cost facilities creates a bottleneck for patient throughput. Furthermore, the reliance on specialized equipment introduces significant capital expenditure requirements for hospital chains. As providers look to scale, the ROI on these advanced oncology suites is increasingly dependent on high patient volumes, which are currently limited by late-stage referrals and a lack of early-detection screening protocols in Tier-2 and Tier-3 cities.

The Forensic Bear Case: Structural Weaknesses

Despite the medical optimism, the economic model for neuro-oncology in India faces structural hurdles. The direct medical costs of ₹5-6 lakh per course—excluding ancillary expenses like caregiver wages and specialized travel—act as a natural ceiling for market penetration. This financial burden makes the sector highly sensitive to insurance coverage limits and government-backed schemes like Ayushman Bharat. Should reimbursement rates fail to keep pace with the rising costs of immunotherapy and CAR T-cell therapies, providers will face acute margin compression. Additionally, the complexity of these cases requires a multidisciplinary workforce that is currently in short supply, creating a labor-driven operational risk for clinics attempting to scale this specialized service.

Market Outlook and Regulatory Influence

The trajectory of the sector is increasingly tethered to the advancement of domestic clinical trial ecosystems and the availability of biomarker testing. As the oncology market evolves, investors should monitor the regulatory environment surrounding genomic data and the commercialization of novel immunotherapies. Companies that can bridge the gap between high-cost innovation and affordable, high-volume delivery are likely to dominate, whereas those reliant on legacy models without precision capabilities risk obsolescence as the standard of care moves toward personalized genomic medicine.